Tesla's Q2 Earnings Could be a Rug Pull on the Current Rally in Its Shares

Tesla's Q2 Earnings Could be a Rug Pull on the Current Rally in Its Shares

After a 44% rise in 4 weeks on no specific positive catalyst, Q2 earnings on July 23rd present a possible "rug pull" if Tesla misses by 20% to 30%, which seems likely

Tesla’s Market Cap Surged By 75% of Toyota’s Value in Just 4 Weeks

Tesla’s stock was stuck in a trading range between $180 and $190 for nearly two months between May 1st and June 25th, when it closed at $187. It broke out from that range on June 26th and has surged by 34% to $254 without one down day during the last 8 trading sessions.

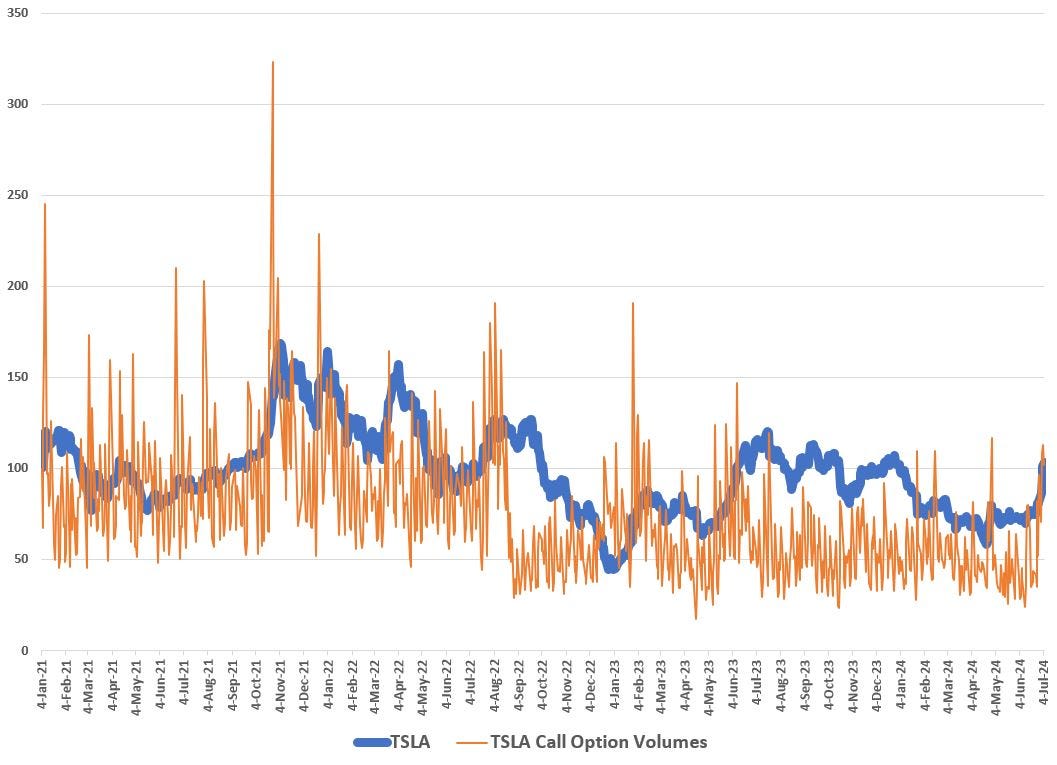

Tesla’s Q2 delivery report on July 2nd was only 2.4% above consensus estimates (which had come down by 8% in the previous 2.5 months), but this somehow added more fuel to the fire: The trading volume in Tesla call options—which helps move the stock upwards if volumes are strong—spiked by 223% on July 3rd versus pre-rally levels on June 25th (see Figure 2 below).

Tesla is up by 44% over the past 4 weeks. If it were a penny stock, it would not be significant. But Tesla’s market cap during this short period increased by $244 billion—the equivalent of 75% of Toyota Motor’s market cap. A rapid rise of this magnitude might be fine for Nvidia which is growing rapidly on the AI theme, but hardly apt for a shrinking carmaker valued at over 100x earnings.

Analysis of Why Tesla Surged by 44% in 4 Weeks

There is no convincing reason why Tesla suddenly rose so much on such high trading volume with virtually no positive news. It was down 43% year-to-date (YTD) at its low of $142 on April 22nd but is 77% higher over the past 10 weeks and is now up 1.2% YTD (although it still has underperformed the S&P 500 by 16% YTD).

