Tesla Weekly (9/13): "Much Ado About Nothing" Rally

Tesla Weekly (9/13): "Much Ado About Nothing" Rally

Excitement about China may have moved Tesla shares. But, what about the low-interest rate loans in China & the US? Q3 could be hit by these "stealth price cuts".

Tesla is up 9.1% through Thursday on lower-than-average volumes versus a 5.4% rise in the Nasdaq 100. There was no discernable catalyst behind this outperformance, which is normal for Tesla and is why it’s such a difficult stock to short, despite deteriorating fundamentals. Below are some possible reasons why Tesla went up so much this week.

The big jump occurred on Tuesday when Tesla spiked by 4.6% versus the Nasdaq 100’s rise of 0.9% and Nvidia’s increase of 1.5%.

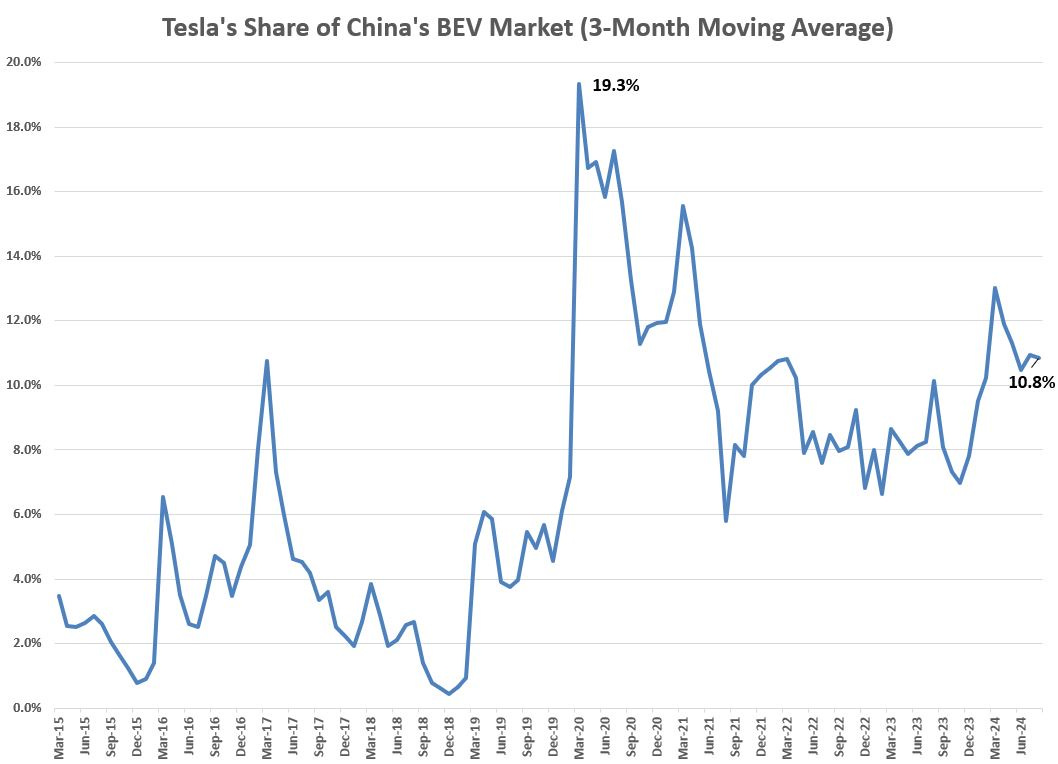

China Data?: Many attribute Tuesday’s spike in Tesla shares to the China domestic sales numbers that came out overnight, but this is doubtful: Tesla’s August domestic retail sales in China were down 1.9% YoY versus total battery electric vehicle (BEV) sales growth of 18.5% YoY. Figure 1 shows Tesla’s share of China’s BEV market. Not only is it uninspiring, but it’s also nearly halved from its March 2020 peak.

