[NEWS]: Tesla's Tweet Implies Q1 Output Down 3% YoY

[NEWS]: Tesla's Tweet Implies Q1 Output Down 3% YoY

This confirms widely flagged estimates that Tesla is no longer growing. But it may be completely factored in. Trade carefully ahead of April 2 Production & Delivery Report.

Q1 2024 Output Appears to be Down 3.4% YoY

Tesla tweeted on March 29th that their cumulative production since inception hit 6 million vehicles (see above screenshot). This implies that Q1 2024 production at Tesla came to 425,776 vehicles, down 3.4% from 440,808 units a year ago in Q1 2023.

This confirms the consensus estimates that Tesla didn’t grow this quarter. While the Q1 deliveries are hard to extrapolate from this, I’m hearing it might be lower than production.

There are two ways to analyze Q1 2024 deliveries based on historical numbers:

Historically, since Tesla’s Model 3 went into full production in 2019, Tesla’s quarterly output has been 1.8% higher than deliveries. If this Q1’s deliveries are the same, it implies 417,839 deliveries globally in Q1.

Using the average Q1 production rate vs deliveries since 2019 shows that output in Q1 was 7.7% higher, so by this measure, this quarter’s deliveries could be 395,336.

Both are simply simulations based on historical trends, but it seems like around 400,000 is likely, and if it’s above, Tesla could see a relief rally.

In my 8 years of covering Tesla, I’ve never experienced a quarterly delivery report as highly anticipated. Nothing I’m writing here is investment advice, but I’ll be selling my puts on Monday ahead of the Tuesday Production & Delivery report from Tesla.

I have a gut feeling that Tesla will publish a beat of some low estimates of around 400,000, which could spark a short-term relief rally.

I’m confident that earnings will disappoint in Q1 and the rest of the year, so plan to be short ahead of Q1 earnings results in late April. But I don’t want to be short on April 2’s Q1 Production & Delivery report when weak numbers have been this well-flagged.

Musk is desperate to get Tesla’s share price higher, as evidenced by his huge effort to pump Tesla’s FSD story this week (details here), and my gut feeling is that he might be looking to finance after Tesla’s 10-Q is published.

Table 1: Auto Returns & Valuations Ranked by Pre-Tax Margins

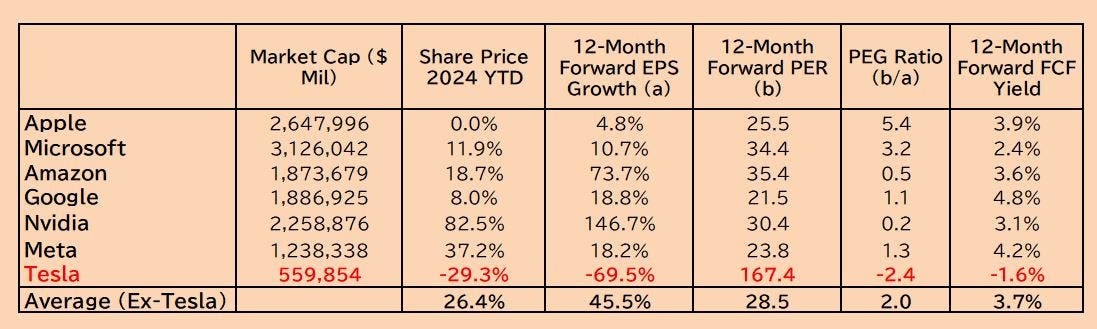

Table 2: Magnificent 7 Returns & Valuations

Nothing in this note is investment advice.

Consensus among Wall St analysts is a lot higher than Troy's estimate. Even 420k would be seen as a miss compared to Wall St.

Production at 425k is down 14% versus Q4. That will result in a 2 to 3% hit to margins as fixed costs are spread over a fewer cars. Discounts and price cuts have continued in Q1, maybe another 2% hit to margins.

Automotive gross margin likely around 12% before reg credits and leases.

60k fewer deliveries at 2% lower prices. Automotive revenue drops to $18 billion ex reg credits and leases (Wall St. estimates for revenue are about $3 billion too high).

Automotive gross profit falls to 2.2 billion plus reg credits, leases and energy, $3 billion

Operating expense $2.4 billion, Net profit $0.6 billion, 19 cents/share.

Fewer parts ordered, payables down, free cash flow negative.

Huge miss, share price collapses.

Not investment advice.

Interesting. I think the opposite. Consensus is 455, which is stale, but recent updates center around 425, and only today Gary suggested 415. Troy is an outlier, so anything below 425 is a miss imho. A bearish analyst ($85pt) suggested 430k on CNBC (yesterday I believe).

Elon has been pumping FSD bc sales are a miss, which has kept the stock propped up (when china data came in weak).

I’m more concerned that earnings are weak, but Tesla recognizes FSD deferred revenue (and/or other levers) and numbers appear better than expected, stock rallies, while no one waits to read the 10Q.