Tesla Weekly (9/20): Lower Interest Rates Won't Help

Tesla Weekly (9/20): Lower Interest Rates Won't Help

The Fed's 0.5% cut in interest rates can't help Tesla's stale model line-up, but it did help the stock price

This week’s wrap-up is mainly about 2025 consensus earnings estimates versus the current share price. Tesla is the most out-of-whack stock among its rivals in both the auto industry and the Magnificent 7.

Don’t miss the comment at the end about why Tesla’s Full Self-Driving (FSD) product is a dud and doesn’t warrant a valuation premium at which Tesla trades.

This Week’s Main Points

Tesla was down by 1.3% through Wednesday after the FOMC meeting but surged by 7.4% yesterday along with other junk stocks like Carvana, Peloton, etc. due to the Fed’s 0.5% cut in interest rates.

Tesla’s 5.9% rise this week through yesterday was the third biggest gain among the major global auto stocks after Li Auto (+11.2%) and Toyota (+6.4%), and the second largest increase among The Magnificent 7 after Meta (+6.6%).

This week’s wrap-up will be easy, starting with Tesla trading thoughts and winding down with key charts and tables that should assure Tesla bears that they’re not wrong and provide food for thought for Tesla fans.

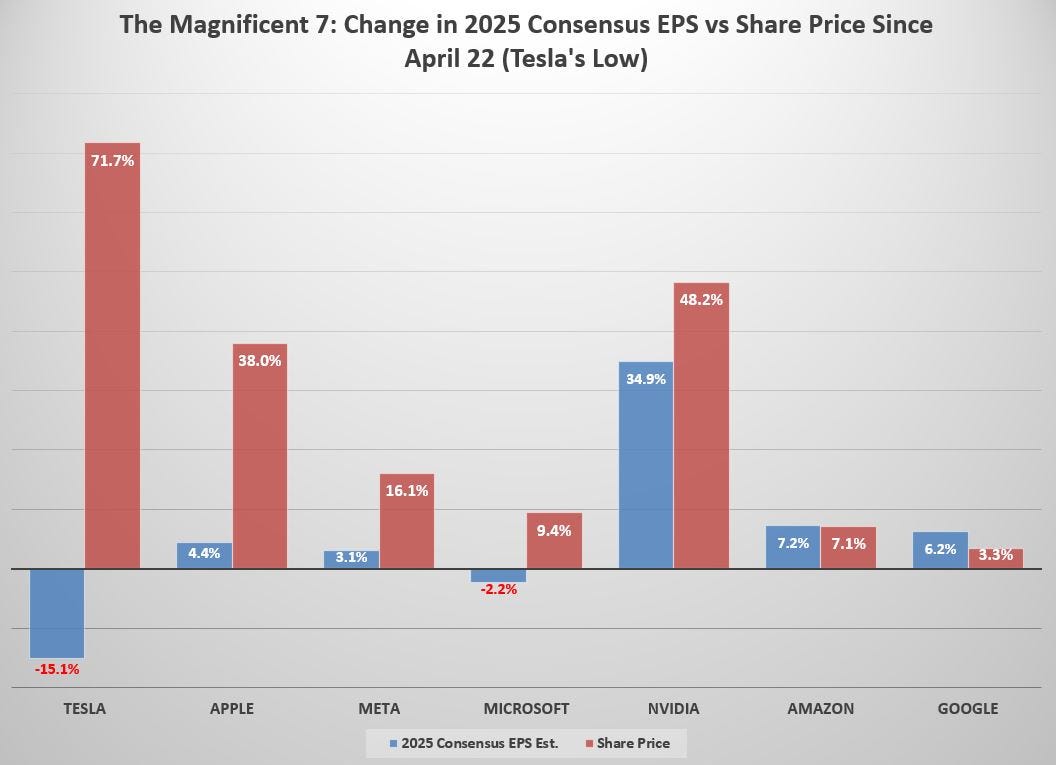

The most important chart this week is Figures 5 and 6 below: Tesla’s share price has surged by 72% since its $142 low on April 22, while its 2025 consensus EPS has dived by 15%. I’ve never seen anything so insane in my investing career.

Tesla Trading Thoughts

Once again, call option buying this week pushed up the share price. Buying of weekly call options supported the share price as it declined through Wednesday’s FOMC meeting and then propelled it yesterday.

