Tesla's Bad Q1 is Well Flagged, But Here's What to Watch for on Tuesday

Tesla's Bad Q1 is Well Flagged, But Here's What to Watch for on Tuesday

Depending on how Musk explains the future product pipeline of Tesla's EV business, any pumping of "robotaxis" should be met with selling pressure

Tesla’s Q1 earnings call on Tuesday is the most highly anticipated call for the embattled EV maker since its IPO in 2010. This is because Reuters reported on April 5th that Tesla has scrapped the long-awaited Model 2—a low-cost, high-volume EV—and will instead focus its resources on robotaxis.

Because Tesla is struggling with an old model lineup that requires constant price cuts to stay alive, many Tesla investors had hung their hopes on the Model 2 launch, which Musk in January said would be in the 2H of 2025. News of this switch from Model 2 to robotaxis appalled most Wall Street analysts who lowered their estimates in the following two weeks.

The term “thesis-changing” is now widely used in describing this huge—yet unannounced—pivot at Tesla and it’s understandable why: 94% of gross profits still come from the car business and there is nothing to show for with regard to “robotaxis”. Hence the bated breath with which Wall Street awaits Tuesday’s earnings call.

Below are three sections: (1) what to look out for in the earnings results; (2) how to look at (recent) consensus estimates versus mine; and (3) what factors to beware of if you’re short Tesla.

Things to Watch for in the Numbers & on the Call

Deferred FSD revenue recognition could be huge: The biggest question is how much deferred FSD revenues Tesla books in Q1, given that recognition depends on (a) technological milestones achieved and (b) the number of customers FSD beta is rolled out to.

During Q1, Tesla rolled out multiple new versions and changed the term “FSD beta” to “FSD (supervised)”, which implies it’s no longer in beta stage even though it still drives into oncoming traffic. Everyone expects Tesla to book deferred FSD revenues, but the question is how much.

In its 2023 10-K, Tesla said that it plans to book $926 million in deferred FSD revenues over the next 12 months. Because Q1 is a trainwreck of a quarter for Tesla, some believe that Tesla will book all $926 million in one go for Q1, but this may not be possible without the auditor’s approval. This is why I assume that Tesla booked $450 million in Q1 to pad weak profits and spreads the rest out over the rest of this year.

We won’t know exactly how much Tesla booked on the day of earnings results as they only disclose FSD-related information in the 10-Q which comes out a week or so later. If average auto revenues (ex-credit, ex- leases) per unit are rising on a QoQ basis, this is a sure tell that the booking was huge.

Note that deferred FSD revenues are a non-cash item so won’t impact free cash flow (FCF).

Pure auto revenues (ex-credits; ex-leases) should fall by 2.7% QoQ: This assumes a 3% decline in China ASPs and a 4% QoQ drop in rest-of-the-world ASPs. Once again, if the ASPs rose QoQ in Q1, it’s a sure sign of Tesla having booked a large amount of deferred FSD revenues.

Cost/unit should rise due to Germany & Cybertruck: There were 2 cost headwinds in Q1 that should increase the cost of goods sold (COGS)/unit in Q1: (1) a 2-week shutdown of the German plant due to the rerouting of parts shipments from China to Germany; and (2) start-up losses from the Cybertruck launch.

I estimate the 2-week shutdown of the German plant cost Tesla $300 million in Q1. The Cybertruck cost Tesla another $190 million assuming that each Cybertruck sold had $45,000/unit in gross losses (this is conservative, as Rivian only lost $43,000/unit on 14,000 deliveries, while Tesla only delivered around 4,000 Cybertrucks in Q1).

These two factors cause my COGS/unit estimate for Q1 to only rise by 3.7% QoQ, which seems optimistic: when Tesla shut down its Shanghai plant due to the COVID breakout in Q2 2022, it caused COGS/unit to jump by 13.7% QoQ.

Tesla likely sold their Bitcoin in Q1: Given the need to pad profits in Q1 more so than ever before, it’s hard to imagine that Tesla didn’t sell the remaining 10,000 coins they had when Bitcoin rose to the $60,000 handle in March. Using the average price of Bitcoin in March ($53,537), I estimate that Tesla booked a $235 million gain by selling their remaining 10,000 Bitcoins.

From 8% to 24% tax rate will stunt EPS growth in 2024: Tesla will be paying higher taxes in the US and China, which combined, made up 69% of global revenues last year. In the US, Tesla never paid taxes up to now but will do so from Q1. In China, Tesla’s tax rate went from 15% last year to 25% as of the start of 2024. Assuming the US tax rate is 20%, the blended tax rate in 2024 should be around 24.1% which is significantly higher than 8.3% in 2023.

