Tesla Q1 Progress Report: The Worst is Yet to Come

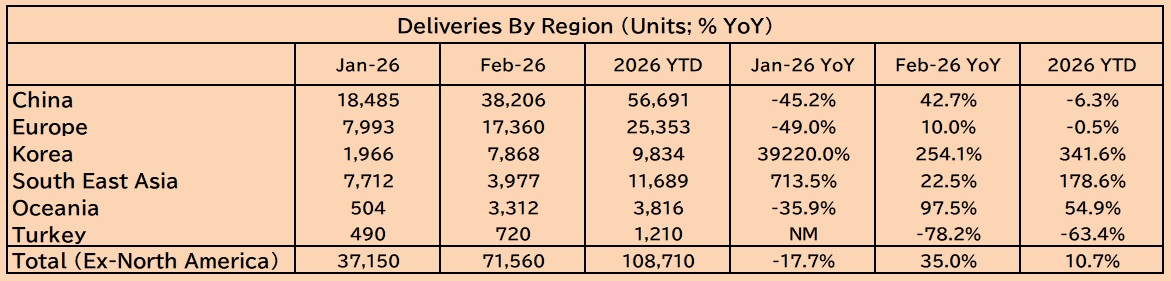

Deliveries outside of the US are up 11% YTD, but this is due to a low hurdle in Q1 2025 and huge discounts so far this year. Higher volumes don't lead to higher profits, as the trend has proven.

Tesla’s share price closed below its 200-day moving average on Friday for the first time since September, and the chart now looks really broken (see Figure 3).

There’s a palpable nervousness among Tesla fans about the Cybercab, which is scheduled to start production next month but still lacks a permit to be sold as designed, without a steering wheel or gas/brake pedals. Because this is the only new product Tesla has within its aging model lineup, tensions are high.

The only thing that had held Tesla’s stock above $400—a psychologically critical level, which was breached 4 times but pumped back up since last September—is the continuous high hopes for robotaxis.

The market is still largely duped by Musk’s lies about Tesla’s ability to launch a paid driverless ride-hailing service, as the mounting death toll and serious injuries have rendered Tesla’s “Full Self-Driving" software 4x less safe than humans (see details in last week’s report).

Deliveries outside of North America are up 11% YTD: Most countries except for North America have already reported Tesla’s registrations, and they’re up by 11% YTD, after a 35% YoY surge in February (see Figure 1).

Q1 2026 has a low hurdle due to weeks of downtime last year: Giga Shanghai, Tesla’s largest factory, saw over 3 weeks of production downtime from January to February 2025 due to retooling for the refreshed Model Y. This makes Tesla’s February sales growth of 43% YoY in China seem spectacular, but it’s actually +28% YoY on a daily-sales basis, with revenues of $1.8 billion down by 7.7% YTD in light of 8.5% price cuts. Tesla’s European operations are even worse, despite having longer downtime in Q1 2025, with deliveries flat YTD and prices down by 8% from Q4 2025 levels.

