Diary of a Tesla Short Seller: Load Up Ahead of Q1 Results

Diary of a Tesla Short Seller: Load Up Ahead of Q1 Results

Low RSI fooled me into not pressing harder on my Tesla short; TSLA -12% this week versus flat Nasdaq

Tesla’s Been a Tough Short Amid Rising Tides

As a Tesla short seller, it’s been a glorious start of the year with Tesla’s stock down 28% versus the Nasdaq 100 index rising 9%.

Nevertheless, Tesla’s been a tough short if you started since its horrific Q4 2023 earnings call on January 24th, after which it dropped by 12% the following day and has been range-bound between $180 and $200 ever since. Things that trade in tight ranges are bad for hedge funds.

However, in a rising market with great rivals like Toyota Motor (+35% YTD; see Figure 1) as a long, Tesla has been a stupendously great short. And there’s likely more downside by the time we get to Q1 2024 earnings on April 19th.

Figure 1: Toyota Motor Outperforms Tesla by 63% in 10 Weeks

Source: Bloomberg

Morgan Stanley Slashes Estimates

This week, Morgan Stanley’s auto analyst, Adam Jonas, slashed his 2024 non-GAAP EPS estimates by 26% to $1.51 from $2.04 (consensus estimates for 2024 are still at $3.05).

He raised Tesla from Neutral to Outperform last September with a $400 price target, ever since which, Tesla has plunged by 29% to $179, so he was wrong.

But Wall Street’s biggest Tesla cheerleader only cut his price target by 7% to $320 on Monday and maintained his “Outperform” rating, saying that the non-automotive business (computing efforts labeled as “AI” and Tesla’s sloppy "Full Self-Driving” ADAS product) is worth 79% of his price target.

To be clear: there is no data on Tesla’s “AI” capabilities or its robotic operations in its financial statements. In 2023, 94% of Tesla’s gross profit was derived from its auto business.

Morgan Stanley extended the largest amount of margin loans to Tesla CEO Elon Musk for his $13 billion worth of convertible debt needed to purchase Twitter.

Musk reportedly had talks with the Twitter debt syndicate last week. I wouldn’t be surprised if Musk sells more Tesla shares to fund the $350 million/quarter of interest payments needed to pay for Twitter’s debt.

Back to Tesla’s fundamentals. Figure 2 shows how a Tesla bull who met Tesla IR on Monday tweeted that Tesla (a carmaker trading at 94x EPS), might be having tough times right now.

Figure 2: Tweet From Investor Who Met Tesla IR This Week

Source: Twitter (X)

In 8 years of covering Tesla, I’ve only seen Tesla pump their stock and never once seen them warn investors about anything.

But, the fundamentals in the global auto industry are deteriorating as the auto chip shortage—which allowed carmakers to hike prices—is almost gone:

US inventories have ballooned to 80 days supply vs 59 last year (60 is ideal). See details here. EV inventories are over 100 days’ supply.

Incentives are rising significantly because of higher inventory.

Zero-interest loans are rampant—a big sign of weak auto demand.

Bad Monthly Data Confirm Tesla IR’s Weak Guidance

Tesla has been guiding investors’ sentiment lower both for Q1 2024 and the full year. The weak monthly data for January and February in Q1 2024 underline this.

Because China’s lunar new year falls either in January or February, it’s always best to analyze car sales in China on a January + February combined basis.

Here’s what we have this week from all countries that report, except for the US, where Tesla isn’t required to report monthly sales data.

China: Bad Despite Price Cuts & New Model 3

January + February local sales are up 14% YoY, but wholesale shipments (local + export sales) were down 6% YoY despite deeper price cuts. Exports were down 22% in the January + February period (-20% YoY in January and -25% YoY in February).

This shows that EV subsidy cuts in France, Germany & Italy are hurting Tesla exports from China.

Today, Chinese EV makers like BYD and others launched another round of price cuts. Tesla’s gross margins on local China sales are close to zero.

The only reason its Shanghai factory made 70% of global profits last year is due to exports to the EU (see a detailed report on Tesla’s China profitability here). A 22% decline in exports from China quarter-to-date (QTD) is a massive hit to Tesla’s profits. In 2023, Tesla shipped over 200,000 vehicles to the EU. There are no other export regions that can take up that slack in Asia.

And while domestic deliveries are up 14% YoY, they’re down 26% QoQ in the first two months of 2024 versus Q4 2023.

Europe: Down 6% vs Q4 2023 + Factory Down for 1 Month

Despite the refreshed Model 3 being pushed on European car buyers, Tesla’s EU sales are tepid at -15% QTD versus Q4 2023. While this is up 14% YoY, it’s with much lower prices and a “refreshed” Model 3 (i.e. higher costs, as all new models require new equipment).

The European auto market is the weakest in the world after China and just as unprofitable from a local production standpoint (Tesla’s Shanghai factory made 70% of global profits in 2023 by supplying 59% of EU sales from China).