FCF should be negative, but who knows what levers Tesla pulls: Given that Tesla’s Q1 output was 12% higher than its deliveries, Q1 FCF should be negative. Tesla hasn’t had a negative FCF since Q1 2020. In light of this and the fact that Tesla likely needs to finance after Q1 results are out, I wouldn’t be surprised if FCF was break-even or slightly positive. Among the recent downgrades on the Street, Morgan Stanley, Barclays, and JP Morgan all forecast negative FCF in Q1. My Q1 FCF estimate of -$1.5 billion is 69% higher than (recent) consensus estimates of -$0.9 billion.

Consensus is Duly Bearish for Q1 but too Optimistic for 2024

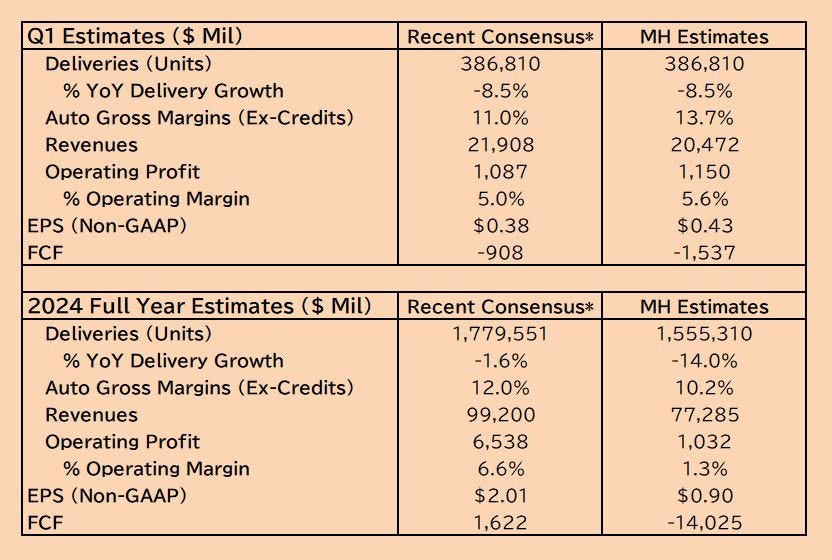

Q1 Non-GAAP EPS estimates are low enough: The Bloomberg consensus estimate for Q1 non-GAAP EPS is $0.52, but most of these analysts haven’t published their revised forecasts after a huge delivery miss was announced by Tesla on April 2.

Mind the Morgan Stanley gap: The more recent consensus (see Figure 1) has Q1 non-GAAP EPS at $0.38, which is 12% lower than my estimate of $0.43. It should be noted that Tesla’s biggest cheerleader on Wall Street—Morgan Stanley—has the lowest EPS estimate of $0.20, which is likely a low-ball number to give Tesla a low hurdle for Q1. Stripping out the “Adam Jonas” low-ball estimate of $0.20, the Q1 “recent” consensus is $0.45 for non-GAAP EPS, which is largely in line with my estimate of $0.43.

Also, while my operating margin estimate of 5.6% is higher than the Street’s 5.0%, I may be assuming a higher rate of deferred FSD revenue recognition than the Street is (I’ve got $450 million in Q1 vs planned recognition of $926 million for all of 2024).

Full-year estimates are still out to lunch: While the brokers in the “recent consensus” may be close to my estimates for Q1, their full-year EPS estimates are 123% higher than mine. All of them—including the bears—see deliveries and earnings going up and not stopping after Q1. The fact that consensus sees 2025 and 2026 deliveries and earnings growing despite no new model launches is proof of how much further Tesla’s shares could drop as the Street becomes more realistic.

Figure 1: Consensus Estimates vs My Estimates

* Recent consensus is made up of revisions published after Q1 delivery results, including Morgan Stanley, Barclays, JP Morgan, and Mizuho.

Final Thoughts: Musk Could Squeeze the Shorts with One Positive Utterance

In the past 4 quarters, Tesla has dropped by an average of 10% the day after their quarterly conference call due to bad fundamentals and Musk’s flippant remarks on the calls.

While I expect Tuesday’s call to be even more bearish—there is no way Musk can wiggle his way out of this proclaimed shift to robotaxis without explaining how the car business will remain profitable—I am cautious given how much bad news has come out on Tesla in the past 19 days.

