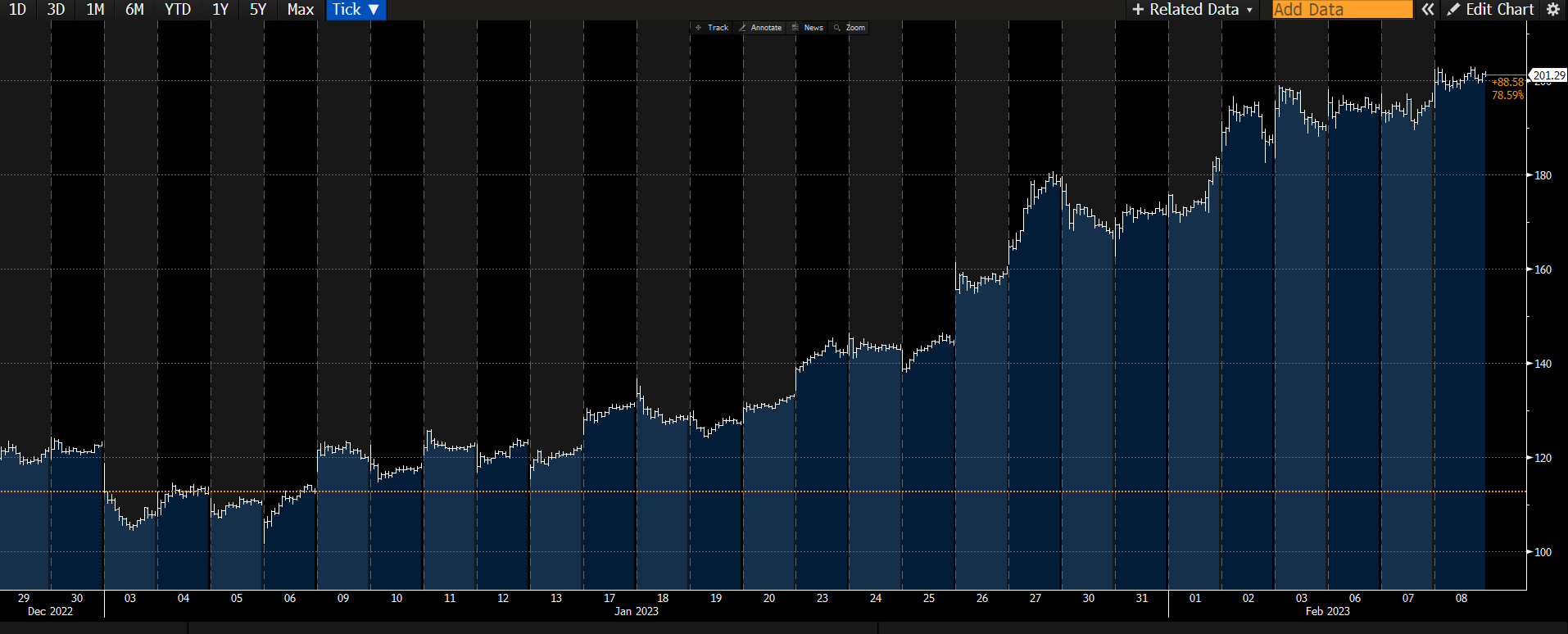

Only Tesla Would Rally on These Numbers

Tesla missed EPS estimates by 47%; Stock goes up 43%.

EPS Effectively Missed by 47%: Tesla reported a 6% Q4 2022 GAAP EPS beat, but stripping out a one-off deferred revenue recognition of $0.3bn & a $1.5bn reversal of deferred tax asset (DTA) valuation allowance, Q4 EPS missed by 47% (see Figure-3).

Gross Margins Missed by a Wide Margin: Tesla’s key metric of performance is the automotive gross margin (ex…

Keep reading with a 7-day free trial

Subscribe to Motorhead to keep reading this post and get 7 days of free access to the full post archives.