Diary of a Tesla Short Seller: Musk's Desperate FSD Pump

Diary of a Tesla Short Seller: Musk's Desperate FSD Pump

The Tesla CEO shines a huge spotlight on FSD this week in a herculean effort to divert attention from Tesla's ailing car business & try to highlight Tesla's "AI" capabilities

Weak sales and production cuts in China sent Tesla shares tumbling to their low for this year of $162.50 on March 14th. Musk responded by diverting attention from this by spotlighting the advances in Tesla’s Full Self-Driving (FSD) driver-assist product. This spiked the stock in recent weeks.

Musk also mandated Tesla sales staff to carry out an FSD demo for customers taking delivery this week, even if it “slows down the delivery process”. This could serve as an excuse for weak Q1 sales and allow Musk to rave about how customers were “blown away” by FSD on the Q1 earnings call. This would ensure further FSD hype among retail investors.

Tesla influencers have been singing praises about how close the new version of FSD is to full autonomy. One hedge fund manager said it was “Tesla’s ChatGPT moment”.

The truth is that FSD’s new version appears to be worse than its previous one. FSD beta testers have damaged rims from running into curbs while turning corners. FSD is rated as “Poor” in a recent study of driver-assist systems by the non-profit IIHS (see Figure 6).

This FSD pump may get retail investors and some institutional investors excited, so if you’re short Tesla, it’s worth monitoring. Ultimately, the deteriorating fundamentals at Tesla (high fixed costs amid faltering growth) should lead to a continued sell-off of this overvalued auto stock (see Figure 9).

Not a Car Company. An “AI Company”

Sales conditions at Tesla are rapidly deteriorating and Musk sprung into defense mode on Monday in an attempt to pump Tesla’s share price. His ploy this time is to divert attention from Tesla’s weak auto business by shining the spotlight on Tesla’s Full Self-Driving (FSD) product, a $12,000 driver-assist option available for Tesla cars either at the time of purchase or on a subscription basis for $199 per month.