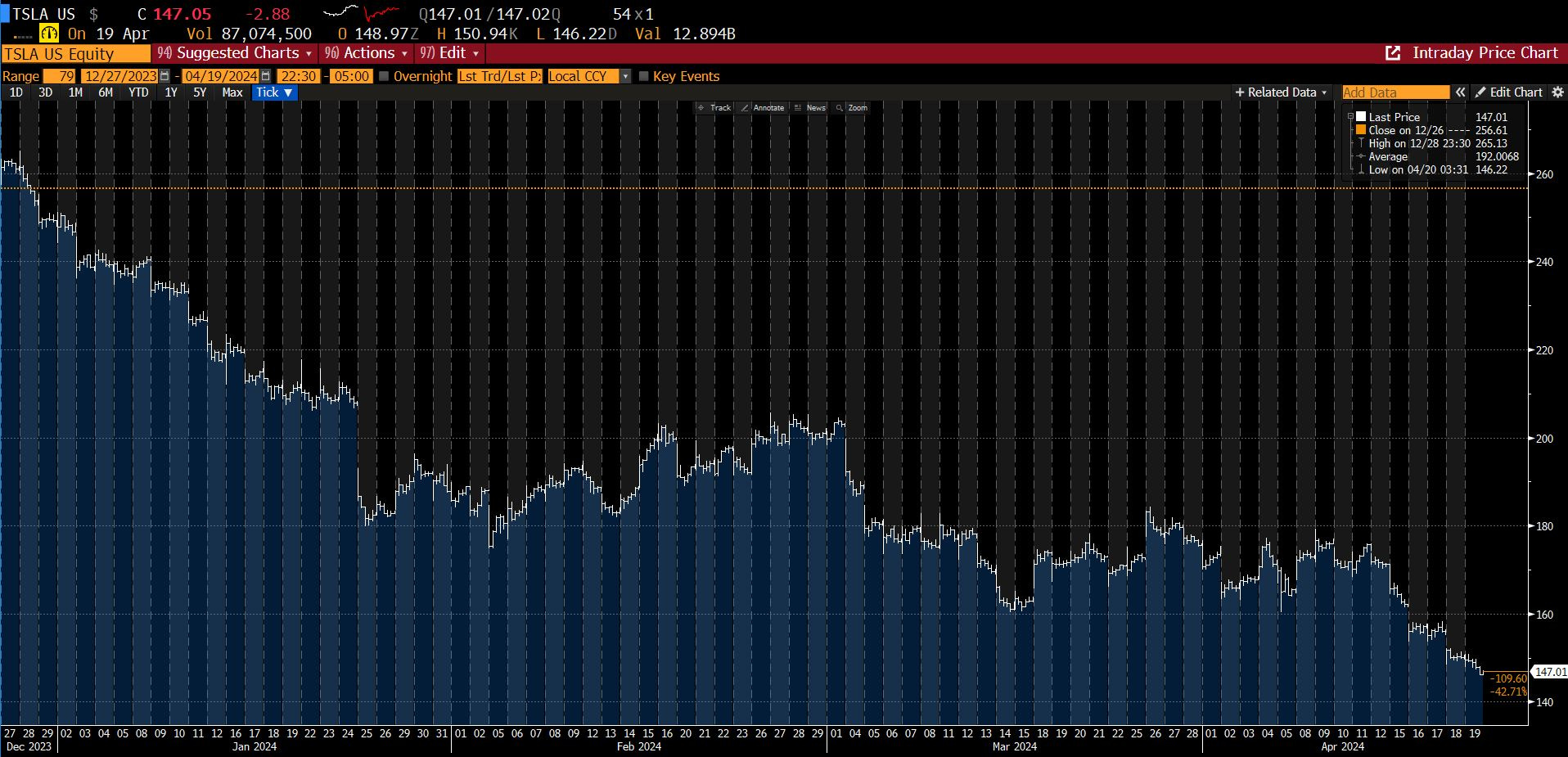

Tesla is down 41% year-to-date and 14% month-to-date on all the bad news that’s come out this year, especially since the April 2 delivery miss. Tesla’s RSI (relative strength index) is at 30, which indicates that it’s “oversold”, but it was at 27 in January when Tesla had a horrible earnings call where they gave no delivery guidance for the first time. The stock dropped by 12% the following day but wound up rallying 10% over the following 4 weeks in February.

What worries me about being too short for Tuesday’s earnings call are the following:

Musk needs the stock price higher: Tesla needs to raise cash (see Section 3 of my recent report on whether Tesla could go bankrupt here). This means Musk may try to pump the stock on Tuesday’s call. He did so on the Q4 2023 call in January 2023 when he justified his decision to cut global prices by 20% by saying “orders are currently 2x output” as a result. The stock jumped by 12% the next day despite horrible Q4 2023 results and Tesla missed its gross margin targets in all of the following quarters.

Being short Tesla, the one thing I would hate to hear is any talk (lies?) about the Model 2 still “being on the table for 2H 2025” or “just slightly delayed to 1H 2026”. This would turbo-charge the stock for a while, but I would short more into any such rally. Even if Tesla built the Mexico plant tomorrow, start of production wouldn’t happen until at least Q1 2026 at the earliest.

