Tesla: A List of Near-Term Negative Catalysts That Should Cap the Stock

Tesla: A List of Near-Term Negative Catalysts That Should Cap the Stock

This is why Tesla had a weak relief rally after Musk got his $47bn comp package re-ratified by shareholders last week. There are too many negatives facing Tesla.

The Weakest Relief Rally in Recent History

72% of Tesla Shareholders voted on June 13th to re-ratify Musk’s $47 billion pay package that a Delaware judge voided in January (I predicted the vote might not pass in a June 12th note, so apologies for being wrong).

This victory for Musk should’ve sent the stock to the moon, as it had been range-bound for 6 weeks ahead of the vote on concerns that Musk would leave Tesla with his “AI knowhow” for his AI startup, xAI (something which both Musk and his Board reminded [blackmailed?] investors about before the vote).

Tesla is only up 3% since the day before the vote took place on June 13th and down 10% since Musk made his surprise visit to Beijing on April 29th, when Tesla hit $199 intraday on rumors that the CCP approved FSD for use in China (proven to be false ever since).

This is the weakest relief rally I’ve ever seen. While it could go up more in the coming weeks, I doubt it as both the S&P 500 and the Nasdaq 100 are at historically high “overbought” levels right now. Besides, here are two factors that should weigh on the upside of Tesla’s stock price:

Fundamentals are much weaker in May than they were in April, pointing to a weaker Q2 and much lower 2H 2024 earnings. Q2 delivery consensus estimates are still 444,000 versus reality at a lower level of 414,000. Q2 adjusted EPS estimates are also very high at $0.58 (+71% QoQ despite lower pricing and restructuring charges) versus my estimates of $0.30. Tesla is expected to report Q2 results on July 19th.

The shareholders’ vote to re-ratify Musk’s 2018 pay package is simply a “fans’ vote of approval”. It has no legal bearing and likely will not sway the Delaware Chancery Court’s January 30th ruling to void it. The next hearing is on July 8th. A final ruling should come shortly thereafter.

If Delaware doesn’t reverse its ruling, Tesla will appeal and it will take years to resolve. If the Delaware Chancery reverses its ruling to approve Musk’s compensation plan, there will be lawsuits to oppose it. Hence, Musk is without his $47 billion comp package for a long time, which should lead him to favor xAI for his “AI” ventures, which is already clear (see picture below from Michael Dell’s tweet on June 18th). The whole “re-ratification” vote was simply a clown show.

Tesla Faces Huge Negative Catalysts From Here On

This is a short list of negative catalysts for Tesla in the next 6 months. The consensus estimates have yet to factor these headwinds in:

According to Tesla’s 2023 annual report, overseas pre-tax profits were 68% of global pre-tax profits. My estimate is that China was over 70% of Tesla’s 2023 global pre-tax profits and mostly from exporting to the EU and APAC at much higher prices than sales in China.

Tesla’s performance in China has been weak despite big price cuts at the start of Q2 which included a 5.7% reduction on the (refreshed) Model 3 and a 3.5% cut in the Model Y price. Tesla likely makes no profit on cars sold domestically in China, so this should hurt. Musk’s April 29th visit to Beijing was not about “FSD” as reported, but more about how to wind things down without firing too many Chinese employees (hence the new Megapack factory in China). The CCP is pushing its people to go back to working at factories. Hence the CCP’s concern about Tesla’s auto production and Tesla’s decision to build a Megapack (energy storage) factory to make up for the lower auto production.

Despite the April discounts, Tesla’s China delivery time was lowered to 1-3 weeks versus 3-6 weeks last week. 1-3 weeks means that there’s tons of inventory in China, given how big the country is.

China Model Y production was cut by 20% between March & June (March output was -18% YoY and April was -33% YoY) due to lack of demand in the EU, where Tesla’s sales are down 13% year-to-date (YTD). To make matters worse, Giga “Berlin” had to slow-roll production this month by idling the plant for 5 days. Aside from lower imports of the Model Y from China, the EU seems to be the worst market for Tesla. Even worse if the EU pushes through 21% tariffs on Tesla’s Chinese imports.

EU tariff hikes on China-made imports will come into effect from July 4th. This will be a 21% import tax for Tesla vs 10% up to now. It will negatively impact Q3 & Q4 profitability as cars shipped from low-cost China to high-priced Europe are over 100% of Tesla’s profits at its Shanghai factory (cars sold locally have close to zero profit margins). Giga “Berlin” has never operated above 50% of capacity since it opened in March 2022. It may be a matter of time until Tesla writes this $3 billion factory off.

The US traffic regulator (NHTSA) is Serious Now: NHTSA gave Tesla a deadline of July 1st to reply to its questions about why Tesla’s Autopilot/FSD recall flaws weren’t fixed. According to NHTSA, there were 20 more crashes since Tesla reported their OTA fixes last summer. This is not your usual NHTSA warning. They sent two statements in 12 days which purposefully contained language to arm every personal injury lawyer in the US to sue Tesla over Autopilot/FSD (there are over 90 lawsuits related to Autopilot/FSD outstanding in the US). NHTSA has it out for Tesla after getting snubbed by Tesla for over a decade.