The weekly 230 and 235 calls were the biggest traded options between Monday and Wednesday while Tesla was weak.

But yesterday’s 7.4% spike in Tesla’s stock was largely fueled by huge volumes in the 240 and 245 calls expiring today (171,533 contracts and 145,641 contracts traded, respectively). Figure 1 shows yesterday’s most highly traded Tesla options.

My trading rule on Tesla—which has worked like a charm if you’re disciplined—is to buy (or cover your short) when Tesla’s RSI approaches 30 (oversold) and sell (or short) when it’s near 70 (overbought).

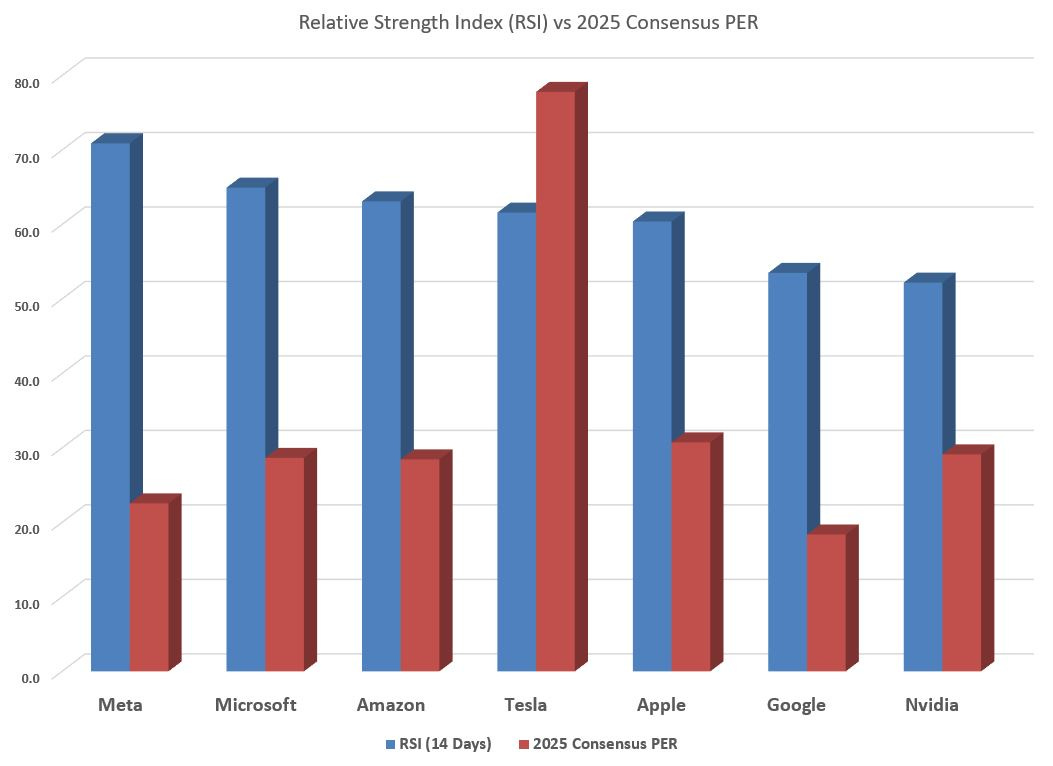

Tesla is now at 62, which is getting close to the 70 “overbought” level. And its 2025 PER is the highest among the Magnificent 7 (see Figure 2).

I was an undisciplined trader this week, albeit in small size. I shorted more Tesla intra-day on Wednesday at $233 after it spiked on the FOMC minutes and “revenge” shorted a bit more yesterday at $242. I’m still not fully loaded but plan to fill my boots by “Robotaxi Day” on October 10th.

The Tesla events that I’m happily shorting into are (a) the Q3 delivery report on October 2nd (estimate); (b) Robotaxi Day on October 10th; and (c) Q3 earnings on October 18th (estimate).

Figure 1: Largest Traded Tesla Options On Thursday

Source: Bloomberg

Figure 2: Tesla’s RSI Ranks in the Middle of The Mag-7 But Has The Highest 2025 PER (Ranked From Highest to Lowest RSI)

Source: Bloomberg

The Insane Disconnect Between Tesla’s Declining Earnings Estimates & Its Soaring Share Price

Tesla hit a low of this year at $142 on April 22nd just before it reported worse-than-expected Q1 earnings results (see report here). The RSI on April 22 was 27.8 (oversold) and despite the bad Q1 results, Tesla rallied by 34% over the next 4 days (helped by Musk having a “surprise meeting” with CCP officials in China and then news about FSD being accepted there [debunked as false thereafter]).