The reasons I’ve heard about why Tesla ripped upwards so powerfully in such a short amount of time are largely unconvincing:

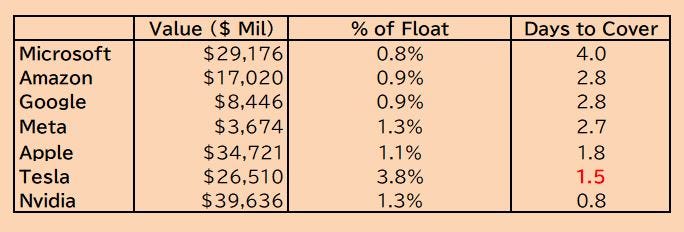

Short Squeeze: Tesla bulls—a rare bunch who enjoy huge gains in Tesla’s stock only if the bears become impoverished—point to a short squeeze in Tesla’s stock. But this is false as Tesla is one of the least shorted mega-cap stocks in the world (see Figure 1 below). In terms of the number of days to cover all the shorts in Tesla (“Days to Cover”, or the number of shares short ÷ 30-day average daily trading volume), there is no sign of a short squeeze as Tesla, at 1.5 days to cover, is the 2nd least shorted stock after Nvidia among the Magnificent 7.

Figure 1: Short Interest in the Magnificent 7

Hiring Uber’s Co-Founder for Robotaxis: There was a rumor—propagated mostly by Tesla bulls—that Elon Musk began following Travis Kalanick (co-founder and former CEO of Uber) on Twitter because he hired him to guide Tesla’s “balls-to-the-wall” move towards autonomy. Musk denied this yesterday.

Robotaxi Day on 8/8: Some Tesla bears speculated that the stock’s rise was anticipating Tesla’s “Robotaxi Day” on August 8th, which I disagree with, as Tesla events are known to cause huge sell-offs the following day and we have Q2 earnings results before that on July 23rd (which, as I explain below, should disappoint).

FSD Being Close to Release: One rabid Tesla bull on a Twitter Space yesterday explained that Tesla’s rip upwards was due to the market discounting the “short” time remaining before Tesla rolls out its robotaxis. This is obviously the least convincing explanation as Tesla’s Full Self-Driving (FSD) technology is so far away from full autonomy that Tesla has yet to even register it for qualification.

Energy Storage More Than Doubled in Q2: This is the most convincing argument, but still not substantial enough to move Tesla’s Q2 earnings (as discussed below). In its Q2 delivery report, Tesla mentioned that it deployed 9.4 GWh of energy storage products. This is a 132% rise versus Q1’s results and could lead to over $500 million in upside to Q2 profits if Tesla’s Energy Division maintains its Q1 gross margin of 25%.

The truth is that there is no good reason for why Tesla spiked by 44% over the past 4 weeks from a fundamental standpoint. The only thing that explains this move is the massive increase in trading of Tesla call options last week.

Tesla’s call option trading volumes last week hit highs not seen since April 29th when Tesla rose 15% in one day on rumors that Musk got a green light from China’s premier for rolling out FSD in China. This was since refuted by the Chinese media (here) which clarified Tesla was only given approval to test FSD in China.

Figure 2: Tesla’s Share Price vs Call Option Trading Volumes

The only thing that could keep this rally going is an earnings beat when Tesla announces Q2 results on July 23rd. But having gone through the numbers, Q2 results should disappoint, especially as consensus estimates are rising now (up 3% in the past week from $0.57 in non-GAAP EPS to $0.58). This is why I see Q2 results as a possible “rug pull” for Tesla if the results are as weak as I’m forecasting.

Q2 Could Miss By 30%

Given the lack of rhyme or reason behind Tesla’s meteoric rise in just 4 weeks, I took a close look at my earnings model and Q2 earnings don’t look good despite the huge deployment of energy storage products (“Megapacks” which are energy storage units that Tesla assembles with battery cells from suppliers like CATL & BYD).

