Tesla Q2 Results Miss And Profitability Hits a 10-Year Low

Tesla Q2 Results Miss And Profitability Hits a 10-Year Low

Tesla's 70% rally since Q1 increased its market cap by more than Toyota is worth...why?

Main Points

Tesla’s Q2 results were weaker than expected and the automotive business saw its lowest profitability since 2014.

Q2 non-GAAP EPS was $0.52 (-43% YoY) or 14% lower than the Street’s estimates of $0.60, but after stripping out record-high regulatory credits of $890 million and one-off restructuring charges of $622 million, Q2 EPS was only $0.46 or a whopping 24% below consensus estimates.

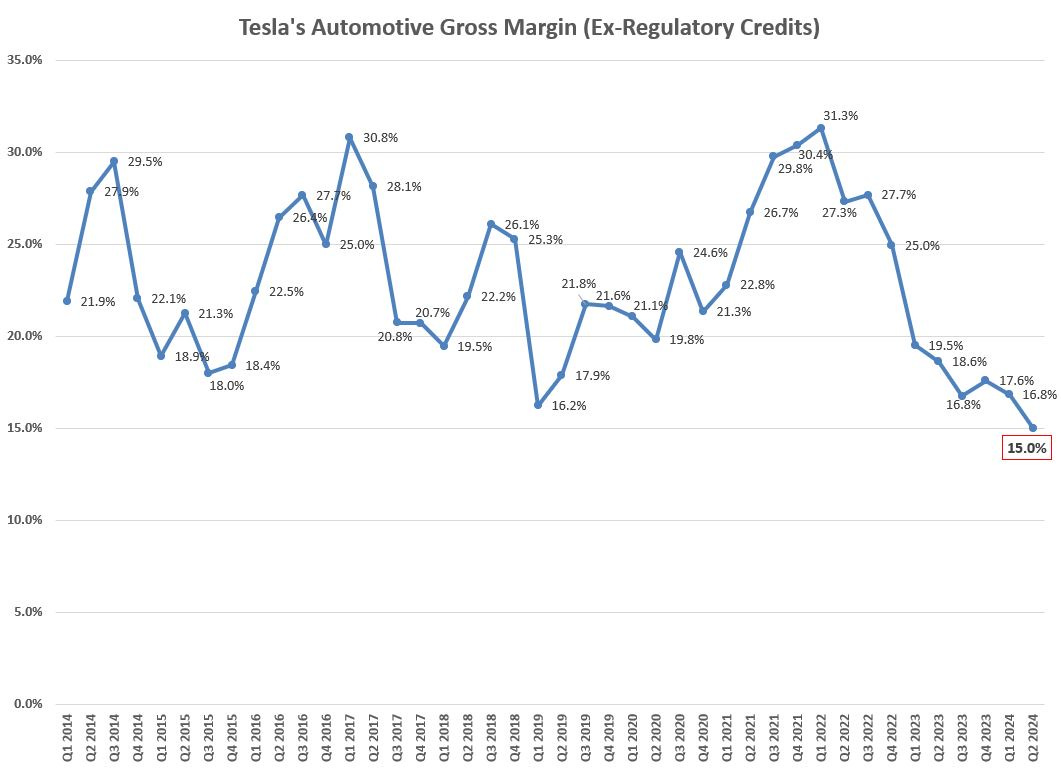

The core automotive business saw its gross margin drop to 15% (excluding regulatory credits), down from 16.8% in Q1 and 18.6% a year ago. It was the lowest margin since disclosures began in 2014. While average prices appear to have been flat, despite discounts, costs/unit rose by 1.7% QoQ due to Cybertruck losses. Tesla’s CFO said that, excluding Cybertruck losses, costs/unit were down sequentially.

Tesla saw its debt rise by $2.6 billion in Q2, proving that Tesla is not as cash-rich as some investors believe and is actively seeking cash.

Tesla’s Energy Division saved the day with its gross profit growing by 84% QoQ and 166% YoY. Unfortunately, there was little color on how, where, and why Tesla Energy generated such high earnings in Q2. There was also little detail given on where the growth would come from henceforth.

The “AI” theme was pumped hard on the earnings call, with Musk saying for the first time that they’re “doubling down” on their in-house AI supercomputer called “Dojo”. Up to now, Musk had said Dojo was a “long shot”.