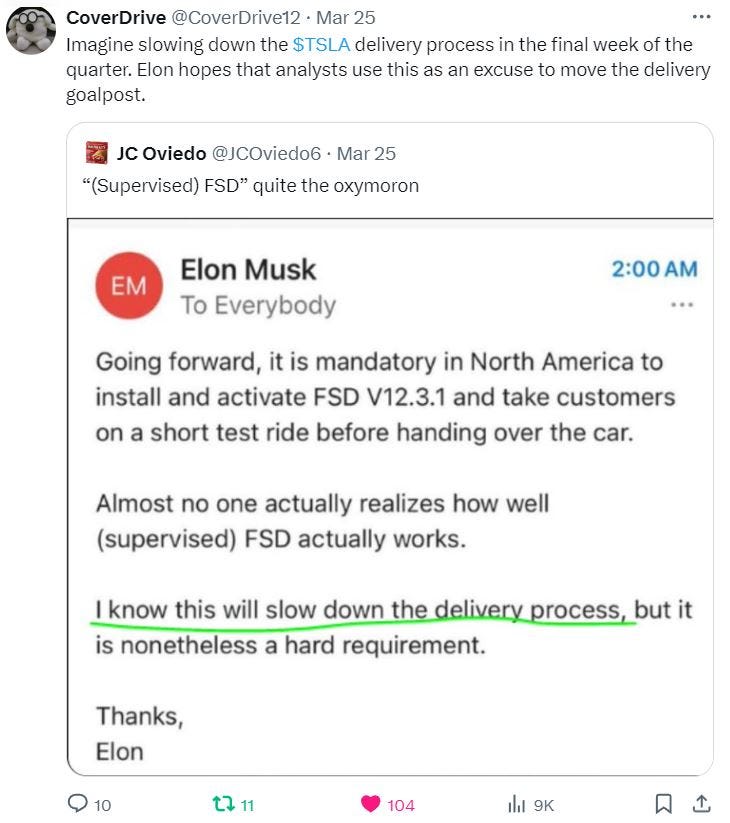

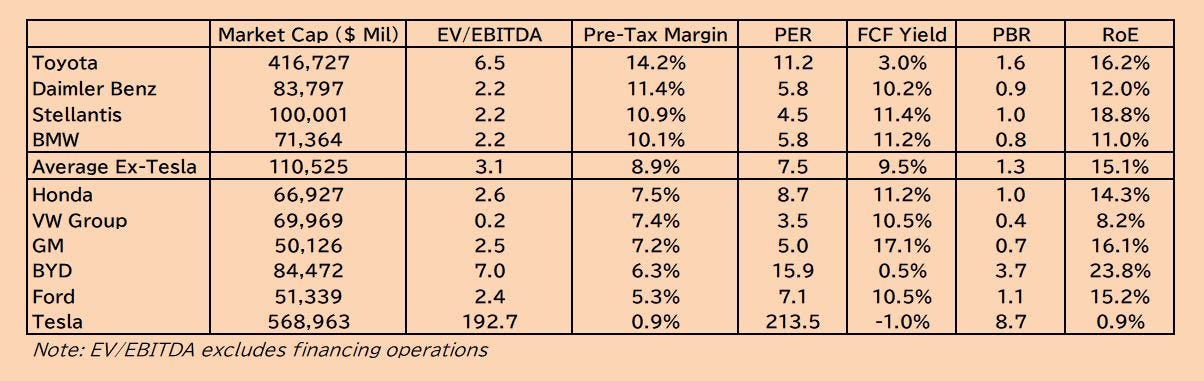

Tesla fans consider FSD the “AI” part of Tesla which warrants a premium in Tesla’s valuations of 28x that of normal automakers (see Figure 9 below). Musk himself said that Tesla would be worth nothing without it. He not only leaked an internal email about it (see Figure 1) on Monday, but tweeted about it 3 or 4 times later that day, with the final one climaxing with a one-month free trial offer for any Tesla owner in North America (the only region where FSD is street-legal).

So far, the pump has worked. Tesla’s shares rose by 5.3% this week and Tesla options traded on huge volumes for the first time in a long while. This is a clear sign that Musk needs Tesla to trade higher, possibly in order to elevate it ahead of a weak Q1 delivery report on April 2, as well as bad Q1 earnings results a bit over 2 weeks later.

The higher Tesla rests ahead of bad earnings later in April, the higher it is after whatever sell-off it has on the bad news. Tesla likely needs cash, so this FSD pump is very important if Musk is eyeing a public offering.

Musk Demands Customers Receive FSD Demos

On Monday at 2:00 his time, Musk sent out an internal email to employees saying “it is mandatory in North America to install and activate [FSD] and take customers on a short test ride” (see Figure 1). There’s a lot to unpack here, but let’s focus on the biggest red flags.

Figure 1: Musk’s Leaked Email on Mandatory FSD Test Drives

Tesla usually ships nearly 60% of quarterly deliveries in the last month of the quarter: Musk says in his email that these FSD test drives at the time of delivery will slow down the delivery process, but it is “nonetheless a hard requirement”. In my 8 years of covering Tesla, I have only seen Musk shove as many shipments as possible into the end of each quarter so that quarterly delivery numbers would look as rosy as possible. This is why his sudden willingness to hamper the quarter-end pump is a bit suspicious. Over the last 3 years, Tesla on average has seen 58% of quarterly deliveries in the last month of the quarter. Things have improved in the last 3 quarters, with only 42% of quarterly deliveries made in the last month of the quarter.

Slow deliveries due to FSD demo could be used as an excuse for weak Q1 deliveries: Musk’s willingness to slow down deliveries in the last week of the quarter is highly odd and may have less to do with marketing FSD to new customers and more to do with being able to use it as an excuse for weak Q1 deliveries.