These are the 5 major assumptions behind my Q2 earnings estimates:

Prices Fall by 2% QoQ: While it’s become more difficult to forecast Tesla’s ASPs (average selling prices) given flat levels in Q1 despite big price drops, I see Q2 being down by at least 2% based on announced price cuts and low-interest-rate loans in the US, China and parts of the EU. A decline of 2% QoQ for Tesla’s ASPs is a generous assumption as there were many new-car inventory deals with 10% discounts during Q2.

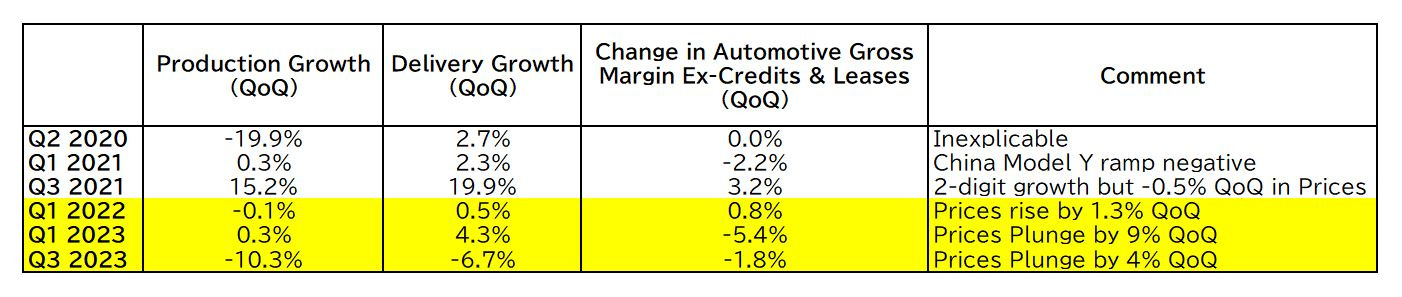

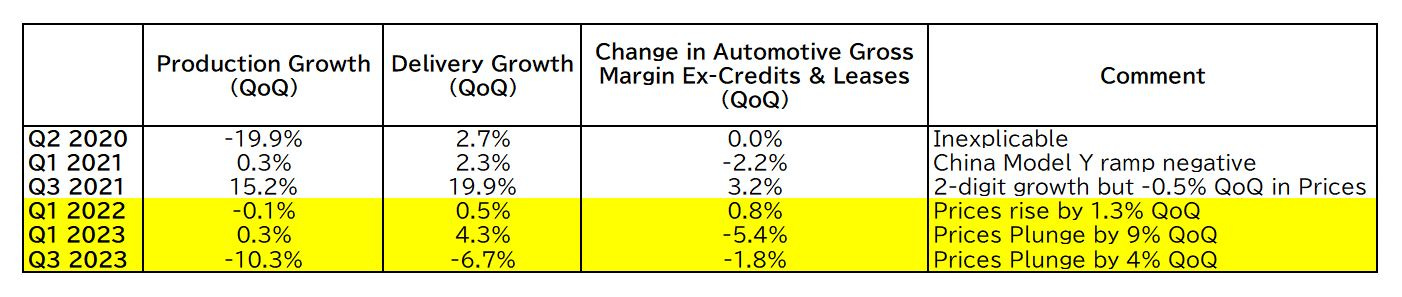

Costs/Unit Fall by 0.5% QoQ: This is the trickiest part of forecasting Q2 profits as deliveries increased by 15% QoQ vs Q1, but production dropped by 5% QoQ to a record-low capacity utilization of 68%, which is bad for fixed-cost absorption. Figure 3 shows all quarters since Q1 2020 where Tesla saw QoQ deliveries grow more than output and the impact on Automotive gross margins QoQ (in terms of %-point change vs the previous quarter).

The yellow-highlighted quarters are those that saw gross margin deterioration QoQ due to price cuts—which is the case in Q2 as well. Q3 2023 possibly serves as the best benchmark: re-tooling in Shanghai to prepare for the “refreshed” Model 3 Highland caused the Model 3 line there to close down for 3 months.

This led to Tesla selling inventory rather than producing cars for sale (very much like Q2, when Tesla needed to lower output to clear record-high inventories of 144,000 vehicles at Q1 end). My Automotive gross profit estimate (ex-credits, leases & deferred FSD revenues) for Q2 comes in 1.7% lower than Q1 despite deliveries having grown by 15% QoQ. This assumes a real COGS/unit decline of 2% QoQ (no specific reason; just lowering it in line with estimated price declines) and a gross loss/unit of $25,000 for the Cybertruck (TroyTeslike estimates that Q2 Cybertruck deliveries were around 11,000 units).

