When Goldmans Says "Buy Tesla Calls" Before Robotaxi Day, We're Near a Peak

When Goldmans Says "Buy Tesla Calls" Before Robotaxi Day, We're Near a Peak

Tesla Weekly (9/27): The hype over Q3 deliveries & Robotaxi Day are presenting a high hurdle

This week’s topics include:

Tesla trading thoughts

The coming clown show called “Robotaxi Day”

Q3 delivery outlook

Why strong China deliveries aren’t necessarily positive

This week’s gainers are Chinese EV stocks; losers are US auto stocks

BYD surpasses GM as the best-performing auto stock this year; Rivian becomes the worst as NIO spikes on China’s stimulus package

Tesla Trading Thoughts

As of yesterday, Tesla was up 6.7% this week due to even more frenzied hype over its potential Q3 delivery beat on October 2 (see Figure 2 below), but more so because of the October 10th Robotaxi Day drawing nearer.

Most of Tesla’s Rise This Week Came on Monday: The spike in Tesla began on Monday with the stock rising by 4.9% to $250 on scant newsflow and a flat Nasdaq, but it was likely due to news of the SEC looking to sanction Musk coming out after market close last Friday: Tesla call buying usually surges when there’s negative news about regulators closing in on Musk or Tesla.

Monday’s Call Buying Was More Intense Than Usual: And like clockwork, Monday saw volumes in the weekly 250 and 260 calls explode to 143,168 (up 216% versus last Friday) and 68,121 (up 191%), respectively. While the trading volume in Tesla’s options usually start the week at low levels and end at highs by Friday, this Monday’s call options saw a decline of only 21.5% versus last Friday. The average since Tesla hit its near-term low of $192 on August 7th has been a 46.2% decline in call volumes on Mondays versus Fridays.

Goldmans Pumps Tesla Calls at a Higher Strike Than Their Price Target: The hype over Q3 deliveries and Robotaxi Day this week culminated with Goldman Sachs’ derivatives team recommending that clients buy Tesla’s October 25 expiry call options at the $255 strike. Note that Goldman’s auto analyst has a Neutral rating on Tesla with a target price of $230. Goldman’s derivatives team said that their auto analyst saw Q3 deliveries “in line with consensus of 460K” (the median buyside consensus is said to be 472,500). They also said that Robotaxi Day “could include details about an expected start for the service,” which is astounding given nearly a decade of Musk predicting start dates that came and went without any robotaxis. Trading volumes in Goldmans’ recommended Tesla Oct-25 calls at 255 strike spiked to 1,145 contracts on Tuesday (from only 446 contracts on Monday), to 1,032 on Wednesday and 1,480 yesterday (purely coincidental, I’m sure). I wonder if Goldmans’ derivatives team remembered to warn clients that Tesla’s Q3 earnings results are out on October 18th (a week before the expiry of the 255 calls that they’re flogging) and results might be somewhat unsavory.

I remained disciplined this week and refrained from adding to my Tesla short position. My rule is if earnings look weak, short the stock when its relative strength index (RSI) is at 70 or above (overbought) and buy cover as the RSI approaches 30 (oversold). Tesla’s current RSI of 66 is close to being overbought (the stock is up 33% in 7.5 weeks from its near-term low of $192). Q3 should see one of the most unprofitable Automotive gross margins on record unless Tesla sees a huge drop in battery material costs. As mentioned in last Friday’s Tesla Weekly, the aggressive low-interest-rate loans Tesla is offering in the US, China, and the UK should hit profits very hard, aside from other regional price cuts (see details here).

The Absurdity of Robotaxi Day

It should be noted that Robotaxi Day was not a well-planned event to showcase Tesla’s autonomous driving prowess. Rather, it was a fit-of-rage response from Musk to an April 5th Reuters scoop about Tesla having scrapped its new Model 2—a $25,000 compact EV that was highly anticipated due to a new production method that would allow it to be highly profitable despite its low price (see details in Section 2 of this April report).

Sales volumes were expected to scale from 500,000 to the millions and the Model 2’s high profit contribution could’ve been the saving grace for declining profits and volumes of the aging Models 3 and Y (currently 95% of global sales).