Step 1 in a concentrated effort to pump Tesla as an “AI company”: I have no doubt in my mind that Musk will talk about how many customers were blown away by the FSD test drives on the upcoming Q1 earnings call. We’ll never know though, as Tesla doesn’t disclose FSD take rates or revenues, so he can say whatever he wants. After slashing Tesla car prices by 20% in January 2023, Musk went on the Q4 2022 earnings call weeks later and pontificated about the "price elasticity of Tesla demand” and said that orders were 2x output. Nevertheless, Tesla had to slash prices every quarter since then.

FSD v12.3 Rallies Fanbase But Big Problems Remain

Musk’s rallying of the fanbase via the latest version of FSD (version 12.3 or “v12.3”) is an effort to shift attention away from the bad fundamentals and give investors something to hang onto as Tesla’s car business flounders.

The stock hit a year-to-date low of $162.50 on March 14th due to the pile-up of negative news flow in recent weeks:

Bad weekly sales data from China indicating the 1H of March was down 28% YoY and that Q1 was pointing to being down 6% YoY.

A Bloomberg scoop revealed Tesla’s Shanghai factory had cut production by 23% as of mid-March due to EV price wars in China and weak exports.

TroyTeslike, a prominent Tesla research account on Twitter, reported estimates of Tesla’s Q1 global deliveries likely being way below consensus estimates of 458,413.

Because of this, Musk pumped FSD hard on Twitter this week most likely because he wants Tesla to be engraved into the AI sector of the stock market and needs to preempt bad Q1 results possibly in order to finance thereafter.

In a strange state of amazement, I watched multiple Tesla influencers with hundreds of thousands of followers toe the Tesla party line, proclaiming “This is a major step-change towards Robotaxis. This is Tesla’s ChatGPT moment”. It was like watching Kremlin propaganda being disseminated.

Musk’s FSD pump caused Tesla to have a steep 6.7% bounce in the first hour of trading on Tuesday, although it faded into the market close and was only up by 2.9% on the day. I’m skeptical about whether this FSD rally can continue and whether the FSD theme can mask the horrible earnings situation at Tesla right now.

Aside from Tesla refusing to disclose any data collected by its FSD beta testing to prove that it’s a leading autonomous driving technology, these are my main gripes about Tesla FSD:

The name “Full Self-Driving” was ruled illegal in California and is awaiting a long overdue ruling by the state’s regulator (DMV) on whether to ban it. California made up 13% of Tesla’s global sales last year, so if the DMV bans Tesla sales over FSD—doubtful, but a distinct possibility—it could hit Tesla’s earnings hard. In order to avoid this, Tesla would have to change the naming of FSD.

Google’s Waymo can and does drive its cars as robotaxis. Tesla is nowhere near that.

FSD is currently under probes by the Department of Justice and the Securities and Exchange Commission.

Tesla itself devotes around 3,600 words in its owner’s manual to “limitations and warnings” related to using FSD, while Musk constantly touts it as a “hands-free” driver-assist system.

And, most importantly: assuming Tesla deems FSD as having reached "full autonomy”, will Tesla actually take full liability in the event of any accidents or fatalities? Given the 65 lawsuits in the US related to Tesla’s Autopilot and FSD, I highly doubt it.

