Lucid Motors Q4 Impressions: $5 Billion in Financing is Unavoidable this Year

Lucid Motors Q4 Impressions: $5 Billion in Financing is Unavoidable this Year

Order Cancellations were twice Full-Year Deliveries

To give you an idea of how grim the situation at Lucid Motors is, imagine selling cars for $133,392 but paying $318,478 to produce each one. That’s what Lucid’s Q4 looked like. And it gets worse.

The CEO said that Lucid is no longer production-constrained, so the real problem is demand, which he says is not high enough due to Lucid not having enough brand recognition (imagine the advertising expenses needed to solve this on top of the $1 billion per quarter of cash burn).

“My focus is on sales. And here’s the thing: We’ve got what I believe to be the very best product in the world and just too few people aware of not just the car but the company.”

Peter Rawlinson, Lucid’s CEO on the 2/22/23 earnings call

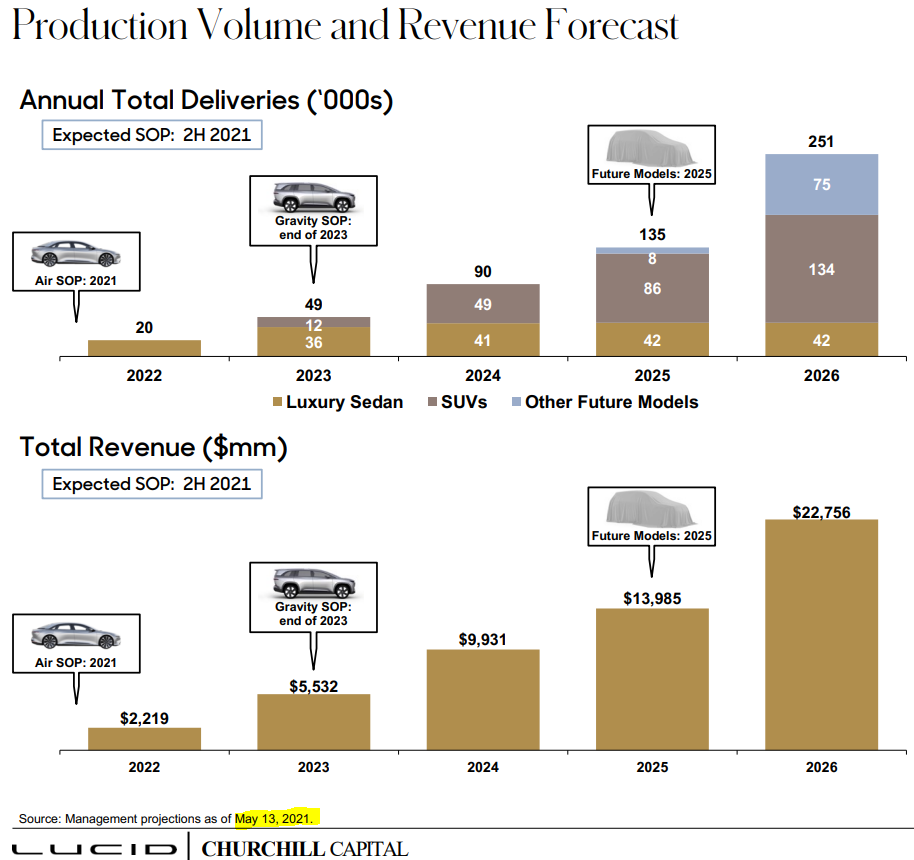

Hence the limp-wristed 2023 production target of 10,000 to 14,000, which at midpoint, is 47% below consensus estimates of 22,700. It is also 76% below Lucid’s original July 2021 target of 49,000 units of output in 2023 when they were marketing to get listed (see Figure-1).

It is also probably why the carmaker was forced to offer $7,500 incentives in an attempt to clear inventory, which skyrocketed to 2,936 vehicles, which is an astoundingly high level relative to 2022 full-year deliveries of 4,396 deliveries (first time I’ve ever seen anything like this).

Below are the other significant negative points mentioned on Lucid’s earnings call last night.

Figure-1: Lucid’s 2023 Production Forecasts are 76% Below what they Saw in July 2021, Pre-Listing

Reservations Drop by More than 2022 Full-Year Deliveries: Reservations fell by 6,000 units (18%) QoQ and are off by 9,000 units (27%) from their Q2 high of 37,000 models. The 9,000-unit shortfall in orders from their peak in Q2 2022 are more than twice what Lucid delivered in 2022.