EU Tariffs?: Tuesday also had news about the EU further lowering tariffs on Teslas imported from China to 7.8% from 9.0% previously (and 21% before that in July), while Chinese EV makers like BYD, Geely, and others saw their tariffs maintained at high levels of around 30%. Nevertheless, this slightly lower tariff amounts to a mere $600 in savings per car that Tesla imports from China. Hardly a cause for celebration in my opinion.

Call Buying?: Given the thinner trading volume in Tesla this week, one thought is that the call buying drove the price up. And while this is likely the main reason behind Tesla’s surge this week (as usual when there’s no news), volumes in Tesla’s call options are down 14% versus Tuesday through Thursday last week (Monday was a holiday), while put volumes are down 18%.

China Weekly Data: Tuesday’s spike in Tesla shares also came after overnight news of Tesla’s insured vehicle sales in China from last week, which were up 51.4% versus the same week last year. BYD saw its sales fall by 27% from the previous week, which probably made Tesla’s 13% rise from last week look even better. However, Tesla’s numbers are actually underwhelming once analyzed: its rise in sales last week versus the same time last year was due to the Model 3 line in Shanghai having been shut down during Q3 2023 for retooling ahead of its “refreshed” version that went on sale last October (and quickly saw its price cut after weak demand).

My Trading This Week—Disciplined: I stuck to my main trading rule on Tesla this week: in the absence of solid catalysts (like quarterly earnings or events like AI Day, etc.) don’t short unless the RSI is near 70 (overbought territory) and always buy cover your short when the RSI is near 30 (oversold territory). Tesla’s current RSI is at a lukewarm 56. So, I didn’t touch my Tesla position this week and kept a stiff upper lip amid its rise. It was also obvious that the call buyers wanted the stock to stay above its 50-day moving average of $224, so it felt like it was better to stay put. Q3 deliveries on October 2nd will be the next catalyst (I don’t expect a significant overshoot of consensus estimates of 460,000, which might cause a sell-off because of no “beat”) and Robotaxi Day will be on October 10th. Robotaxi Day should be a good shorting opportunity as most Tesla thematic “Days” are excellent “buy the rumor, sell the news” events (see Figure 2).

Figure 1: Tesla’s Struggling Market Share in China

Source: CPCA

Figure 2: Robotaxi Day is on October 10th

Source: Tesla & Bloomberg

Tesla’s Low-Interest Rate Loan Programs Should Kill Q3 Margins

Tesla introduced a 1.99% loan program in the US last June to juice Q2 sales during the last month of the quarter. In China, Tesla rolled out a “0% for 5 years” loan program in June as well. Both were supposed to be just for the last month of Q2, but both were extended into Q3 for the full quarter. It should be noted that the US and China are Tesla’s two biggest markets and made up 69% of 1H 2024 revenues. And because the Model 3 and Y’s old age is crimping demand, these loan programs will likely not go away. Below are the main points about why this is bearish for Q3 earnings.

Price Cuts Had to Stop: After having cut prices every quarter since Q4 2022, Tesla finally realized that this was really killing its brand value and likely felt it would hit the residual value of its lease returns (amazingly, there haven’t been any write-downs on lease returns yet despite the 50% drop in used Tesla prices since their peak in July 2022).

Higher Costs Are Better Than Price Cuts: So, in order to keep the factories running (two of which are only 2.5 years old and have yet to run at over 50% of capacity), Tesla decided to use aggressive low-interest rate loans.

US Loan Program Same as 5% Price Cut: The spread between Tesla’s current 1.99% loan program and the 8.85% rate for buyers with “good” credit scores (Fico score between 640 and 679) amounts to roughly $2,180. This is the same as a 4.8% price cut, although Tesla has to pay for this spread so it will be booked at cost of goods sold (COGS). Including the new deal announced last night ($0 down at 2.45% APR), this should cost around $2,200 per Tesla sold in the US under such deals. Roughly 85% of Americans use financing to buy their cars, so this could be around a $300 million hit to profits in Q3 assuming Tesla sells 160,000 cars in the US.