Hence the negative reaction in Tesla’s stock to the Reuters scoop, which was backed up by 3 internal Tesla sources and one supplier. Tesla plunged by 6.2% to $160 that morning before Musk tweeted, "Reuters is lying (again)”, which caused some dip-buying that led to Tesla closing down by only 3.6%.

That night, in what seemed like a revenge tweet, Musk announced, “Tesla Robotaxi unveil on 8/8”. I have no doubt that Tesla’s engineers panicked when they heard this news. Despite August 8th being four months away, Tesla ultimately had to delay the event until October 10th due to further needed preparations.

Below are a few points to consider ahead of Tesla’s Robotaxi Day on October 10. It’s hard to imagine Musk pulling this off without beclowning himself given how weak Tesla’s Full Self-Driving (FSD) software is and how far away they are from catching up to rivals like Waymo (see details below) which already has 100,000 paid robotaxi rides per week now.

My gut feeling is that Musk will be forced to show concept models for upcoming new model launches at the event to divert questions about when Tesla’s robotaxi network will launch or have its “Optimus” humanoid robot do some fancy tricks on location at the Warner Bros. studio.

Warner Bros. Studio Being Used To Narrow Chances of Error: Tesla is holding its Robotaxi event at the Warner Bros. Studio in Burbank, California. Why? Most likely to avoid embarrassment. Tesla is said to have mapped the entire area and its surroundings as of September 13, according to news reports. Ironically, this is exactly what hardcore Tesla fans criticize robotaxi-rival Waymo for doing, i.e. driving autonomously in a geofenced area. Tesla’s FSD technology can drive “anywhere”, they claim.

FSD Not Ready For Prime Time—Scathing AMCI Review: Tesla’s FSD received a horrible review this week by an independent automotive research firm called AMCI Testing. Its professional test drivers used FSD on 1,000 miles of driving which led to “over 75 interventions”, or once every 13 miles (21 km) on average (press release here). This is in stark contrast to Tesla owners’ crowd-sourced FSD data that last showed 101 miles (162 km) between disengagements. To see how shocked AMCI was by Tesla FSD’s lack of “self-driving” capabilities, this passage is worth reading:

“What's most disconcerting and unpredictable is that you may watch FSD successfully negotiate a specific scenario many times – often on the same stretch of road or intersection – only to have it inexplicably fail the next time. Whether it's a lack of computing power, an issue with buffering as the car gets "behind" on calculations, or some small detail of surrounding assessment, it's impossible to know. These failures are the most insidious. But there are also continuous failures of simple programming inadequacy, such as only starting lane changes toward a freeway exit a scant tenth of a mile before the exit itself, that handicaps the system, and casts doubt on the overall quality of its base programming”.

AMCI Testing press release, September 24, 2024

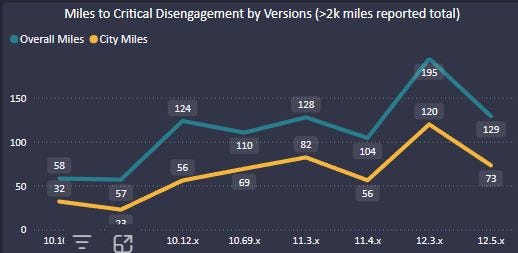

Waymo’s Rapid Advance Leaves Tesla in the Dust: Google’s autonomous driving unit, Waymo, reached 100,000 paid trips per week this month—without a driver. This is twice the rate recorded in June. Waymo’s robotaxis operate in San Francisco, Los Angeles, and Phoenix. Austin will soon see Waymo robotaxis and the company plans to expand its service to colder regions like upstate New York and Michigan next year to test how its system works on autonomous EVs in cold temperatures (Musk wouldn’t dream of doing this). Waymo reports roughly 17,000 miles (27,200 km) between critical disengagements whereas Tesla—which refuses to report its FSD data regulators—has around 101 miles (162 km) between critical disengagements, according to crowd-sourced data from Tesla owners who beta-test FSD (website here). Moreover, the current version of FSD (version 12.5) is so bad that it has gone back to August 2022 levels of range before disengagements despite Musk saying the previous version (12.4) would be 5x to 10x better in terms of miles between interventions than 12.3 (it wasn’t). Figure 1 shows the miles before critical disengagements by each version. The current version 12.5 is basically back to version 10.69 levels of range in between interventions in 2022.

