[Quick Note] Tesla Up More on No News

[Quick Note] Tesla Up More on No News

2025 EPS estimates are down 41% year to date while the stock is up 2% on nothing but bad news; This is weird and deserves a short comment.

The charts and tables from Figure 1 to Figure 4 below are very useful in showing how the upside in Tesla is likely limited, so take a look at them if you don’t have time to read the update below.

Many investors are probably scratching their heads over the fact that Tesla was up 4.9% yesterday despite news after Friday’s market close that the SEC may sanction Musk for once again backing out of a court-mandated deposition last week.

Any bad news about regulators closing in on Musk or Tesla is usually met with heavy call options buying to keep the stock up. There are many examples of this, but the most recent one is the April 26 news of the US traffic safety regulator’s scathing report on Tesla’s 2023 Autopilot/FSD recall not having fixed key problems: Tesla fell as low as 2.2% on the news (despite the Nasdaq 100’s rise of 1.65%) but rallied into the close to finish down only 1.1% on the day.

Below are some possible reasons as to why Tesla spiked by 5% yesterday amid another day of no particular catalysts.

To me, it seems like Tesla’s chart is being painted by those who need the stock to remain high. Tesla is up 32% from its August 7th low of $197 just after bad Q2 results (missed Q2 Street estimates by 13.5%) which included regulatory credits of $890 million, which is free money for Tesla and was over 2x higher than consensus estimates.

A Q3 Delivery Beat Should Be Factored In

Barclays & UBS both predict higher than consensus Q3 deliveries: Both analysts put out notes yesterday predicting Q3 deliveries of 470,000, which is only 1.9% above consensus estimates of 461,450. Both say that the buyside’s expectations are much higher, with UBS reporting its clients seeing Q3 deliveries between 465,000 and 480,000, the average of which (472,500) would only be 2.4% above consensus—hardly a reason for Tesla to rally as much as it has.

If this is a “Q2 delivery event” all over again, the downside is deep: Barclays noted that the buyside’s bullish outlook on Q3 deliveries is a change from its more bearish expectations in Q1 and Q2.

Note that in Q2, the buyside saw deliveries of only 410,000 to 425,000, the average of which (417,500) was 3.7% below Q2 consensus of 433,397. After Tesla reported Q2 deliveries of 443,956, the stock surged by 10% the following day despite only beating the Street by 2.4%. However, it did overshoot the buyside’s average estimate by 6.3%, which is likely why the stock spiked by 10% the next day. Hence the importance of the current buyside Q3 consensus of 472,500.

Tesla could drop heavily if its Q3 delivery report on October 2 is lower than the buyside’s average estimate of 472,500. My gut feeling is that Tesla will produce a Q3 delivery print that’s at least higher than the Street’s estimate of 461,450 in order to keep the stock rising into its October 10th “Robotaxi Day” event.

$260 seems to be the cap on upside 3 times in the past 12 months: The upside in Tesla’s stock price may be limited unless Q3 deliveries are closer to the buyside’s high-end estimates of 480,000 (which is somewhat hard to imagine).

Recall that Tesla only rose by 15% to $210 over its past 5 trading days ahead of the Q2 delivery report. It rose by 10% the following day to $231 and then hit a high of $263 five trading days later on July 10. Thereafter, Tesla dropped back to $215 after the horrible Q3 earnings report.