China Loan Program Same as 4% Price Cut: The average car loan in China is around 6% and Tesla is offering a “0% for 5 years” loan program (as far as I know, none of the stronger Chinese EV makers are offering such aggressive incentives). The spread for this costs Tesla roughly $1,440 per vehicle sold (the equivalent of a 4.1% price cut) which is not as much as the US, but note that the price of a Tesla in China is the lowest in the world (the Model Y in China costs only $35,700 [with taxes], which is 20% lower than its US price of $44,900 [without taxes]). Tesla’s local sales in China barely make a profit, so this loan program might put them in the red if enough Chinese buyers use it. 50% of car buyers in China use financing. Applying that to Q3 sales estimates in China of 177,000 vehicles, this could amount to a $100 million hit to Tesla’s Q3 profits.

The Street Hasn’t Accounted For These Aggressive Loans: While the Street sees deliveries up 3.6% from Q2, they also see Q3 non-GAAP EPS rising by 16% QoQ for some reason. Retail investors (like the Tesla fanboy in Figure 3) actually think these low interest-rate loans are bullish for Tesla. I currently see Q3 non-GAAP EPS at $0.45 (25% lower than consensus at $0.60) and plan to be fully loaded with my short position on the day of results, depending on the share price (recall that even though Q2 results were worse than expected, Tesla had a huge relief rally thereafter due to it being down 42% YTD). But I’ll only make decisions on timing and size after the October 2nd delivery report for Q3.

Figure 3: Tesla Fanboys Celebrate Anything That Moves the Metal

Source: Twitter

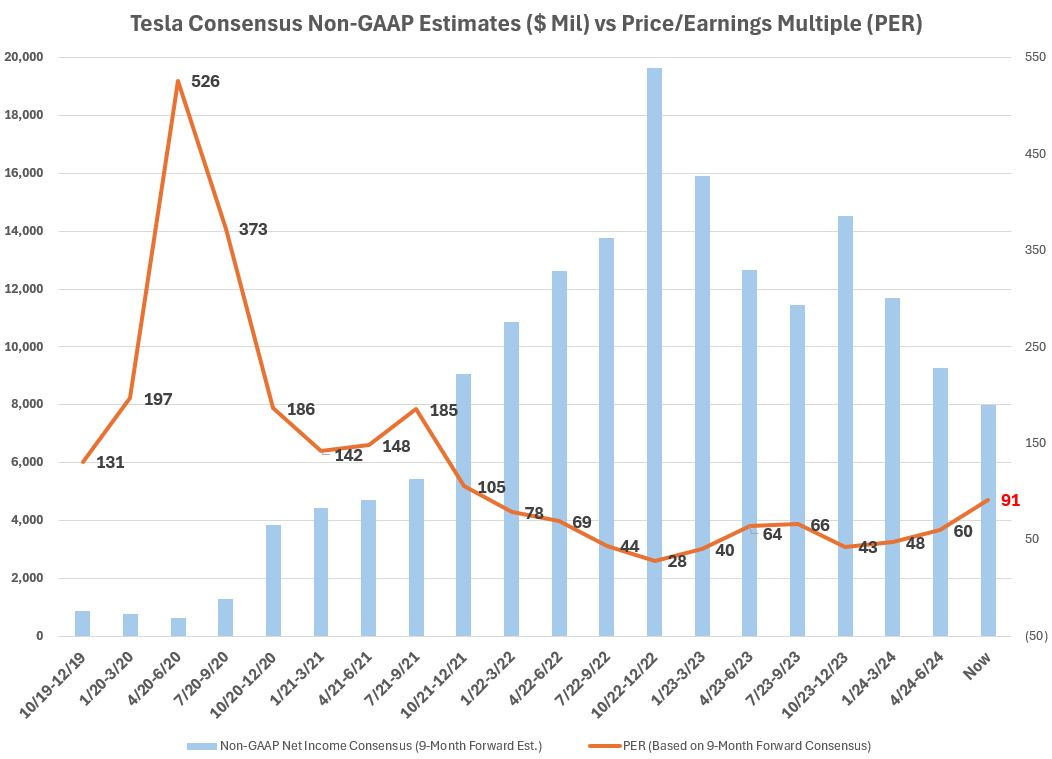

Tesla’s PER Rises Close to 2021 Levels of 105x

Despite the horrible fundamentals at Tesla, the share price is only down 7% this year while consensus estimates continue to drop after 1H pretax profits plunged by 40% YoY.