Tesla is now up 72% above its April 22nd low of $142 and this would make sense if consensus earnings estimates for 2025 were rising. But they’re not. In fact, they’ve dropped by 15% since then.

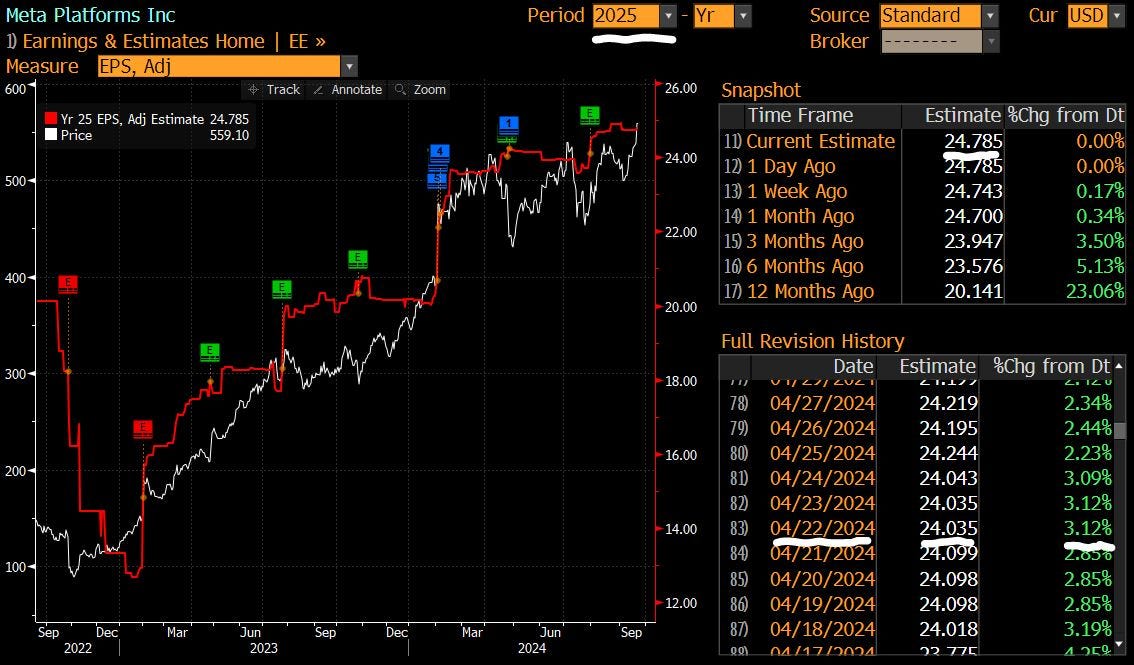

Figure 3 shows what this disconnect in Tesla looks like on Bloomberg and Figure 4 shows what a proper rise in Meta’s share price shows when adjusting to higher 2025 consensus EPS estimates.

Among the Magnificent 7, only Tesla and Microsoft have declining 2025 consensus EPS estimates since April 22 while their share prices rise. But Microsoft’s share price rise of 9% since then versus its 2% decline in FY2025 EPS outlook is mild compared to Tesla’s 15% drop in estimates and its 72% spike in the share price (see Figures 5 and 6).

Figure 3: Tesla 2025 EPS Consensus vs Share Price is Out of Whack

Source: Bloomberg

Figure 4: Meta’s Share Price Rising into its Higher 2025 Consensus EPS Estimates

Source: Bloomberg

Figure 5: Magnificent 7 Changes in 2025 PER Since April 22 (Tesla’s Low of the Year)

Source: Bloomberg

Figure 6: Tesla’s 2025 Consensus EPS Drops the Most While its Share Price Rises the Most Among the Magnificent 7