After the earnings call and post-aftermarket close, Musk tweeted a poll on Twitter asking whether Tesla should “invest $5 billion into xAI, assuming the valuation is set by several credible outside investors?”. While this may sound bullish given the market’s obsession with all things “AI”, it could lead to equity financing, legal scrutiny, and shareholder lawsuits.

Since its Q1 earnings miss, Tesla’s stock has risen by 70% over roughly 3 months, adding $325 billion to its market cap (more than Toyota Motor’s current market value of $316 billion). Nevertheless, Tesla’s Q2 results were possibly one of its weakest in recent history.

In terms of profitability, Tesla’s Q2 automotive gross margin of 15.0% (excluding regulatory credits) was the lowest on record since such disclosures were made in 2014 (see Figure 2 to get a feeling of how bad this looks).

In a nutshell, these are the key variables behind Tesla’s weak Q2 results:

Regulatory credits surged by 101% QoQ, boosting Automotive gross profit by $448 million vs Q1.

Energy gross profit surged by 84% QoQ, or +$337 million vs Q1.

Automotive gross profit (ex-regulatory credits) was roughly flat vs Q1, despite a 12% QoQ increase in retail deliveries.

This led to a record-low Automotive gross margin (ex-credits) of 15% and a 43% YoY drop in non-GAAP EPS (ex-credits of $890 million & restructuring charges of $622 million).

The pronounced silence on new model launches and louder fanfare over Tesla’s pivot to “AI and robotics” on the earnings call helped push the stock down by nearly 8% in after-hours trading.

SolarCity Part Deux: Musk Loves xAI

The big question is what Musk’s tweet below (Figure 1), post-after-hour trading, does to the share price today. To me, this is as egregious of a grift as getting shareholders to sign off on Tesla’s 2016 take-over of the insolvent SolarCity, in which Musk was the top shareholder, along with his cousins, brother, and close Tesla Board members at the time.

With the intense hype over all things AI in the market these days, this Twitter poll of Musk’s might be a purposeful way of softening the blow to Tesla’s share price today after its horrible Q2 results and many unanswered questions on the earnings call. However, here are some questions that might raise some red flags:

Why wasn’t xAI started within Tesla (Musk said on the call that all xAI employees refused to work on AI at Tesla, so he had to create a start-up to hire them)?

How does a $5 billion investment in xAI from Tesla benefit Tesla shareholders, especially if it can be proven that Musk used Tesla resources to create xAI?

If Tesla invests in xAI—which is currently loss-making—how much further down does that bring Tesla’s net profit? $5 billion is 1/5 of xAI’s $25 billion valuation (according to Musk). This means it will likely be booked as an equity-method affiliate, which could further depress Tesla’s deteriorating pre-tax and net profit.

Finally, if xAI is folded into Tesla, how would that be accretive to Tesla’s already insane valuations (see Figures 4 and 5 below)?

Given how badly the auto business is doing, it begs the question of whether there will be a platform on which Musk can carry out his AI/robotic fantasies. Just look at Tesla’s 10-year-low Automotive gross margin (ex-credits) in Figure 2 below. The lack of effort in bolstering the car business with a solid, new product pipeline belies all of Musk’s AI/robotic ambitions. If there is a sudden recession—along the lines of 2008’s Great Financial Crisis—Tesla could face a larger downturn than other carmakers, given its huge outlays for investments in AI.

Figure 1: Musk Wants Shareholder Approval for Tesla to Buy xAI

Figure 2: Tesla’s Pure Automotive Profitability Hits a 10-Year Low

Source: Tesla

Most Significant Points About Tesla’s Q2 Results & Earnings Call

First, and foremost, I’d like to apologize for being way too bearish with my Tesla Q2 earnings forecasts (see Figure 3 below). My non-GAAP EPS estimates of $0.41 were 21% below Tesla’s result of $0.52. While my operating cash flow estimates were in-line with Tesla’s Q2 result, my capex estimates were 32% above Tesla’s Q2 investments. My key mistake was not estimating the huge regulatory credits that Tesla booked and the larger-than-expected restructuring charges. Adjusting for both, Tesla’s Q2 non-GAAP EPS would’ve been $0.46, or 12% above my $0.41 forecast.

Tesla’s Q2 results missed by 24%, excluding one-offs: Tesla’s Q2 results were impacted by two huge one-off factors: $890 million in regulatory credits (a record high) and $622 million in restructuring charges. Netting out both of these factors, Tesla’s Q2 non-GAAP EPS came in at $0.46 (-43% YoY) or 24% below the Street’s estimate of $0.60.