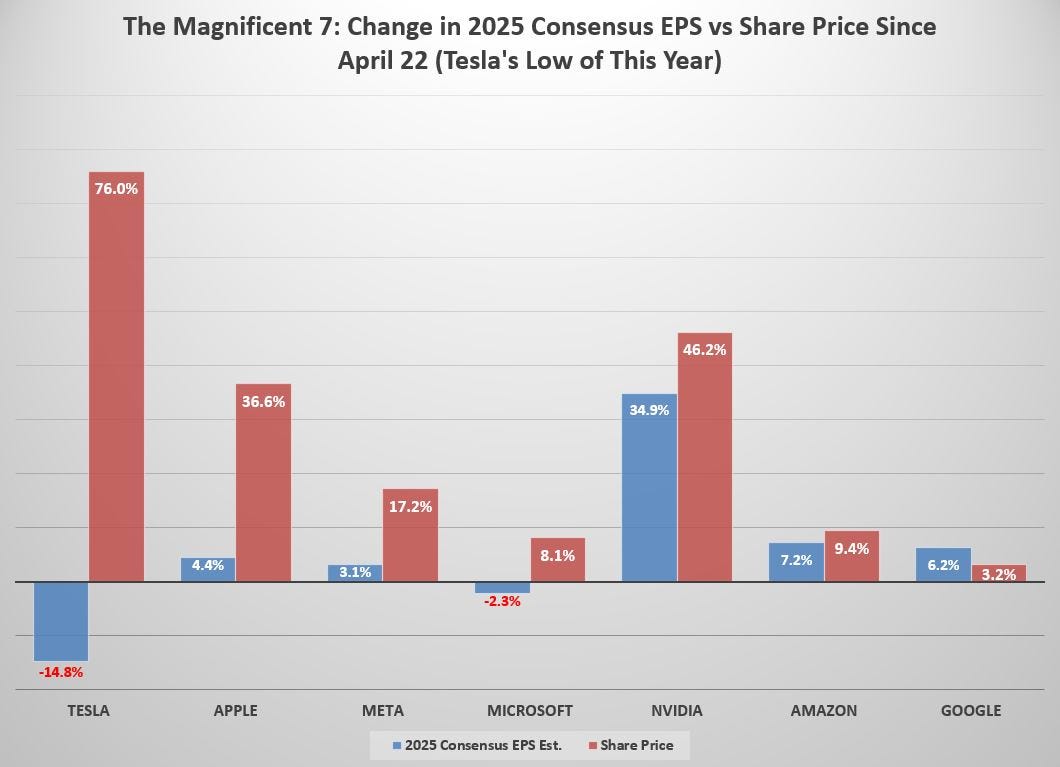

The $260 level seems to be the “line in the sand” for Tesla’s upside since October 10, 2023 (see Figure 1), despite the Nasdaq 100 being 31% higher since then. This is largely due to Tesla’s 2025 consensus earnings estimates being down by 41% year-to-date to $3.01. Since Tesla’s low of $142 for the year, Tesla is up 76% despite 2025 consensus EPS estimates dropping by 15% (see Figure 2).

Figure 1: Tesla’s Upside Seems Capped at $260

Source: Bloomberg

Figure 2: The Magnificent 7’s Change in 2025 EPS Outlook vs Change in Share Price Since Tesla’s April 22nd Low of the Year

Source: Bloomberg

Higher China Numbers Aren’t Positive Given Huge Discounts

China is up versus low hurdles in Q3 2023 but profits likely lower: The higher domestic insured sales in China this quarter are also causing the bulls to become more excited: overnight reports show that Tesla’s China local deliveries of 13,800 last week (+2.2% YoY; -11% vs last week), may be on course for Tesla to hit a record quarterly high for deliveries in China.

It should be noted that a year-over-year (YoY) increase in Tesla Q3 deliveries is completely factored in due to the low hurdle in Q3 2023: The Shanghai Model 3 line was shut down in Q3 2023 in order to retool for the October launch of the refreshed Model 3 “Highland” in October 2023. Unfortunately, Tesla saw weak orders for the new Model 3, which caused a 7% discount since then and served as proof that Tesla still can’t rejuvenate demand with its “refresh” efforts (Models S/X/3 all have seen big price cuts since their launches).

Tesla China sales in Q3 likely lead to lower profits YoY: Tesla’s Model 3 and Model Ys sold in China have the lowest prices in the world (at least 20% lower on average than US prices after taxes). The addition of 0% interest-rate loans for 5 years in Q3 this year in China likely leads to zero operating profits, despite higher operating rates this year versus Q3 2023. The massive bloodbath from the price war in China (spurred by Tesla’s deep cuts from Q1 2023) has yet to end.

Last Friday, the Mercedes-Benz Group (MBG) lowered its 2H 2024 operating profit guidance by 30%. This was not due to lower-than-expected volumes, but because of worse-than-expected pricing. They mentioned China as their key area of weakness. MBG also warned that free cash flow would be lower than expected. This warning is worse than BMW’s downward revision two weeks ago, half of which was attributed to a massive brake recall. Benz had no recall, yet guided much lower than BMW. Both generate over 2/3 of their sales in China.