Source: Bloomberg

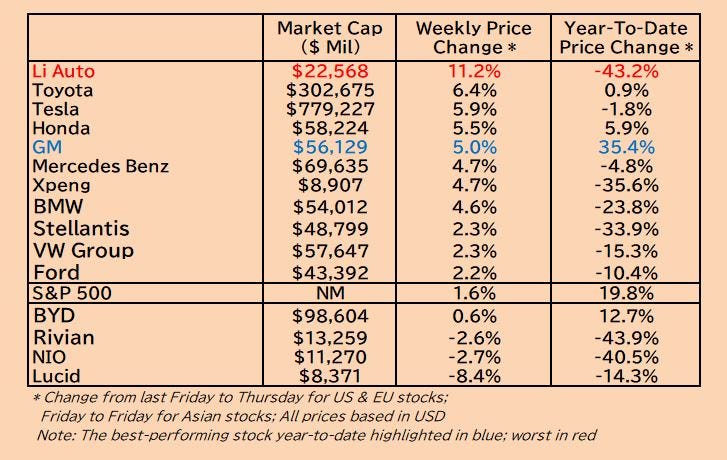

Weekly Auto Stock Gainers & Losers

This week’s gainers and losers are literally a reversal of last week’s winners and losers. The key stocks worth keeping an eye on are as follows:

GM is the best-performing major auto stock this year at +35% YTD. Could it be 2025’s weaker-performing auto stock?

Li Auto is the worst-performing auto stock this year due to profits falling after introducing loss-making BEV models this year (they had higher profits last year due to only making extended-range hybrids, which have higher profit margins than BEVs). It is the only profitable EV maker after BYD in China, so look out for a potential bounce if 2025 earnings look improves.