Lucid’s CEO explained that this was because orders are being canceled due to long waits from production issues and parts suppliers not ramping up quickly enough to supply those models which are in high demand. There are no other carmakers blaming suppliers of anything but auto semiconductors being in short supply at the moment.

Deferring capex to Next Year Again: Lucid cut their 2022 capex plan from $2 billion to $1.2 billion after bad Q3 results and the need for cash. They said that the $800 million of deferred capex would be used in 2023, which meant that they should’ve had a capex budget of around $3 billion this year.

In a sign that Lucid is cash-constrained, their 2023 capex guidance only came to $1.6 billion (the midpoint of a guidance range of $1.5 billion to $1.75 billion), which is concerning given the fact that Lucid’s 2023 production plans of 12,000 units is 76% below original plans of 49,000 before they listed in July 2021. More than anything, it is another clear sign that demand for Lucid’s cars is not robust at the moment.

Q1 and Q3 2023 Warning: Lucid’s CFO said that, due to a “planned shutdown of the factory in order to conduct a year-end physical inventory count” (never heard of anything like this before), Lucid saw 7 days of downtime in January, so Q1 earnings will be bad.

The CFO also warned about how exports to Europe and the Middle East this year would increase “in-transit” times on ships and that depreciation of new equipment to be used from Q3 would also weigh on earnings. But Q4 should be great, is the message. Nice runway for the year.

All in all, Lucid is warning that this year will be very tough. This might be due to having revised down estimates so many times last year, which could be a positive if Lucid can overshoot the lowered bar in guidance this year. But it does show what extreme strains the carmaker is under.

“Other” Income Reduces 2022 Net Losses by 40% in 2022: Because of outstanding warrants from Lucid’s SPAC merger in July 2021, the lower the stock price, the higher the warrant valuation gains Lucid books are (and vice versa). These are non-cash valuations gains, but the 2022 warrant valuation gains were $1.3 billion, which reduced net losses from -$2.6 billion to -$1.3 billion.

Conclusion: Lucid will Need another Equity Raise by Q3

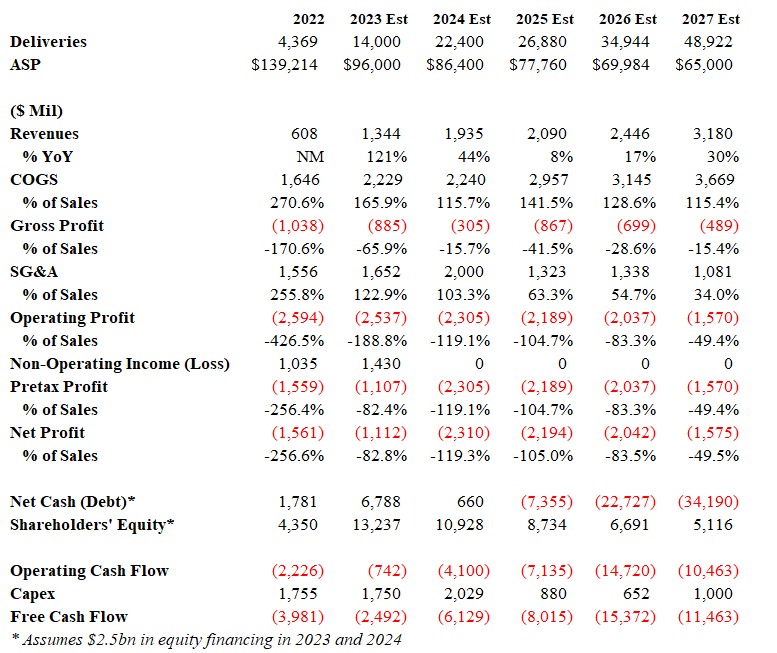

Given the 2022 results & 2023 guidance, it looks like Lucid should see $2.5 billion in operating losses this year, which would be flat with 2022 levels, despite 3.2x higher deliveries (see Figure-4).

This is based on the assumption that COGS/unit will only halve in 2023 (due to higher battery cell costs) despite the four-fold rise in deliveries to 14,000. It also assumes that ASPs will fall by 31% YoY from $139,214 to $96,000 due to the majority of Lucid’s order backlogs are for the Lucid Air Pure model, which is the lowest-priced trim at $84,700.