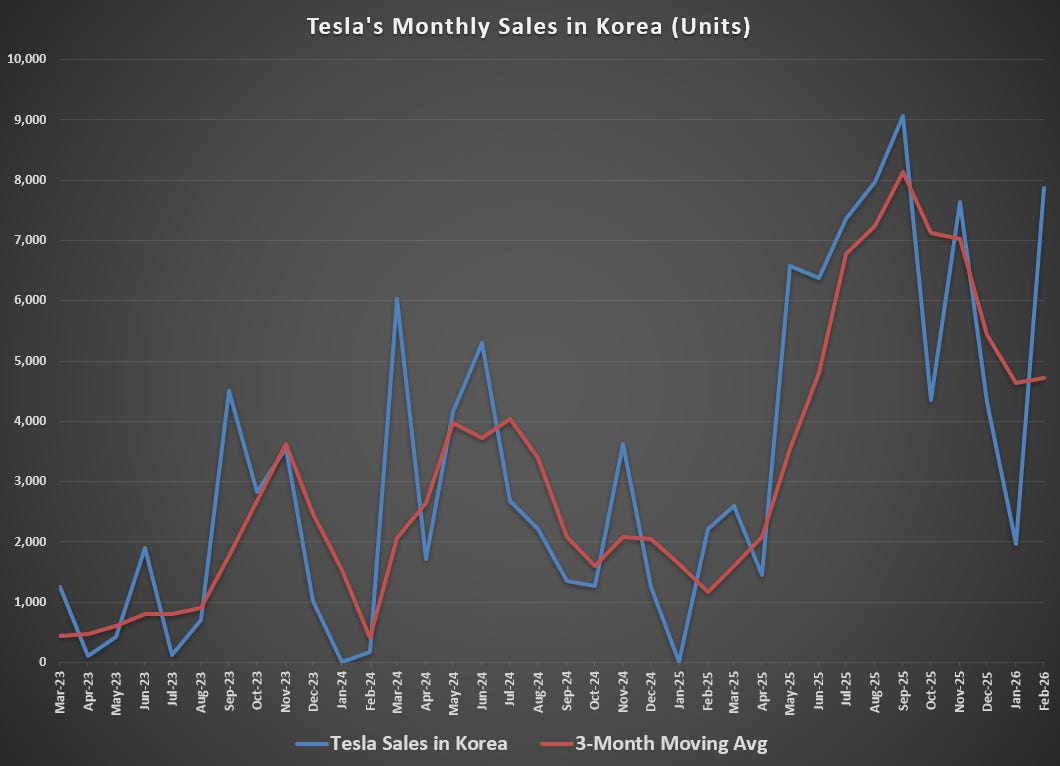

Korea is carrying Q1 2026 global deliveries: Tesla cut its Model 3 and Y prices by 16% on average, which, along with Korean EV subsidies, lowered the price of the cheapest Model Y to $25,354 versus $39,990 in the US. This has led to 9,834 deliveries YTD in Korea, or 16% of 2025’s total of 59,916 (see Figure 2). Tesla is selling these cars at cost or lower in order to keep its Shanghai factory from falling below 80% capacity utilization.

The stock chart is broken and valuations remain extremely high: After having struggled for 5 times since September to stay above $400, Tesla’s closing price of $391 on Friday was the first time since then that it closed below its 200-day moving average (see Figure 3). Moreover, the usual call buying doesn’t seem to be as effective as last year, as it only worked in concert with "robotaxi” catalysts (see Figure 4). This is also the first time in a while that the put/call ratio declines with the stock price, rather than moving in the opposite direction up to now (see Figure 5).

Tesla’s market cap is 28% higher than its top 15 rivals, combined: Tesla’s EV/sales ratio is 15.35x versus the sector average of 0.47x, while its P/E multiple is negative versus a sector average of 11.2x. Despite having one of the worst earnings outlooks in the sector, Tesla’s current market cap of $1.3 trillion is 28% higher than the $1.01 trillion market cap of its top 15 rivals, combined (see Figure 7).

Tesla’s 12-month price action is 2nd best among the Magnificent 7: Despite having the lowest profitability among its Mag-7 rivals and negative earnings growth, Tesla’s share price over the past 12 months is still up 63%, or second only to Google’s 83% (see Figure 8). While Tesla usually outperformed rising markets and underperformed falling markets through 2024, this trend was broken in 2025, and hasn’t recovered so far this year (see Figure 6). The coming SpaceX IPO looks to raise $50 billion (74% of total IPOs + SPACs in 2025), and this should cause forced selling for investors looking for the next “10 bagger” and those who can only be exposed to one “Elon Musk” stock. Given its sky-high valuations versus real tech companies in the Magnificent 7 (see Figure 9), Tesla could plunge ahead of the SpaceX IPO if there hasn’t been an official launch of its driverless robotaxis.

====================================================================

Figure 1: Low 2025 Hurdle Drives Sales Growth Outside of the US

Source: Local car registration agencies.

Korea is Tesla’s New “Dumping Ground”

Tesla’s huge growth in South Korea during January and February 2026—with nearly 10,000 units delivered, nearly quadruple the previous year’s volume—is a result of aggressive pricing to uphold healthy operating rates at Giga Shanghai, Tesla’s most profitable factory.

Tesla strategically lowered the price of the Model Y RWD to ₩49,990,000 ($34,349), precisely undercutting the government’s ₩53 million price cap to qualify for 100% of the newly announced 2026 EV subsidies ($4,300 on average). This move, combined with a new ₩1 million ($687) “cash for clunkers” deal for people trading in their ICE vehicles, allowed Tesla cars a deal many Koreans couldn’t refuse.

Figure 2: Tesla’s Monthly Deliveries in Korea May Be Peaking

Source: KAIDA.

China Sales Drop Despite Low Hurdles & Higher Incentives

Keep reading with a 7-day free trial

Subscribe to Motorhead to keep reading this post and get 7 days of free access to the full post archives.