Watch For Any Predictions of Timelines: For nearly a decade, Musk has predicted every year that all Tesla cars would be fully autonomous in the following year. On the Q2 earnings call in July again, he said, “You just literally open the Tesla app and summon a car and we send a car to pick you up and take you somewhere,” implying that Tesla would be running a robotaxi network to which Tesla owners could rent their cars out, “a bit like Airbnb”. Given that Tesla’s FSD software can only drive while supervised for 0.5% of the range before critical disengagement that Waymo can without a driver, the question is “when?”. Even if Musk puts out yet another timeline for this, it may fall on deaf ears and even cause a sell-off in the stock the next day.

Figure 1: Tesla’s Current FSD Version Reverts Back to 2022 Levels

Source: FSD Community Tracker (teslafsdtracker.com)

Q3 Delivery Beat Is Largely Factored In

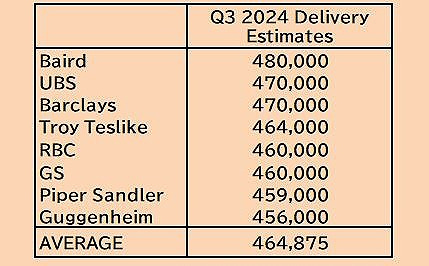

Barclays and UBS came out with notes on Monday both forecasting Q3 deliveries of 470,000, which is a 1.7% overshoot of consensus estimates of 461,964. This poured fuel on the fire in the already hot options trading on Monday, helping Tesla rise by nearly 5%. My gut feeling is that unless we see a Q3 delivery print of around 480,000 and decent deployment of Energy storage products (around Q2’s 9.4 GWh), Tesla may not rise that much. The current consensus based on 9 estimates reported this week (see Figure 2) comes to an average of roughly 465,000, which is 1.6% below the buyside’s median estimate of 472,500 (according to UBS, the buyside’s bullishness on Q3 deliveries ranges from 465,000 to 480,000).

Figure 2: Q3 Delivery Estimates By Broker

Note that in Q2, the buyside saw deliveries of only 410,000 to 425,000, or a median estimate of 417,500, which was quite bearish and 3.7% below Q2’s consensus of 433,397. After Tesla reported Q2 deliveries of 443,956, the stock surged by 10% not because it was 2.4% higher than the Street, but rather because it was 6.3% higher than the buyside consensus.

My Q3 estimate is 472,000 which assumes 173,000 for China, a generous 81,000 for Europe, a 5% QoQ decline in Asia/Oceania to 31,000, and sequentially flat volumes in North America and other small regions. Where I could be wrong is North America, where visibility is low compared to monthly and weekly disclosures in China and Europe. Regardless of the delivery numbers, Tesla’s heavy use of low-interest-rate loans in North America, China, and the UK this quarter compared to Q2, should negatively impact margins in Q3 (not to mention the €6,000 “special offer” on Model Ys sold in Germany and €4,000 for those sold in France).

Given Tesla’s high exposure to China and Europe—currently the two weakest auto markets in the world—it would be surprising if Tesla doesn’t see weak earnings despite its strong China numbers. Two key points regarding this:

Last week, the Mercedes-Benz Group (MBG) lowered its 2H 2024 operating profit guidance by 30%. This was not due to lower-than-expected volumes, but because of worse-than-expected pricing mostly in China. 25% of Tesla’s Q2 revenues came from China.