The company gave very little detail about why production in 2022 was 7,180 versus deliveries of only 4,369 vehicles. There were comments about orders being “in transit”, logistics, etc. regarding the huge inventories. If this were the main cause, Lucid would not have been forced to offer $7,500 incentives for its cars this month.

Lucid launched an equity raise of $1.5 billion on November 8th last year, after Q3 cash & equivalents fell to $3.3 billion (net cash was $0.9 billion). Lucid’s cash burn in Q4 2022 was roughly $1 billion and Q4 cash & equivalents were at $3.9 billion, in spite of the equity raise. If Q1 is as bad as the CFO warned, it would not be surprising to see Lucid do another equity raise in Q2 or Q3 of this year.

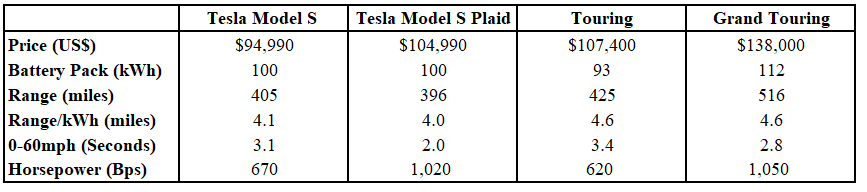

Tesla’s price cuts on the Model S are a sign of how much pressure Lucid is under (Figure-2). And the fact that Lucid can’t meet their order backlog on their cheapest variant (the Lucid Air Pure), is a sign of bad management. Not to mention the fact that 70% of US car buyers prefer SUV over Lucid’s sedan line-up.

Figure-2: Model S Prices Now are on Average 15% Lower than Lucid

Warning about Being Short Lucid Motors—Saudi Arabia Owns 61%

The Saudi Arabia sovereign wealth fund (PIF) has a 61% stake in Lucid Motors, which means Lucid’s free float is only 33.7% of shares outstanding. The current short interest, according to Nasdaq data as of January 31st, is 145 million shares, or 2.8x average 30-day volumes, which is not that much.

But it can get squeezy. A rumor from the UK stock website, Betaville, on January 27th said that PIF was preparing to buy out the rest of minority shareholders, which sent Lucid’s stock price soaring by over 40% intraday.

So Lucid is squeezy, but you have to ask yourself this: why would PIF buy Lucid at these valuations if money didn’t matter? Why not wait for Lucid to approach the brink of bankruptcy?

Moreover, why has PIF invested in another EV start-up called “CEER”, which is licensing technology from BMW and using Apple’s assembler, Foxconn, to make their cars in Saudi Arabia? Saudi Arabia is hedging their bets.

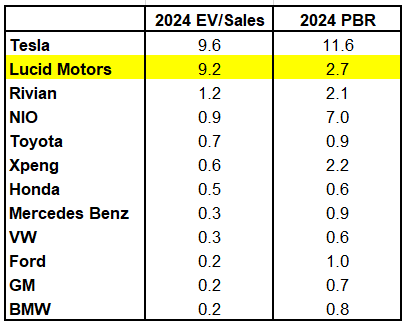

Figure-3: Valuations—Lucid has the Second Highest Valuations in the Auto Industry

Figure-4: Lucid Earnings Estimates

Great write up Motorhead! I suspect dilution is gonna happen soon (in Q1). Equity mkt is not getting better as the year goes by and everyone knows market valuations are back to being frothy. If BBBY was able to raise money, I am sure apes will queue up for LCID

I think Peter Rawlinson is a very questionable/unscrupulous man. He said 7K deliveries in 2021, 20K in 2022. He keeps revising those numbers over and over. They have a very poor product market fit , it is not just about brand awareness. They kept releasing reservation numbers when it pumped the stock. In Q4 earnings report, they confirmed they won't be releasing the reservation numbers anymore since it is affecting them negatively. Talk about cherry picking , this is such a sleazy tactic

Btw, in 2022, PIF had promised to buy 100K vehicles from Lucid. If that was factually true and not just a pump, we wouldn't be having a "demand problem" . Coz they could produce all those cars and pretty much sell the ones which cannot be sold in US to Saudi Arabia. What do you think about that?

https://www.cnbc.com/2022/04/26/lucid-to-deliver-up-to-100000-evs-to-saudi-arabia-government.html