With the Red Sea dangers and a recent “sabotaging” of the German plant’s power lines, Tesla will see one month of downtime in Germany, where they have a stated capacity of 375,000 units per year (capacity utilization was only 51% in Q4 2023). Local officials have said that this will cost Tesla $1 billion in lost production, which sounds like a bit of an exaggeration.

Given that Tesla Shanghai lost around $200 million from closing down due to covid in 2022, Grunheide may cost around $300 million from one month of idled production. I’ll publish my Q1 2024 estimates next week.

US: EV Sales QTD Reportedly Flat YoY (February: -3% YoY)

The US is the only major car market in the world to not force Tesla to disclose its sales data (50% of 2023 revenues).

But according to automotive data trackers in the US, February EV sales were down 3% YoY (January was +5% for the segment). This implies much weaker growth for Tesla than the industry, which is up 10%+ in 2024 YTD.

Furthermore, there’ve been some tweets this week about Tesla’s Model 3 line in Fremont, CA having problems with the refreshed Model 3.

The problem seems to be the white interior of the Model 3. It would not be surprising if the German and US plant slowdowns were a method of reducing high inventory levels in both regions.

Rest of the World: Down Over 30% vs Q4 2023’s First 2 Months

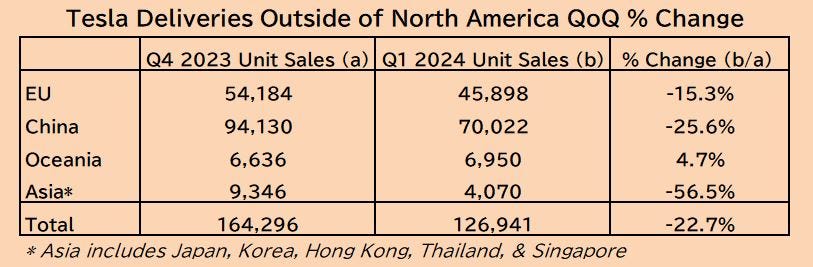

Asia has seen a huge pullback in the first two months of 2024 versus the first two months of Q4 2023, which makes sense given the year-end push.

Australia seems to have become the dumping ground for Tesla’s Shanghai excess capacity, with sales up 14% QoQ. This seems to coincide with new tax laws that make EVs cheaper as company cars.

Oceania, as a whole, was only up 5% QoQ due to New Zealand deliveries dropping by 75% QoQ in the first two months of this quarter.

Figure 3: First Two Months of Sales in Q1 Are Down vs Q4

EU Solidifies Roadmap to Taxing China-Made Imports

From this July, the EU will start “experimentally” taxing EV imports from China. By November, it’ll be solidified. Tesla is the biggest exporter of EVs to the EU from China and they should face considerable tariffs. This has yet to be factored into Tesla’s share price, but it can’t be ignored: Around 204,000 vehicles, or 59% of Tesla’s 2023 EU sales, were supplied from its Shanghai factory.

I’ve written about how important Tesla’s Shanghai factory is from a profit perspective (short report here). The decline in 2024 exports from Shanghai should have a significant impact on earnings.

Final Word: Outlook is More Negative

The question is how much to lean in here on the short side. These are my thoughts:

RSI at 35 is still close to the trough of 30.

Monthly data got the share price this low, but there’s nothing as such until Tesla announces Q1 2024 deliveries on the 1st or 2nd of April.

The delivery numbers should disappoint, but who knows (Tesla is notorious for pumping sales in the last month of the quarter).

The Q1 2024 earnings should disappoint even more (on top of weak deliveries, the German plant will have been down for one month in Q1).

2024 consensus EPS estimates of $3.05 are way too high. My estimate is $1.73.

As of now, I’m seeing Q1 2024 non-GAAP EPS at $0.47 versus consensus of $0.65. If I’m right, the stock should plummet. Or it could slowly drop into Q1’s earnings call on April 19th in expectation of that. Either way, I do plan to be short in size ahead of Q1 results unless the situation improves.

I will publish my earnings estimates next week. For 2025 and 2026, they’re negative.

Valuations and Returns

At a 2024 PER of 94x and an EV/EBITDA multiple of 80x, Tesla trades at a 1,477% and 2,466% premium to the industry average, respectively (see Figure 4).

Even compared to the “Magnificent 7”, Tesla is an outlier. I’m confident that, after horrible Q1 results, Tesla will be kicked out of the Mag-7. Current valuations versus the Mag-6 are in Figure 5.

Figure 4: Tesla Valuations & Returns vs Industry Rivals

Figure 5: Tesla Valuations & Returns vs The Magnificent 6

Please note: None of the above is investment advice.

Great write-up.

TSLA has been a fantastic hedge to this bull market. If you're an investor, wtf are you still doing in this stock and missing out on the rest of the market lighting it up. Thanks for the liquidity though.

You're going to see traders front-run Q1 results like they front-ran Q4 earnings. This move being so telegraphed is a bit concerning and will affect price action.

RSI is a horrible timing tool.

Great insights waiting for your next post