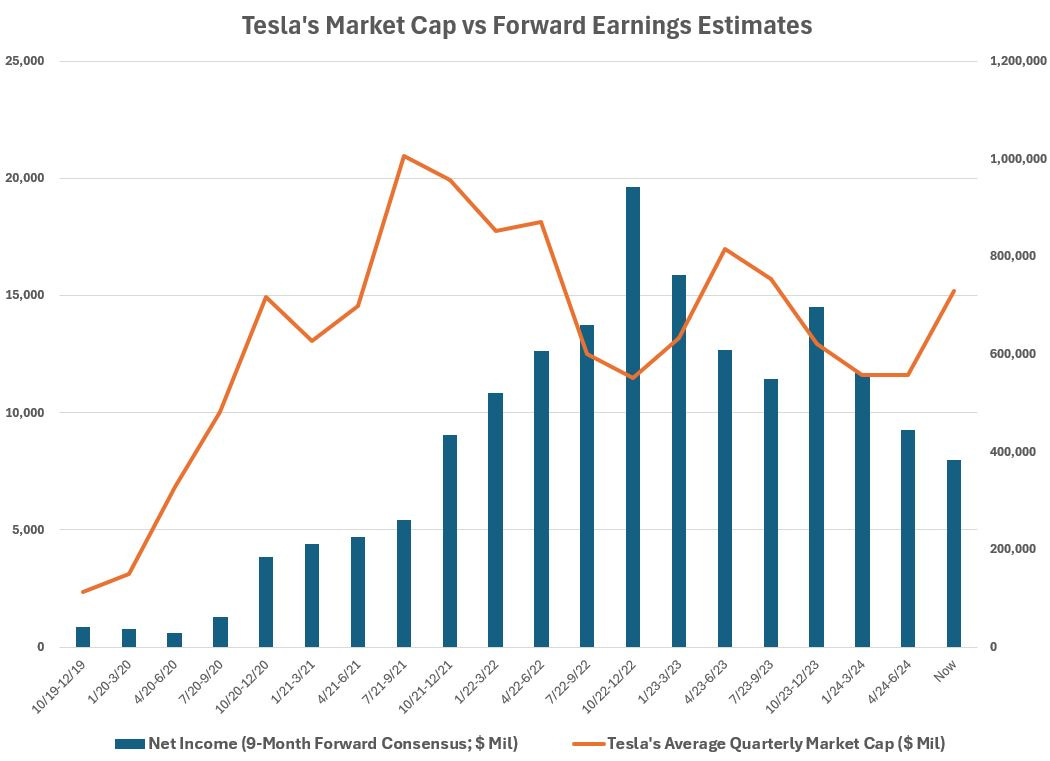

Figure 4 shows Tesla’s PER based on 9-month forward consensus estimates of non-GAAP net income. Figure 5 shows Tesla’s average quarterly market cap versus 9-month forward consensus net income estimates. It starts with Tesla’s average market cap in Q4 2019 (its first big profit beat) and 2020 consensus estimates. It changes to the next year’s estimates after every third quarter, as the Street seems to focus more on next year’s earnings after Q3.

It’s clear that at 28x 2023 consensus estimates back in Q4 2022, Tesla was a good trading buy and I regret not having covered my short at around $105 and going long. What’s interesting now, however, is that the stock is rising despite declining consensus estimates and deteriorating profit margins (see Figure 7). While the Street’s non-GAAP EPS estimates for 2025 are still overly optimistic ($3.14 versus my estimates of -$0.82), it’s interesting to see how much they’re dropping (see Figure 6). This is likely the main reason why Tesla has had trouble trading above $260 over the past 12 months.