Bad sentiment could lead to institutional selling on any Musk pump: Since the start of this year, I’ve left money on the table by being too cautious around earnings and delivery results due to the stock already being oversold. The same goes for this results season, although I’ve realized that when things are as bad as they are now, the market sells Tesla off regardless of Musk’s pump on the call.

There is little that Musk can say to erase the bad image everyone now has of him being bored with the ailing car business and thinking a pivot to robotaxis can maintain Tesla’s egregious valuations.

If Musk doesn’t address the car business’s product strategy from here on, it doesn’t matter how “balls to the wall” Tesla goes on “autonomy” as there won’t be a solvent company at which Tesla can build robotaxis anymore.

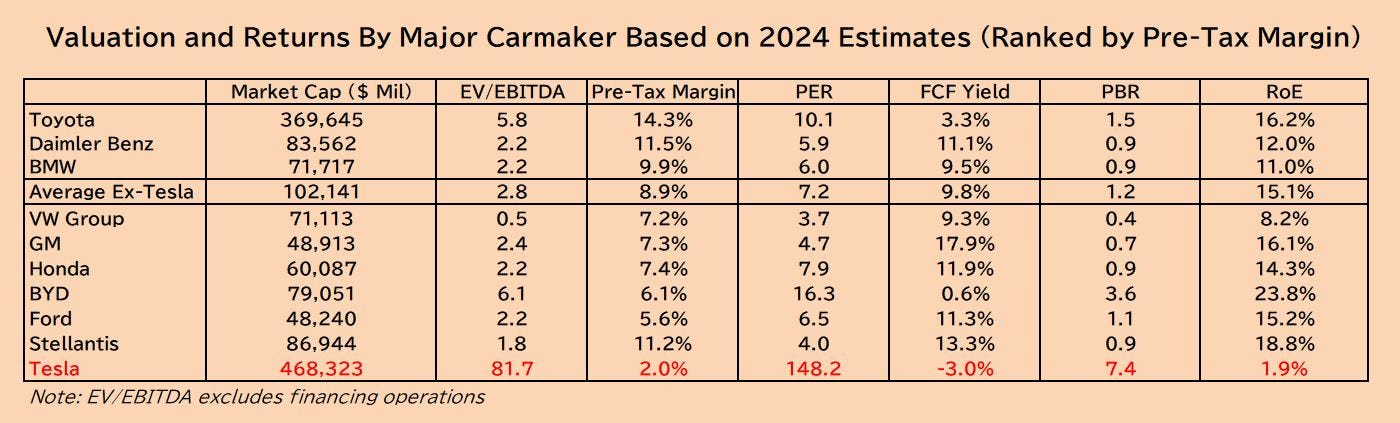

Figure 2: Tesla is the Most Overvalued Auto Stock

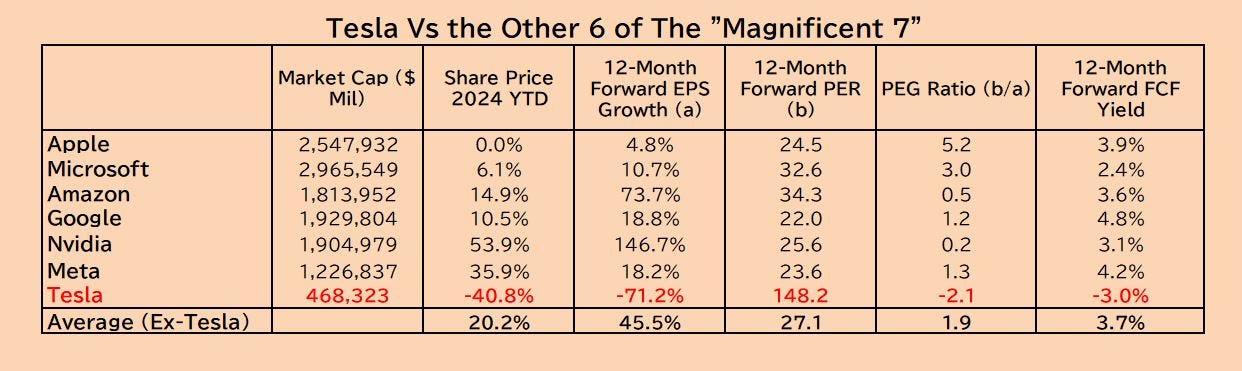

Figure 3: Tesla is the Most Overvalued of the Magnificent 7

Note: Nothing in this report is investment advice.

Regarding earnings I will just do nothing and hold my short position and puts. I find it too hard to guess what is going on in longs minds. The situation at Tesla is as bad as I can imagine. A bounce is always possible but hopefully would be short lived.

great post, Brad, thank you