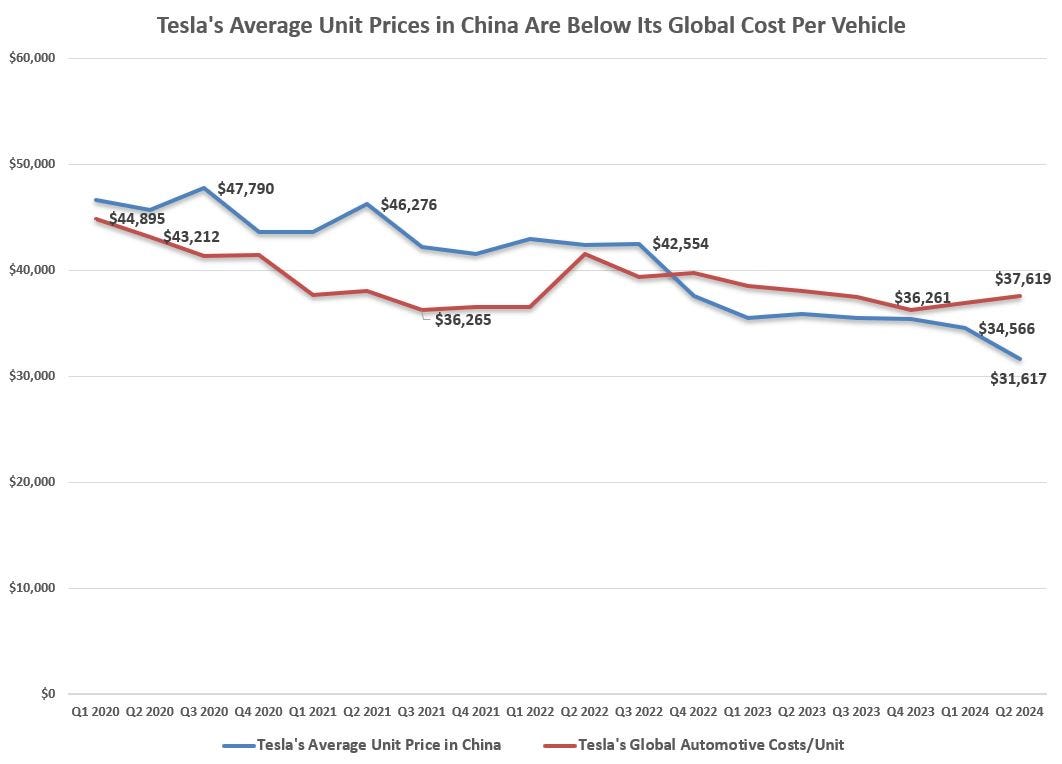

Figure 3 shows Tesla’s average price per vehicle in China compared to its global automotive cost of goods sold per unit. While dollar prices in China per vehicle are below Tesla’s global costs per unit, this doesn’t necessarily mean Tesla is losing money on its local sales in China. Costs of components, lineworker wages, and logistics are much lower than the rest of the world, which allows Tesla to charge only $31,617 per unit on average. However, 3 months of 0% loans for 5 years in Q3 could push local sales into the red. And it does mean that any upside in local sales volumes may not have much (or any) impact on profits. Note that in Q2, the average price of a Tesla in China was $31,617, which was 37% below the average price per unit of $50,036 for Teslas sold in the rest of the world.

Figure 3: Tesla’s China Prices Lower Than Global Cost Per Unit

Source: Company data & CPCA

Huge Reversals for China vs US—Morgan Stanley Made a “Stealth Pump” on Tesla by Downgrading its US Rivals

Chinese EV Stocks Soared This Week: China launched a stimulus package this week which led to an 11% rise in China’s CSI 300 index, lifting key Chinese EV stocks with it. China is caught in the same deflationary malaise that Japan was back in the early 1990s (i.e. a deflationary phase where cash flow either paid back debt or got tucked under the mattress in expectation of lower prices).

It’s no surprise that some saw this week’s huge surge in the Chinese stock market attributed more to short-covering by hedge funds and right-sizing by long-only funds from underweight to equalweight. There was less organic buying due to the stimulus package being lower than expected, according to local commentators.