Figure 4: Tesla’s PER Rises As Analyst Estimates Continue to Drop

Source: Tesla & Bloomberg

Figure 5: Tesla Trading Like It’s 2021

Source: Tesla & Bloomberg

Figure 6: Tesla’s 2025 EPS Estimates Are in Free Fall

Source: Bloomberg

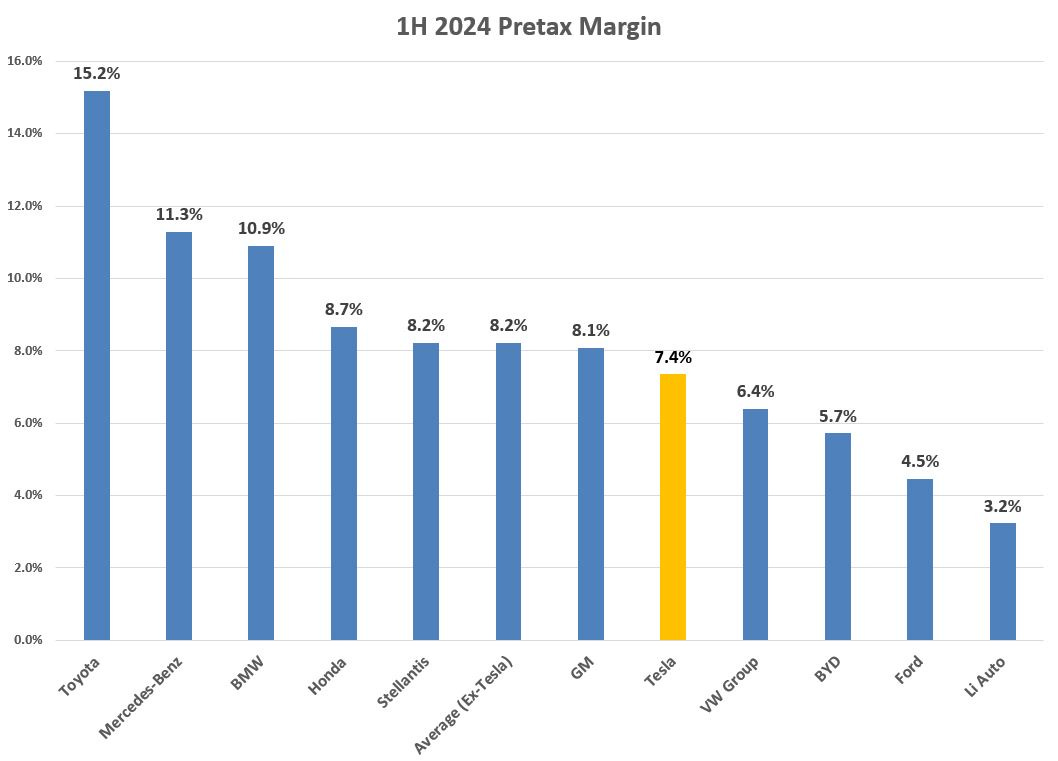

Figure 7: From Most Profitable in 2022 to Below Average Now

Source: Company data

Panasonic Announces 4680 Cell Mass Production

Panasonic announced that it will be mass producing its 4680 battery cells at its factory in Western Japan for Tesla from next month. Originally, it was scheduled to begin in July but was delayed.

This is positive for Tesla because they have been producing these cells in-house at a significant loss (Tesla has noted cell production as “earnings headwinds” in multiple quarterly releases since Q1 2023).

While Tesla proclaimed that they’d make their 4680 cells on their own, but would welcome any third-party suppliers back on Battery Day in 2020, it’s been a horrible mess for Tesla. And rightfully so. There’s a reason why there are only 5 main battery cell makers globally while the auto industry has over 100 players.

The main question in light of this news: Will Tesla put back the more affordable $61,000 Cybertruck variant on their order page? It was removed in early August, leaving the cheapest Cybertruck available now at $100,000.