While Tesla has a much stronger standing in China than Benz or BMW given all the subsidies there to buy EVs (and the disincentives to buying petrol cars), it’s hard to imagine Tesla being more profitable than it was in Q3 2023, amid this vicious price war in China.

Tesla Bulls Pumping the Stock Hard Since Last Week

Some prominent Tesla bulls are tweeting to the world that Q3 will be the bottom of Tesla’s earnings decline due to the “new” affordable Tesla model slated to come out in 1H 2025. Here are the main points that upend this prediction:

Tesla only announced a new, affordable model “by 1H 2025” after Reuters’ April 5th scoop on Tesla scrapping the much anticipated “Model 2” priced at $25,000. This led to a big drop in Tesla’s stock to which Musk responded by tweeting (in a rage over the Reuters scoop) that Tesla will have a “Robotaxi Day” on August 8, which was delayed to October 10 last month.

Despite only 21 words about future products in its Q4 2023 Shareholders Deck (released on January 4), the next Deck on April 23 had 142 words about new model launches in the same section due to the Reuters’ scoop of Tesla scrapping its Model 2 compact on April 5.

Bernstein rebuked by Musk on Q2 call for asking about 2025 new model details: Given the language about “new model” launches in its Q1 Shareholders Deck, it was natural for Bernstein’s Tony Sacconaghi to ask Musk if these “new models” would simply be “tweaked” versions of the current Models 3/Y, given they are said to be built on the same line in Tesla’s Q1 and Q2 2024 Shareholders Deck. Musk shut him down by saying, “Enough on this subject”. Musk also shut down Sacconaghi’s question about the Model 3’s slower-than-expected ramp on the May 3, 2018 earnings call, saying his question was “boneheaded”. Musk later apologized to Sacconaghi on the next earnings call.

Prominent Tesla bull says 2025 will be like 2020’s launch of the Model Y: “This is very similar to 2019-2020 when Einhorn, Chanos, and other TSLA shorts got their heads handed to them because they didn’t realize the Model Y would usher in a whole new TAM [total addressable market] by getting TSLA into CUVs [compact utility vehicles, or small SUVs]. I warned the $TSLAQ community repeatedly on Twitter they were not looking at this right (they argued Model Y was just a big Model 3), I am warning again that the $25K-$30K Tesla will destroy anyone short TSLA”.

The above claim is wrong in the following ways: (a) The Model Y was a great hit, but became the world’s best-selling car amid a chip shortage that kept rivals shut down; (b) The Model Y was a revolutionary car that outsold the Toyota Corolla in 2023, so it’s unlikely that the “tweaked” version slated to be on sale in 1H 2025 can outsell or be more profitable than the original Model Y, and (c) the refreshed Models S/X/3 all saw huge discounts right after launch and volumes are still falling.

Tesla Trading—The Stock Tends to Levitate Between Quarterly Earnings & Delivery Reports

I’ve traded Tesla since 2016 and the one thing I’ve learned is that being fully short after a quarterly earnings result if you’re bearish might leads to losses as Tesla usually bounces in between—especially since Q1 2023.

This is why I never get fully loaded on my shorts (even if the fundamentals are weak) until a day or so before quarterly earnings results.

Aside from the Q1 2024 earnings call on April 23 (which missed by 10% but led to a rally of 12% the next day due to Tesla having been oversold at a 30 RSI), Tesla has on average dropped by 10% on every quarterly result since Q1 2023. Figure 3 shows the key data with a yellow highlight on that rare time that Tesla’s stock rose on bad results (Q4 2022’s bad results were also bad, yet led to an 11% rally the next day due to being oversold).