This too is generous, as Rivian saw gross losses/unit of $85,615 on average between Q4 2022 and Q2 2023 as it ramped up to 12,640 deliveries (mainly its pick-up truck model). One could argue that Tesla’s Cybertruck loses more money at its current run rate given its use of stainless steel and more labor costs per unit because of this (not to mention 5 recalls during the 6 months since it was launched).

Figure 3: Tesla’s Auto Gross Margins When Output Exceeds Deliveries

Deferred FSD Revenues Drop by 29% QoQ: Tesla stated in its Q4 2023 financials that it plans to recognize $926 million of deferred FSD revenues this year, after having recognized a whopping $281 in Q1. Over the past 3 years, Tesla has recognized roughly 73% of what it says it will book in deferred FSD revenues at the start of the year. I forecast $200 million of deferred FSD revenues recognized for Q2 (-29% vs Q1) and then $173 million thereafter for Q3 and Q4 as this adds up to $800 million (95% of what Tesla says it will recognize this year).

Energy Division’s Gross Profit Rises by $545 Million QoQ: While Tesla reported a Q2 deployment of 9.4 GWh of storage units in its Energy division (which made up 11% of total Q1 gross profits), revenue growth in this division has not been as high or low as the increase/decrease in GWh deployment. To be generous, I assume that GWh deployment of 132% QoQ is the same for revenue growth and use the same 25% gross margin seen during Q1. This gives an upside of $545 million in gross profits, which is duly generous.

One-Time $400 Million Restructuring Charge: In its Q1 10-Q, Tesla stated that it sees “in excess of $350 million” in Q2 restructuring charges, so I’ll assume $400 million, although this could be higher given the news that Tesla fired more than its originally planned 10% reduction in headcount. It should be noted that Tesla’s digital assets (mainly Bitcoin) were valued at $821 million as of March 31st, so Q2 restructuring charges could’ve been offset if Tesla sold some of its Bitcoin.

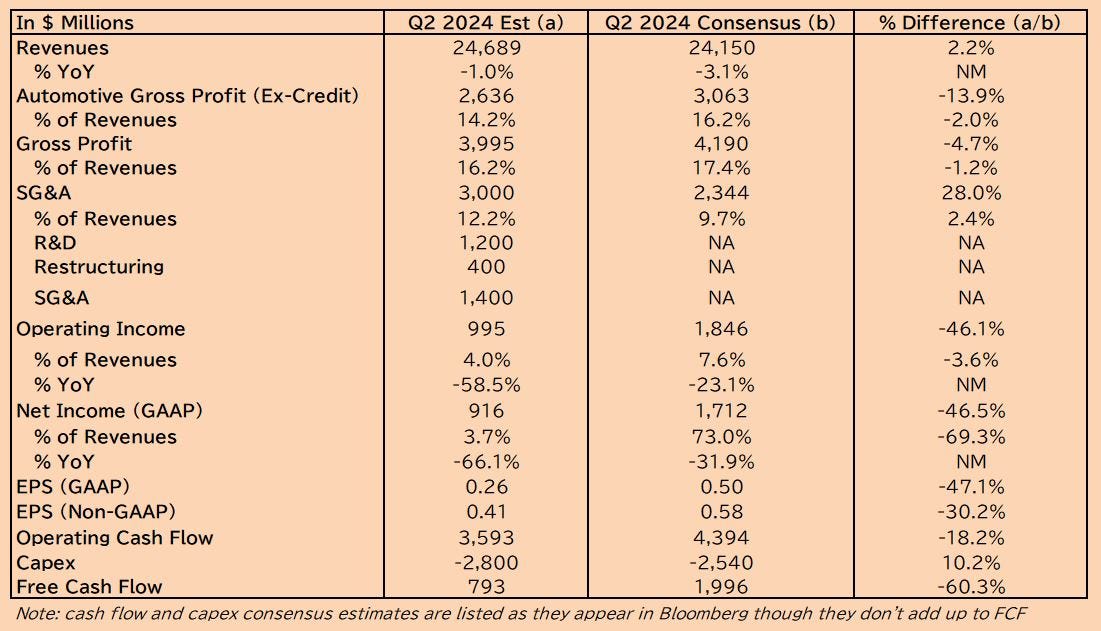

Given the above assumptions, I see Q2 non-GAAP EPS at $0.41, which is 30% below consensus estimates of $0.58. Note, that Q2 consensus EPS has risen by 3% since last week’s 2.4% beat in Q2 deliveries. It seems like an attempt by analysts to chase the stock price higher with their earnings estimates (one prominent Tesla bull raised his target price by 35% despite changing his 2024 EPS estimates by only 9%).