Global Price Action: Chinese Win; Germans Lose

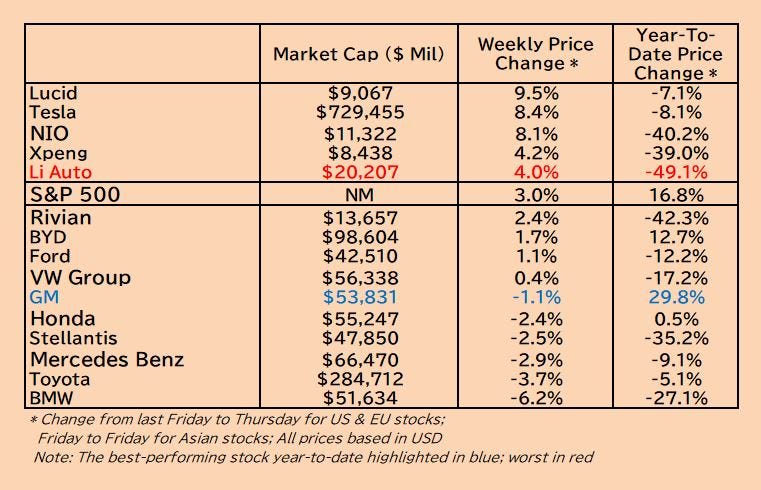

It’s become clear that investors are buying the dip in Chinese EV stocks like BYD, Li Auto, NIO, and Xpeng. They were the top performers for the third week in a row. Tesla seems to be included in these weekly gains among Chinese EV stocks most of the time, which is interesting.

Figure 8 shows the weekly price action among the major global carmakers and EV start-ups. Lucid is the top outperformer (with Tesla close behind), while BMW got dumped after its profit warning on Tuesday.

Conclusion: There’s serious dip-buying going on with the Chinese EV stocks and it doesn’t seem rational. The weakest (NIO and Xpeng) are rising the most, while the strongest (BYD and Li Auto) lag. I also understand that NIO and Xpeng were the worst performers over the past year, while Li Auto and BYD were the best, but it seems that the lower-quality Chinese EV stocks are getting bid up recently.

If China were to “make investing in China great again”, I’d be a buyer of BYD for its vertical integration and global expansion and Li Auto because of the huge growth in demand for hybrid vehicles (or in Li Auto’s case, extended-range electric vehicles [EREV]).

GM being the best-performing stock in my universe of “global majors” (see both Figures 8 and 9) makes me think that it may underperform most of the stocks in my universe next year unless earnings show signs of growth.

I would avoid the German Big-3 despite their bombed-out charts and seemingly “cheap” valuations, as they have over 66% of their earnings exposure to China and Europe, which are seeing intense price wars amid declining demand.

We’re heading into a recession—at least in the auto sector, based on what I’m seeing—and it’s risky to be long auto stocks in such a situation. However, if you’re running a pure automotive long/short portfolio, I would hedge my shorts in Tesla and others with longs in Honda, BYD, and Toyota, in that order.

Below is a brief summary of why Lucid was the best performer this week and why BMW was the worst.