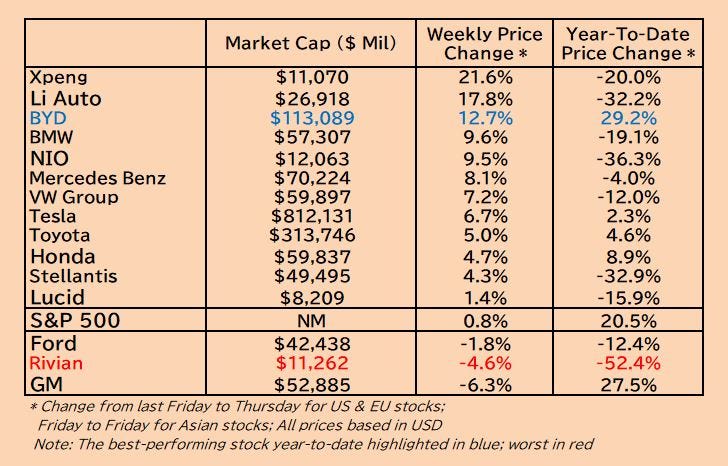

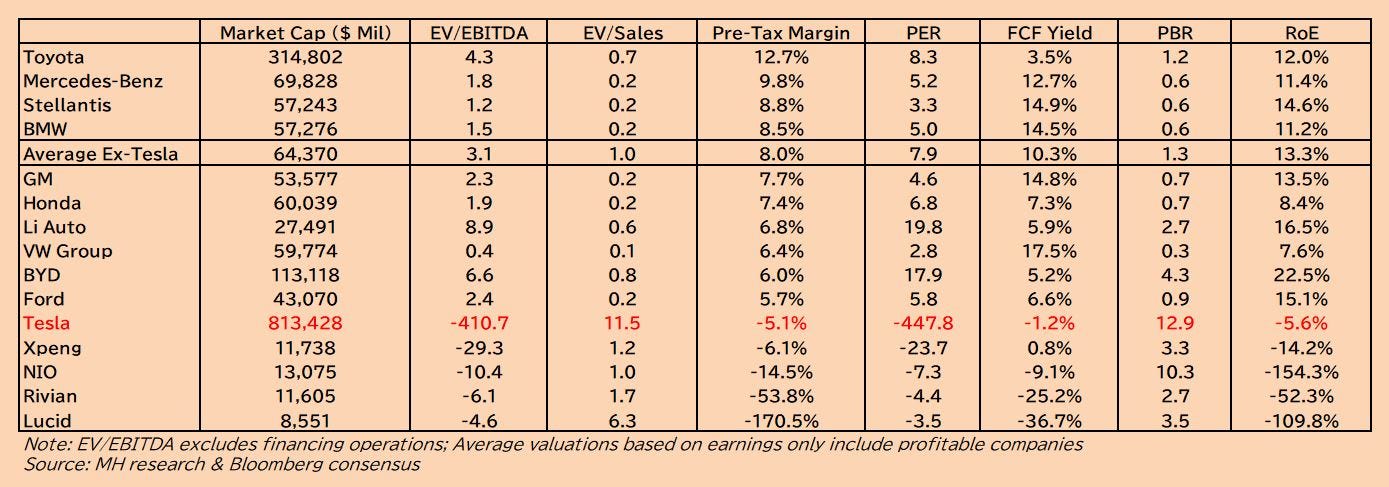

Nevertheless, the stimulus package led to Xpeng (+22% versus last week), Li Auto (+18%), and BYD (+13%) being this week’s top gainers in my global coverage. While Xpeng is the weakest among the 4 Chinese carmakers under coverage, its rise was likely due to short covering or “mean-reversal” buying. On an EV/Sales basis, Xpeng at 1.2x 2025 estimates and NIO at 1.0x are the most expensive Chinese EV stocks despite their losses, while BYD (0.8x) and Li Auto (0.6x) are the least expensive while being profitable. For reference, Toyota’s EV/sales ratio is at 0.7x 2025 estimates while generating the highest pretax profit margin among those under coverage in Figure 5.

This rise in Chinese auto stocks this week led to NIO going from worst to second-worst performing auto stock year-to-date (leaving Rivian to be the worst performer), while BYD became the best-performing auto stock YTD, replacing GM.