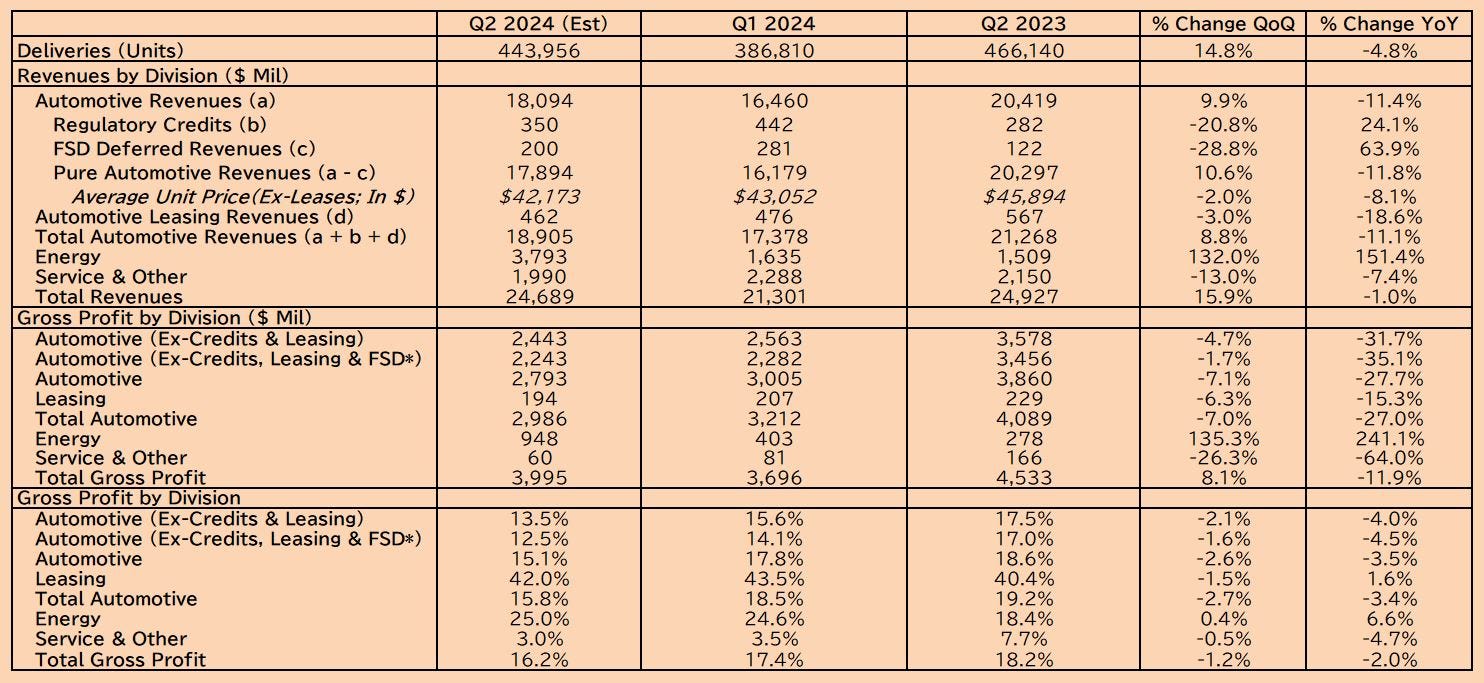

If this continues, Q2 earnings results could be a setup for the perfect rug pull. Figure 4 below shows details of my Automotive gross profit estimates while Figure 5 shows my Q2 earnings estimates versus consensus.