I might be wrong, but I’ve never seen NHTSA this angry at an automotive company before. Surprisingly, NHTSA hasn’t ordered a recall of Autopilot/FSD yet, but these two reports (here & here) just 12 days apart from April 25th, show that they will if Tesla doesn’t comply. And it seems like Musk is snubbing his nose at NHTSA again, as he recently tweeted that Tesla would remove the “nag” from the steering wheel (which keeps drivers alert while using Autopilot/FSD).

The California DMV is moving to force Tesla to change the naming of its driver-assist technology from “Autopilot” and “Full Self-Driving” to a less “suggestive” name. Bloomberg broke the story (here) but has no date for when the CA DMV will act. It should be soon, given that it took the CA DMV over 6 years to draft its case. This won’t be good for Tesla given that Musk is trying desperately to pump FSD (to no avail) as the product that will keep Tesla afloat. Imagine what happens if the headlines say that “Autopilot” and “Full Self-Driving” are renamed as simply, “Cruise Control”.

Canada was 12% of Shanghai’s Exports in 2H of 2023 But is Set to Slump: Canada’s biggest “hotbed” for Tesla cars is British Columbia (BC), which just announced stricter controls of EV subsidies (EV incentives are now only for cars priced at CAD$ 50,000 and below vs CAD$ 55,000 before). If Tesla lowers the price of its Model 3 by CAD$ 1,000, it can continue to sell the Model 3 in BC with the incentives. The other models come nowhere near the new BC thresholds. Tesla has sent around 20,000 units per quarter of Tesla cars from China since the 2H of 2023 to sustain Giga Shanghai output. Like other countries, Canada is seeing lower EV demand. Even worse is Canada’s fading out of EV subsidies in 2025 and 2026. This will negatively impact profits at Tesla’s Shanghai factory.

Australia is Larger Than the UK or France: Tesla slashed prices in Australia 3 times in the 2 months since Q2 started. Why is this significant? Because Australia has become a huge export location for Tesla Shanghai, with Q1 deliveries of 12,789, which is higher than all EU regions except for Germany at 13,068. This news article about Tesla cars shipped from China baking under the sun in Melbourne should be a red flag (here). Note that exports of around 12,000/quarter to a country like Australia that only has a population of 26 million people is ridiculous. Exports to the UK from China were 12K cars in Q1 (population of 68 million) and 11K to France (population of 65 million). No surprise that News 7 from Australia published this picture below, which has been there since the start of Q2.

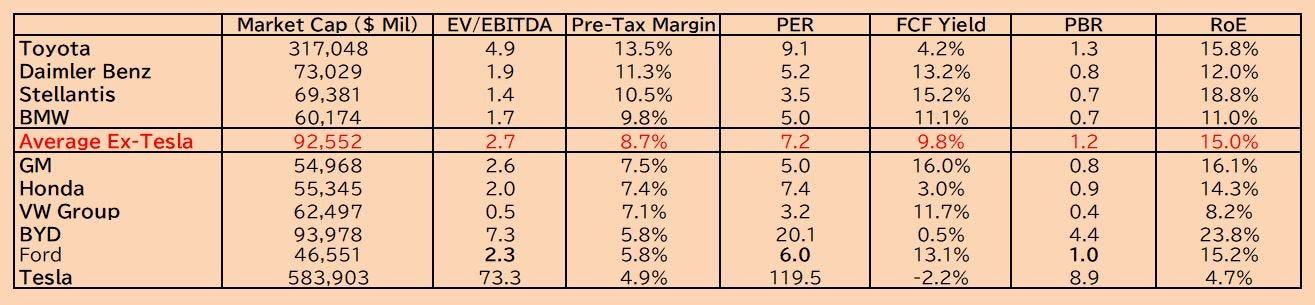

This is a long list of caveats, but they’re real risks. Yet Tesla still has a $587 billion valuation versus Toyota’s $307 billion (which sells 11 million cars per year versus Tesla’s 1.8 million). If Tesla were to trade at Toyota’s valuations, it should be fairly valued at $30 or $96 billion in market cap. The reason Tesla doesn’t trade along the valuation of other carmakers is likely as follows:

Investors believe that Tesla has AI capabilities (no disclosure).

Tesla’s AI prowess is proven by its FSD technology (a huge failure).

Musk keeps dangling FSD teases every year (market is adjusting to this).

Overall, I believe that Tesla currently trades at a $587 billion valuation (56x 2025 EPS versus Toyota’s 9x) because investors believe that Tesla has AI capabilities. I think they have no such capabilities and will publish a report next week on why Tesla’s “Full Self-Driving” product is not only a scam, but also a major legal liability.

Tesla vs The Magnificent 6

Tesla vs Rival Carmakers

Options have been stacking puts again. We saw this in Q1. So if there's a lot of put delta adding downward pressure going into Q2 earnings, I'd be careful. Of course, an equity raise or some big event that can trigger a selloff would cause a huge gamma squeeze downward.

Rumors that our boy has some kompromat on Buttigieg.

Most countries do not put their best & brightest as Transportation Secretary...no exception here.