US Auto Stocks Dropped This Week Due to Morgan Stanley: The bank that has lent the most money to Elon Musk with his Tesla shares as collateral downgraded GM (from “Neutral” to “Sell”), Ford (from “Buy” to “Neutral), & Rivian (from “Buy” to “Neutral”) this week due to Chinese competition and growing weakness in the US auto market. Morgan Stanley left its “Buy” rating on Tesla unchanged despite Tesla facing stronger headwinds than all of the above.

Aside from Goldmans’ call option pump this week, Morgan Stanley’s blatant favoritism towards Tesla is another sign of how egregious this Tesla bubble has become. Unlike Goldmans, Morgan Stanley is more tied to Musk’s hip due to its massive margin loans to him based on his Tesla shares and the $3.5 billion of LBO debt it issued to finance Musk’s buyout of Twitter in 2022.

Morgan Stanley’s reasons for downgrading Tesla’s US auto rivals happen to be more pertinent to Tesla:

“The China capacity ‘butterfly’ has emerged and is flapping its wings. China produces 9 million more cars than it buys, upsetting the competitive balance in the West.” This word salad applies more to Tesla than it does to GM and Ford—which are already losing money in China—or Rivian, which has zero exposure to China. Tesla has brand-new facilities in both China and Europe, whereas GM and Ford have joint-ventures that share the profits and losses.

“US vehicle inventories are rising, and prices of new vehicles are getting out of reach for many…credit losses and delinquencies continue to trend upward for less-than-prime consumers.” Once again, this probably hurts Tesla more than its US rivals given that the US is its most profitable market on a local-sales basis. Finally, Tesla’s aging model lineup needs more support in the US than its rivals as each new model has a one-year head start in the US market after launch.

Tesla is the most insane, publicly traded asset I’ve ever seen in my investing career, even when compared to the spastic dotcom stocks in Q1 of 2000. I can only write about Tesla in this much detail every week because I’ve lost a lot of money trading it since 2016.

Despite all of the distortions from central banks, a pandemic, and price manipulation via the options market since 2020, I’ve also never been as confident that “this time” I might be right if I remain disciplined.

Happy Friday.

Figure 4: Auto Stock Weekly Gainers & Decliners

Source: Bloomberg

Figure 5: Tesla 2025 Profitability & Returns vs Rivals (By Pretax Margins)

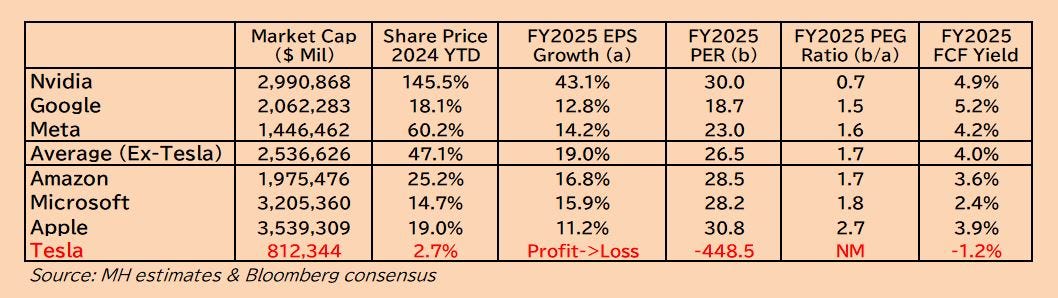

Figure 6: Tesla 2025 Profitability & Returns vs Magnificent 7 Rivals (By PEG Ratios)

That FSD report is shocking. Great report as ever Brad.

Again, could sound like a big time dumbass, but I think the sell off starts next Monday/Tuesday and catches bulls offside who think we're going to get a repeat of the last deliveries rally and/or a straight rally into robotaxi. Think we see 150 by EOM. Could definitely be wrong. But there's upwards of 4-5 "sell the event" events, including deliveries, robotaxi, earnings, SEC/twitter thing, and a McCormick ruling (unsure of the date, doubt it will be October at this point but needs to be remembered) that forces Tesla to (hopefully) recognize a legal contingency in the billions.