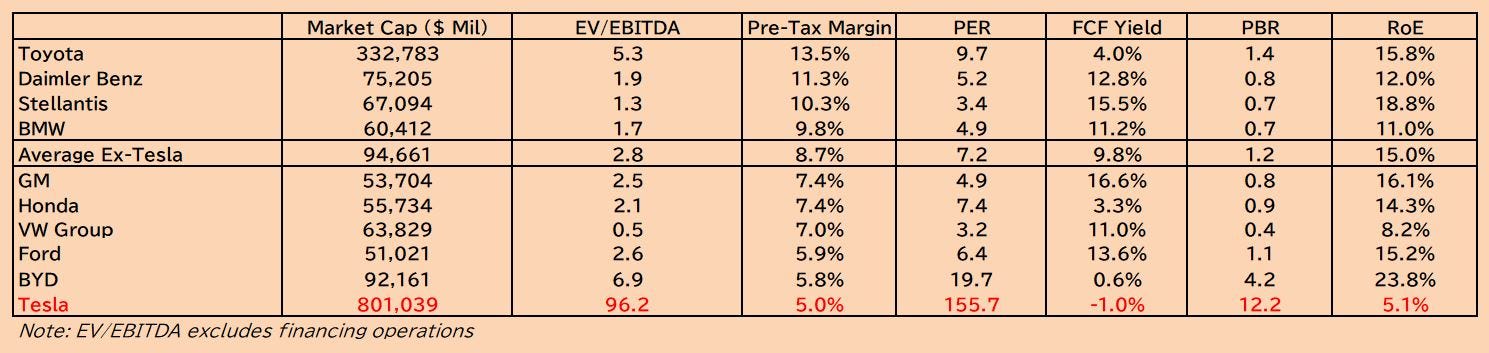

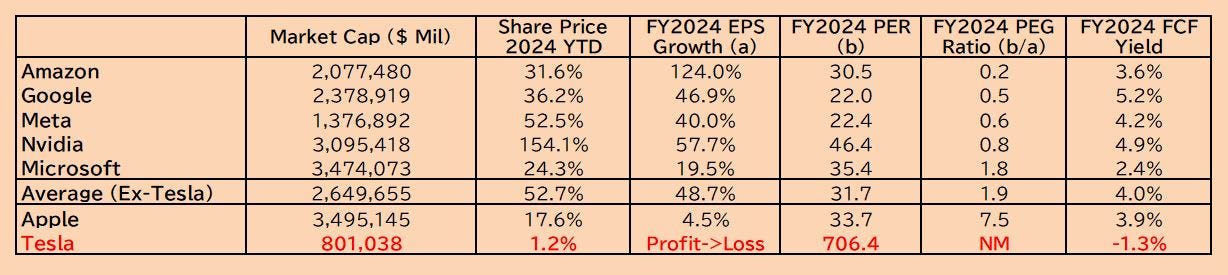

Figures 6 and 7 show Tesla’s profitability and valuations (based on my estimates) versus its rivals in the auto industry and true AI companies in the Magnificent 6. As can be seen, there is no argument for Tesla to trade at its current valuations based on these comparisons. If Tesla traded at 1x book value per share (rival automakers trade on average at 0.7x book), Tesla would be worth $20.

My basic thesis on Tesla’s demise is that no carmaker can survive 2 years without new models like Tesla is trying to do. Worse yet, 95% of Tesla’s global vehicle sales are based on only two models, which are so stale that Tesla has cut their prices every quarter since Q4 2022. Even if Tesla comes out with a new model that becomes a global hit, it could only stem the losses from the Model 3/Y’s decline. It will not likely lead to profit growth.

Given the intense competition in the auto industry—which has hundreds of players and massive excess capacity—Tesla may not survive, despite its AI ambitions (see my full report on how Tesla could go bankrupt here).

Figure 4: Revenues & Gross Profit By Segment

Figure 5: Q2 Earnings Estimates vs Consensus

Figure 6: Tesla’s Returns & Valuations vs Rival Carmakers

Figure 7: Tesla’s Returns & Valuations vs Mag 7 Rivals

Is there any info on their Opt*mus robot? I think it was Techbrew (who are big Elon simps) we’re talking up the size of the humanoid robot industry and how you know who was best placed to take advantage. Have I missed something as the last time it was a person in a spandex suit….

I appriciate your analysis. Tesla does not trade on fundamentals much in general, not at all lately. Is there enough (institutional) holders left that would consistently sell to offset the momo trade from retail going into the robotaxi day or maybe even beyond?