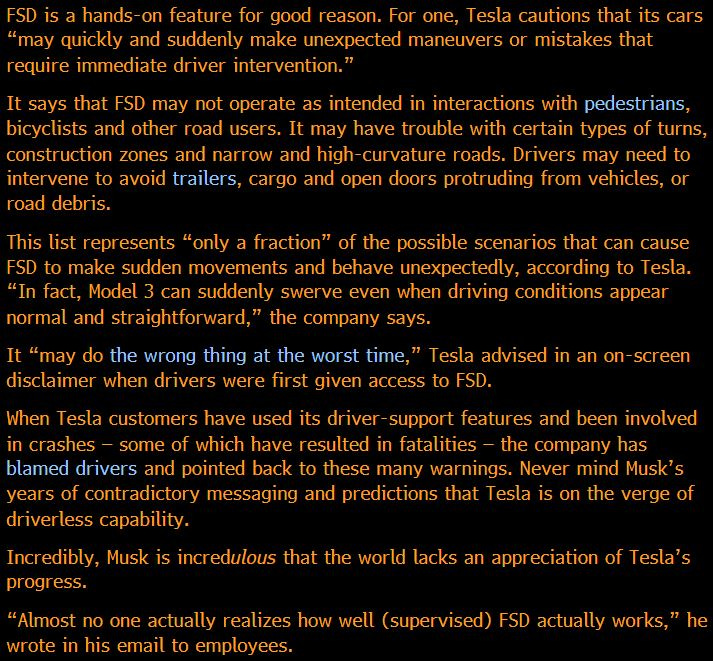

Bloomberg’s Craig Trudell wrote a great article on the controversies surrounding Tesla’s FSD the other day (link here) and it’s worth just reading this passage to understand how half-baked FSD is as a full autonomy software:

Figure 2: The Problems With FSD

Musk’s number one FSD surrogate, Omar Qazi, who goes under the name of “Whole Mars Catalog” on Twitter, has been uploading videos of his extensive drives on FSD to YouTube for years. It was interesting to see this tweet from him back in late 2022 saying FSD could “try to kill you” (see Figure 3), although it should be noted that FSD back then was many iterations behind the current v12.3.

Figure 3: FSD “Will at Some Point Randomly Kill You”

And while Musk’s FSD stock pump this week escalated, some pretty bad news about its new version 12.3 came out. FSD beta testers (all Tesla customers, who aren’t professional testers or on Tesla’s payroll) began having dangerous experiences, including the car trying to run into oncoming traffic.

One interesting feature is the number of FSD beta testers who ruined their rims while trying to turn corners. FSD v12.3 apparently turns corners too tightly (see Figure 4). Some have jokingly speculated that this was a feature of FSD v12.3 to get Tesla’s parts business more money due to all the rim replacements it would generate.

Figure 4: FSD v12.3 Likes Hitting Curbs While Cornering

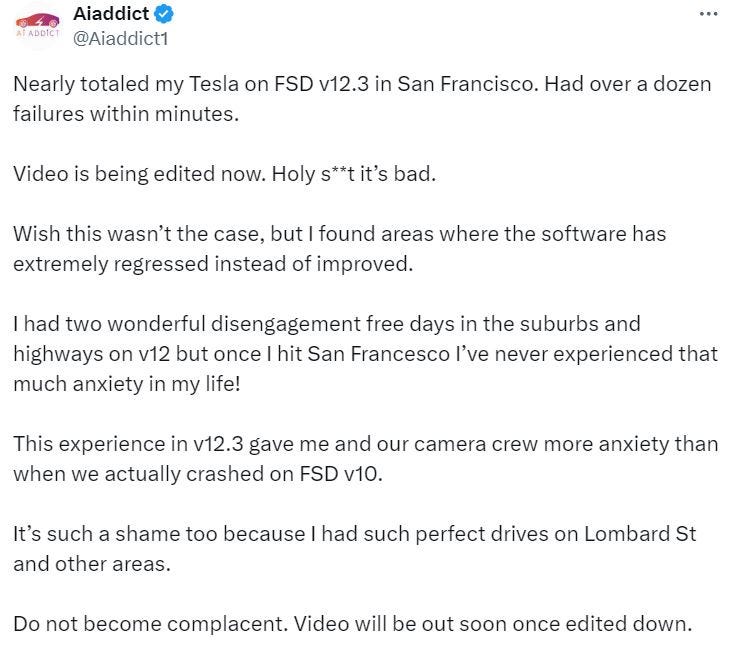

The Twitter account run by “AI Addict” is a man who used to work in Tesla’s Autopilot division (he was fired after uploading videos he took of his Tesla doing dangerous things on FSD) and he went from being extremely positive about FSD v12.3 initially to being shocked by how dangerous it is (see Figure 5).