Record-High Regulatory Credits Boggle the Mind: Tesla booked $890 million of regulatory credits in Q2, a new historical high. These credits have nearly 100% profit margins and are earned from carmakers who must buy them from EV makers like Tesla because they don’t produce enough EVs themselves to satisfy global emission standards. In Q1 2022, Tesla booked its previous record-high credit revenues of $679 million, but this was due to one-off CAFE penalty payments and grandfather-claused regulations that were added to the tally. Q2’s all-time-high credit sales of $890 million were explained this way in Tesla’s Q2 Shareholders Deck: “We recognized record regulatory credit revenues in Q2 as other OEMs are still behind on meeting emissions requirements”. This is utter rubbish, as Q2 BEV sales were up by 11% YoY in the US, by 13% YoY in China, and flat in the EU (Tesla’s sales were down by 6% in the US, by 7% in China, and by 16% YoY in the EU). Stripping out Tesla’s dominant share of each major BEV market shows that Tesla saw huge declines, while other BEV makers saw double-digit growth. How does this lead to Tesla’s record-high booking of regulatory credits? Not one analyst on the earnings call asked about this.

Why regulatory credits should be stripped out from Tesla’s valuations: Many Tesla fans argue that regulatory credits are part of its business model and deserve to be factored into its valuations. This flies in the face of Musk’s tweet last week saying that Tesla doesn’t need subsidies (a sudden shift in sentiment likely due to his endorsement of Trump, who is against EV subsidies). Before Suzuki and Daihatsu grew their share of the Indian and ASEAN markets, respectively, both Japanese mini-car (or “kei”) makers traded at valuation discounts to Toyota, Honda, and Nissan, because they received subsidies from the Japanese government (mini-cars had higher mileage than regular cars at the time). Finally, what happens when subsidies disappear? Things fall apart swiftly. Germany ran out of BEV subsidies in December, which has led the German BEV market to drop by 16% YoY in the 1H of 2024 (Tesla sales there were down by 41% YoY), and the same happened in other countries that canceled BEV subsidies.

Musk reiterates his excuse for why Tesla Nvidia chips went to xAI: When asked about why Tesla diverted its $500 million Nvidia chip order to xAI (as reported by CNBC here and my take on Tesla’s Chair lying about it on CNBC two days later here), he repeated the same lame excuse he used after the CNBC scoop came out in early June: Tesla didn’t have enough space to store all of those GPUs. On yesterday’s earnings call, Musk—who was miffed by that question—said, “You can’t just order GPUs and turn them on. You need a base [to store them in]”. This, once again, begs the question of why Tesla would issue a $500 million order to Nvidia if Musk knew they didn’t have enough space to store the chips at Tesla’s global facilities.

Musk says Nvidia chips are too expensive; moving ahead with Dojo: Tesla is on track to have 85,000 Nvidia GPUs this year, an increase of 50,000 chips from last year’s levels. They spent $1 billion on chips in Q1 and $0.6 billion in Q2. The CFO said this would ramp further in the 2H of 2024, thereby reiterating Tesla’s capex plans of over $10 billion this year. But in what seemed like an about-face, Musk said on the call that Nvidia chips are too expensive and hard to source, so Tesla would push forward with development of its “Dojo” AI supercomputer. This is bullish news for the Tesla fanbase that thinks a 100x PER for a carmaker is “value” if you get robotaxis and humanoid robots with it. But, for those looking at Tesla’s deteriorating car business, one might ask where these chips will be built if Tesla’s Austin factory is foreclosed on. The same goes for Tesla’s robotaxi plans: if liquidity runs dry—and it sure seems like it has, given the $5.6 billion that Tesla has raised via ABS and debt in the past 12 months—where do robotaxis get built? Tesla’s global deliveries last year came to 1.8 million vehicles. Its capacity for the aging Model Y, alone, is currently at 1.68 million vehicles per year. This is not sustainable. It’s actually lethal for a carmaker facing slowing demand.

Tesla has financed nearly $6 billion in 12 months: Tesla saw its debt rise by $2.6 billion in Q2 (details to come in the 10-Q filing), proving that Tesla is not as cash-rich as some investors believe. In fact, since July 2023, Tesla has raised a total of $5.7 billion via asset-backed security deals and other forms of financing. While $30 billion of cash on hand sounds like a lot, 74% of that is wiped out by Accounts Payable and Accrued Liabilities.