Figure 7: Weekly Share Price Performance Among Tesla’s Main Rivals

Source: Bloomberg

The FSD Thing About Tesla—It Doesn’t Make Sense

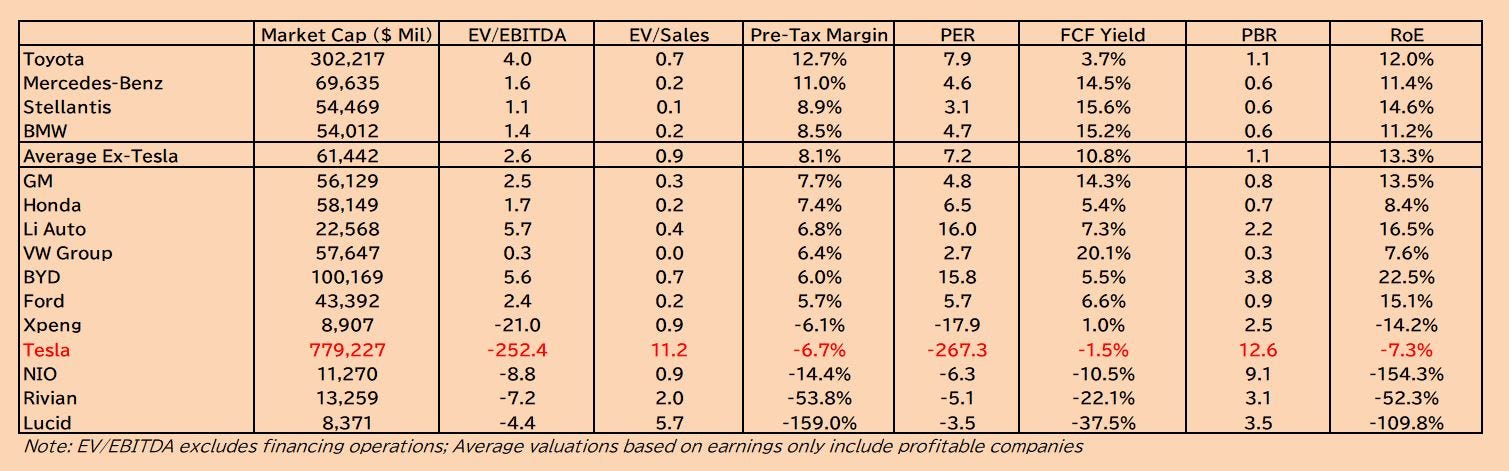

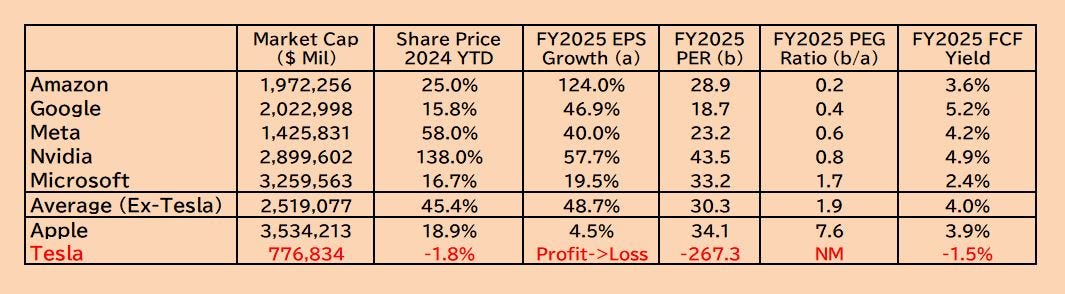

No matter how you look at it, Tesla is massively overvalued versus both its auto rivals (see Figure 8) and its AI rivals (see Figure 9). Despite clearly deteriorating auto fundamentals, Tesla’s valuation is still 2.5x Toyota’s because of (a) Musk’s continued mantra of Tesla being an “AI/robotics” company and (b) the stock price being pumped via its options market.

On Tesla being an “AI” company, let me just say this: Tesla’s Full Self-Driving (FSD) system is what Musk points to as Tesla’s main AI “edge”. It’s merely a Level 2 driver-assist product which is a “dime a dozen” feature among carmakers in China (prices are on average $1,500 versus Tesla’s FSD price of $8,000). Two key points to consider regarding Musk’s claim that FSD is the differentiating factor between Tesla being more than a carmaker:

The April 25th report from the US National Highway Traffic Safety Administration (NHTSA) showed that FSD had 75 crashes and one fatality during its investigation into FSD between August 2022 and August 2023 (link to NHTSA’s report here).

Google’s Waymo—the leading robotaxi company in the US—had only 4 crashes in 2023 and no fatalities.

Tesla has yet to apply for robotaxi testing permits, as attested to by California’s two main regulators (details in this article here).

In light of these three points regarding FSD, it’s hard to understand how big institutions could hold or buy Tesla given its deteriorating auto business (87% of gross profits).

More on this later, but refer to Figures 8 and 9 to see just how much of a premium Tesla receives both amid its auto rivals and AI rivals.

Figure 8: Tesla’s 2025 Returns & Valuations vs Auto Rivals (Ranked by Pre-Tax Profit Margins)

Source: Company data, Bloomberg, and MH estimates

Figure 9: Tesla’s 2025 Returns & Valuations vs Its Magnificent 7 Rivals (Ranked from Cheapest to Highest PEG Ratio)

Source: Company data, Bloomberg, and MH estimates

great stuff brad.

clearly agree on the options pump w/ this stock. couple add'l observations if interested.

* IMO the move thur was A) MFO pump via OTM +Cs (your screen print nailed it--note volumes of 240-245+Cs), B) some index buying and C) underperforming fund mgrs buying high beta in an attempt to catch up and D) some short covering---but weight is overwhelmingly A)

* at present (9am cst Fri) sure looks like MM's are going to wipe all the +Cs 240+ at expiry today. --downside is that big OI at 230 is going to finish ITM, so MFO trading is not just a cash out across strikes.

* for the biggest single day move since July gamma squeeze, trading volume in TSLA (~ 100MM) lags badly vs what happened in July (~ 200MM)...Thurs had ~ 1.5MM +Cs trade, july would see ~ 2.5MM.

these gamma squeezes he tries work best with high short interest along with index buying. --i cannot validate how short the market is (as i dont trust timeliness of BM function "SI" <GO> but presently S3 Squeeze is 45---which is likely stale).

this is a total house of cards, and it just needs a catalyst to topple the levered buying support that is easy to overwhelm (9/6)---a correction / bear market would do it. trouble is powell is elon's best friend.

he's clearly not selling shares in Sept yet, not with the option pump. makes me think he's goosing the shares to increase his borrowing base to get credit for his twitter interest payment (which is > revenues).

ridiculous stock. crazy making. really appreciate your efforts brad as a voice of reason..

I also shorted more yesterday, right at 242.10. Impossible to know how high it can thrust but theyre running out of time, only a few weeks out from the big events now. Im still not fully convinced that robotaxi event even happens. That yellow car looked like a 3d printed toy car. Are they really going to showcase THAT with a dogshit L2 FSD? Deliveries I mean...a strong Asia probably cannot cancel out weak volumes in both NA and EU? And Elon. He's gone completely off the rails. Q3's gotta have nightmare numbers in store.