Tesla is No Longer a Growth Stock But Still Valued as One

Tesla is No Longer a Growth Stock But Still Valued as One

Deliveries slumped by 8.5% YoY in Q1 but the stock only fell 5%; Cash burn has yet to be factored in

I now have Tesla’s 2024 deliveries down by 9.3% YoY to 1.64 million units (consensus is at 1.99 million units).

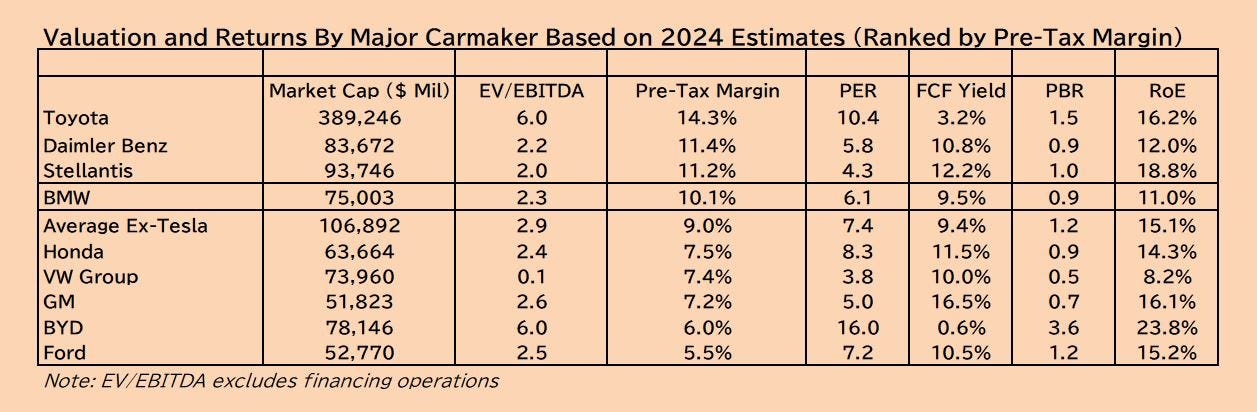

My Q1 EPS estimates are now $0.36, or 40% below consensus estimates of $0.59. My full-year Tesla EPS estimate is $0.98 versus the consensus of $2.89. If I’m right, anyone buying Tesla right now (like Ark Invest) is fine with a PER of 289x versus the average of auto stock valuation of 7.2x (see Figure 2 below).

Tesla’s Q1 deliveries were down by 8.5% YoY to 386,810 units in Q1 and production was down by 1.7% YoY to 433,371 vehicles. This is the first time since the pandemic in Q2 2020 that Tesla has seen sales and production decline on a year-on-year basis.

Showing how stupid they are, Tesla blamed the weak deliveries on the Red Sea crisis and the arson attack on their factory in Gruneide. This excuse belies the fact that production was 12% higher than sales.

With production at 46,561 units over deliveries, it’s also the largest inventory build since Tesla’s IPO. By my count, Tesla now has inventory of around 171,000 vehicles which amounts to 44% of Q1 deliveries or 34% of Q4 2023 deliveries.

Main points About Q1 Deliveries:

First and foremost, I apologize for insinuating that Tesla might bounce due to having been oversold and possibly seeing 410K or more deliveries in Q1. It’s oversold for a reason and that was made clear today.

The stock only fell by 4.9% despite Q1 deliveries being down 8.5%. This is a sign that dip-buyers are still in power and the market is still under QE influences.

The FSD pump (which I wrote about last week here) is not working. And it’s no surprise as it costs $199/month to subscribe to or $12,000 to buy up front. Most car buyers could care less about “self-driving”.

Desperation

Tesla literally hit the gas pedal at their factories worldwide and produced cars that were 12% in excess of demand. This is as erratic as Musk seems to be on Twitter.

Tesla blamed their sales decline in Q1 on deliveries being short-handed due to the Red Sea terrorism (which held back battery pack shipments from China to the EU) Tesla also blamed an arson attack on their factory in Grunheide as a reason for the bad results. Nevertheless, production outgrew sales in Q1 by 12%, which is quite an embarrassment. Any normal company would fire their PR chief for allowing that to be published.

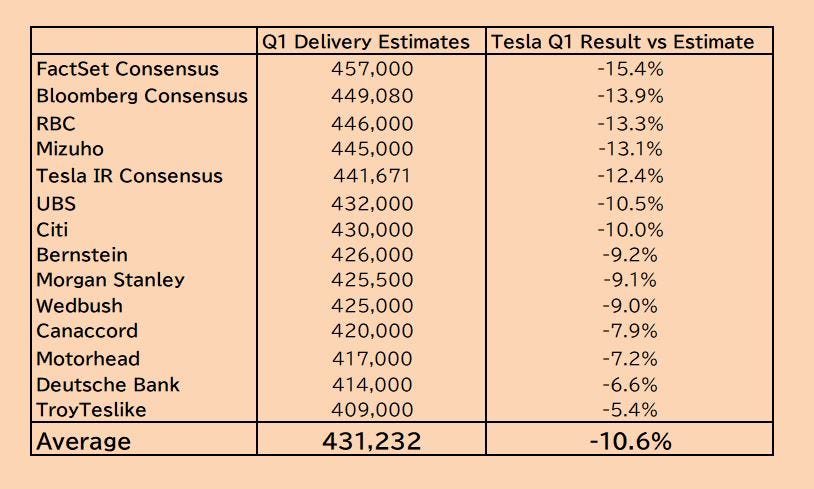

TroyTeslike was the best indicator this quarter (as usual) and there’s no reason to not be subscribed to his Patreon after this quarter. He got slammed by the $TSLA fanboys for simply telling what he felt. And he was more correct than any of the estimates in Figure 1.

Figure 1: Consensus Q1 Deliveries vs the Result

Q1 Sales are Down Across the Board

For anyone thinking of shorting Tesla, here’s a huge catalyst: Tesla’s China sales. Rivals with much better cars than the Model 3 (Xiaomi’s SU7) have received 120,000 orders for their new cars. The Model 3 in China sold around 148,000 last year. Tesla reportedly cut production in China by 23% from 6.5 days a week to 5 days a week…this is not factored into Q2 or 2024 estimates.

Tesla Will Have to Finance to Survive—15% Dilution at Least

The fact that Tesla shares only fell by 4.92% today is insanely contradictory to the fundamentals (nothing new).

What the share price didn’t factor in today was that Tesla might have to finance this year. They already did last year with around $3 billion in ABS-linked deals in the 2H of 2023. I’m sure they’ll do more this year.

If Musk were smart—he’s not—he’d do a 15%-20% equity offering at Tesla’s current market cap. I’d cover my short if he did. But he’s not as smart as Ford was back in 2008.

Figure 2: Valuations & Returns (Ranked by Pre-Tax Margins)

I've been working on a report on how $TSLA could go BK if demand falls really hard. It's more relevant than ever now.

Comp trial will be in August. Shareholders' vote before that is more important. I think that they finally send Musk a pink slip.