Robotaxi Day scheduled for October 10th: Musk officially announced an October 10th date for the delayed “Robotaxi Day”, which was supposed to be on August 8th. He dissed GM’s Cruise for its abandoning a robotaxi product that had no steering wheel or pedals, saying that GM had no choice as they can’t do full self-driving anyway. Images of Tesla’s robotaxi show that it has no steering wheel or pedals, which is what Musk prefers.

No regulatory or operational roadmap for FSD or robotaxis: When asked what regulatory procedures would be needed to receive approval of running a robotaxi fleet, Musk had no clear answer. He said the Tesla App would summon a robotaxi and that all owners could lend their Teslas to the fleet. He gave no roadmap to how and where FSD would be approved, which was quite astounding, given all of his hype over each new iteration of FSD. In true form, however, Musk did (once again) predict that robotaxis would be out next year.

Figure 3: Tesla’s Q2 Results vs My Estimates & Consensus

Source: Tesla & Bloomberg

Outlook is More Negative Than Before

Aside from the fact that Tesla’s brand is tarnished by Musk’s endorsement of Donald Trump for President (California sales were down 24% YoY in Q2; see details here), the old age of Tesla’s fleet is becoming increasingly problematic.

This won’t change with little “tweaks” to the existing Model 3 and Y platforms. Little “tweaks” like those conducted on the Models S/X/3 have all ended in failure (massive price cuts and lower sales). And the “new models” that Tesla eagerly discussed in their Q1 Shareholder Deck (but skipped commenting on in the Q2 Deck for some reason), seem to be modified versions of the Model 3 and the Model Y in a cheaper format.

Such minor changes don’t lead to higher sales for old models in the auto industry, so it’s hard to see how Tesla will avoid massive cash burn from here on.

Regarding Q3 and Q4 this year, these are the two largest problems Tesla faces:

EU Tariffs: There is now a 21% tariff (on top of existing 10% import taxes) on any car imported from China. This means that Tesla’s China-made Model 3 will see its sales drop sharply in the EU. Tesla’s Shanghai plant shipped roughly 100,000 Model 3s to the EU in 2023 and 44,000 in the 1H of 2024 (the EU tariffs came into effect earlier this month). They already hiked prices to cover for part of this, but it’s useless given the weak demand for EVs in Europe and Tesla’s market saturation.

Falling Output in China, Tesla’s Most Profitable Factory: Given the EU tariffs on the Model 3 and weak demand in China, Tesla’s Shanghai factory—which made up an estimated 70% of global pre-tax profits last year—may struggle henceforth. Because the price cuts on Tesla cars sold in China are so large that they merely break even now, the huge profits made by exporting to the EU up to now will wither. And, while Tesla won’t talk about it, this is likely one of the biggest headwinds to its profits from here on.

As mentioned in my note last week, California appears to already be “done” with Tesla. The market is likely saturated there, but Musk’s politics have made things worse: Q2 Tesla sales in California were down by 24% YoY. Musk endorsed Trump’s presidential candidacy last weekend, so Q3 sales in California (12% of global sales and the fourth largest sales region for Tesla) could be worse.

The US was very firm for Tesla in Q2 and it was interesting to hear the CFO say that 2/3 of Teslas sold last quarter in the US were to first-time Tesla buyers. This explains how Tesla only saw a mild decline in US deliveries in Q2 versus the massive decline in California.

Figure 4: Tesla Returns & Valuations Vs Rival Carmakers

Figure 5: Tesla Returns & Valuations Vs AI Rivals

Note: Nothing in this report is investment advice.

Great article, thanks. Even the BBC News TV journalist today, couldn’t hide his incredulity, when reading the latest from Tesla ☺️

Imagine buying (or holding) Tesla shares because, ‘It’S NoT a CaR CoMpAnY,’ and then seeing AI being developed in a separate company 🙈

I don’t think that I have seen a clearer case of shareholder fraud, in my lifetime.

Nice summary. Bears have been predicting this for several years but we finally have substantive proof. The auto biz is dead and future quarters will probably be loss making.

I doubt Tesla Energy sustains those margins for more than a quarter. Increased volumes going forward but my guess is also decreased margins...and given how fast Tesla scaled their energy projects, there's no stopping someone like CATL from doing the same.

The xAI thing begs the question why it wasnt a joint venture between Tesla, Musk and others from the beginning? Personal enrichment. The eval is probably more inflated now meaning more personal enrichment for Mr. Musk.