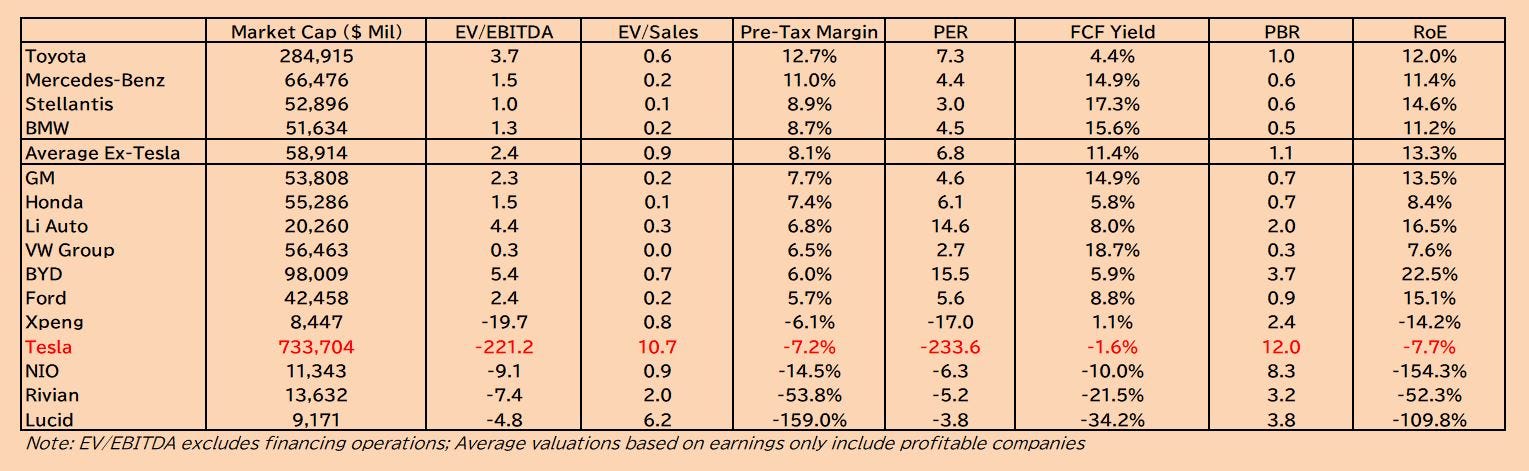

Lucid is the Best Performer This Week: Stock is up 9.5% this week after news came out of a technology event indicating Q3 sales are going better than expected, with management saying that sales as of August had reached 2023 levels. This indicates that Q3 volumes could reach 2,400 vehicles versus consensus estimates of 2,000 units. Lucid sold 6,000 cars in 2023 and consensus estimates see 2024 sales reaching 9,000 vehicles. The Gravity SUV—seen as a potential Tesla “Model Y killer”—could be a huge hit and is slated to see the start of production by year-end. I’ve often warned not to short Lucid given its free float of only 39% and high short interest (along with the fact that Saudi Arabia’s sovereign wealth fund owns 59% of Lucid and could take it private any time). But I also wouldn’t go long the stock given its high EV/sales ratio of 6.2x, which is second only to Tesla’s 10.2x (see Figure 9). But if the Gravity is priced reasonably, it could take share away from the Tesla Model Y and come closer to turning a profit. It’s worth watching this stock if it can manage such a turnaround, especially because of the high short interest.

BMW Plunges on Estimates & Recall: BMW issued a profit warning on Tuesday due to weak China sales and a recall of 1.5 million vehicles due to quality issues with their brakes. This led the Street to slash 2024 EPS estimates by around 18% and 2025 estimates by nearly 10%. I’ve warned before about the German Big-3 carmakers being value traps (see last week’s Tesla Weekly, especially the comment on Germany’s Big-3’s low valuations below Figure 7 here). They have over 2/3 of their profit exposure to China and the EU—the world’s weakest car markets. Both the Germans and the Chinese carmakers suffer from excess capacity at home, but at least BYD can increase profits by growing overseas sales. The Germans have already grown their overseas sales, mostly to China. I wouldn’t buy the dip in BMW just yet, but they will be introducing new models in the 2H of 2025 on a new platform, which should be amazing.

Figure 8: Best To Worst Weekly Price Action

Source: Bloomberg

Figure 9: Tesla Returns & Valuations vs Rivals (Ranked by Pretax Margins)

Source: Company data, broker research, & MH estimates

Figure 10: Tesla Returns & Valuations vs AI Leaders (Ranked by 2025 PEG Ratio)

Source: Company data, broker research, & MH estimates

Nice write up. Let's not forget the Delaware case which could really shake things up. I could easily see Elon taking his ball and going home if he loses again, vs appealing.

“value of its lease returns (amazingly, there haven’t been any write-downs on lease returns yet despite the 50% drop in used Tesla prices since their peak in July 2022” this is a big scandal lurking in the balance sheets