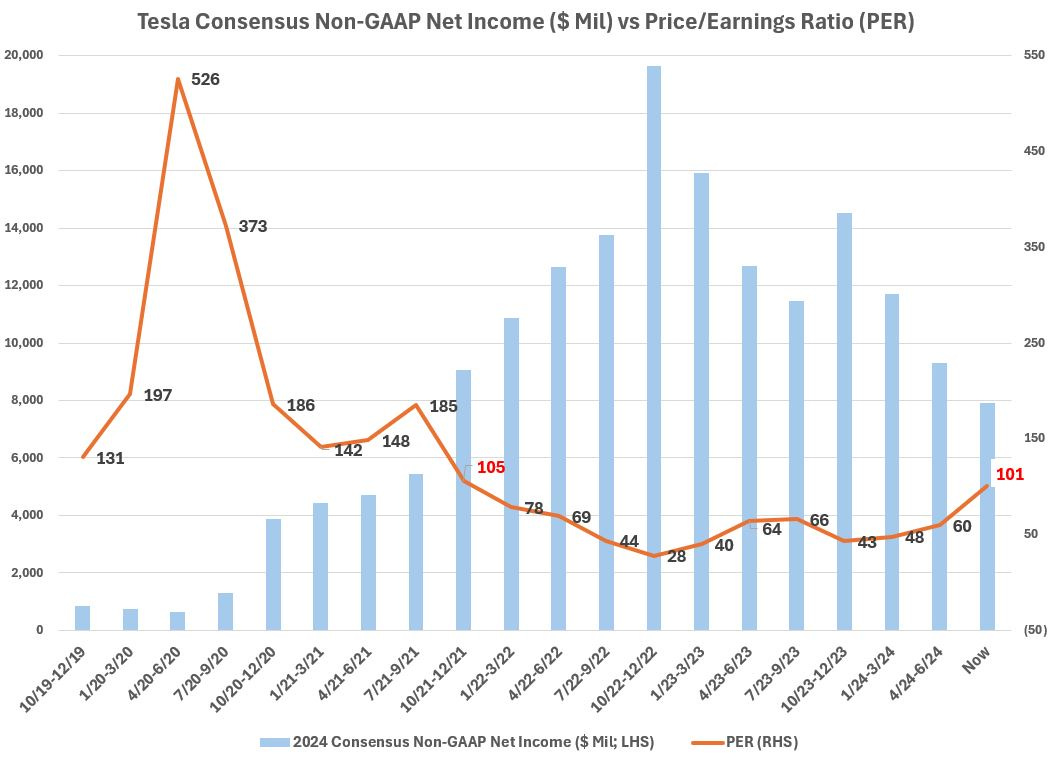

Figure 4 shows the current 2024 PER versus the decline in consensus non-GAAP net income estimates. The massive effort to hike TSLA 0.00%↑ to these levels is most likely quite dodgy and could one day come back to haunt Tesla. For now, however, it’s safer to assume that the stock is manipulated or highly influenced by big players in the options market, which is why it’s best to only be fully loaded with ones short position (or ease up with one’s long position) right before quarterly earnings results while Tesla continues to heavily discount its cars.

Figure 3: Tesla’s Quarterly Results vs Share Price Action

Source: Bloomberg

Figure 4: Tesla’s Current PER on 2024 Consensus Estimates

Source: Bloomberg

Note: Nothing in this report is investment advice.

Great analysis as always, Brad. Your objective views keep me from going crazy while I wait for this turkey to go down.

I did want to share 1 thought on Q3 deliveries, which I've been studying quite closely. We have solid Q3-to-date delivery data from several regions, namely the EU and China. Based on these, I'd give it a 50% likelihood Tesla meets or exceeds the Q3 delivery consensus estimate. It is far less likely they meet the Q3 buyside estimate of 472,500. That's going to take some major surprises or some major fraud.

Let me explain my thinking briefly. EU, China, and the US combine for nearly 90% of deliveries. EU deliveries are cratering (down nearly -20% y/y) while China is growing fast (could be up over 20% y/y). China is also the bigger market, but it's not big enough to offset the declines in the EU and meet these delivery estimates. They need more growth from somewhere to meet the consensus estimate. They need a lot more growth to meet the buyside estimate. Where would that growth come from? The US would be Tesla's best option by far, but I don't see how US deliveries could grow by the thousands they need to meet estimates after Elon has spent months doing everything he can to alienate his core market.

Tesla's China story looks good on the surface, but it won't save deliveries and the terrible margins will sink earnings. Hold strong, friends!

Brad, do you think, Tesla is really developing a $25 car? And if so, how the car should look like?

IMHO, $25k car is something like Corolla, ie Model 3, which cost maybe $35k to produce. Not sure, that building some 2 seats 3 wheels weirdo would open another "Model Y like" opportunity. Maybe rich Americans will buy such cars as 3rd car to the family, but for most, "Corolla like" is primary means of the transportation. On the other hand, they can do such a car in China already....