Figure 5: Former Tesla Autopilot Employee Slams FSD v12.3

The Insurance Institute for Highway Safety (IIHS) is a non-profit organization funded by the US insurance industry (because the US transportation authority [NHTSA] has no guidelines). In a recent study of automakers’ driver-assist systems, it rated Tesla’s FSD as “Poor”. The only carmaker with an overall “Adequate” rating—IIHS’s highest—surprisingly was Toyota (see Figure 6).

Figure 6: Tesla FSD Ranked as “Poor” in Recent IIHS Study

Source: IIHS

Implications of the Musk FSD Pump: Trade Carefully

My gut feeling is that the bad fundamentals at Tesla will continue to weigh on the share price and this FSD hype will die down. However, we have a desperate and spiteful man engineering this rally on an “AI” theme in order to save himself, so it does warrant some vigilance.

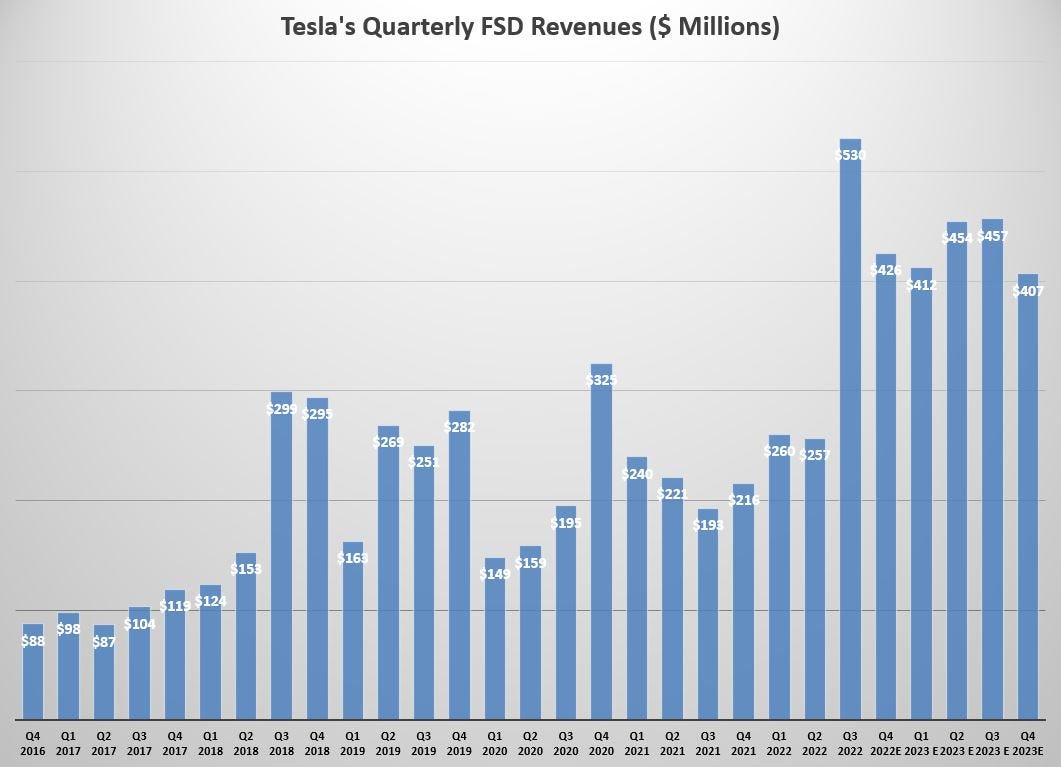

If the geniuses among Tesla influencers had any financial analytical skills, they’d be tweeting and YouTubing how much FSD actually generates in revenues (see Figure 7).

Using TroyTeslike’s FSD take rate estimates (which he stopped publishing in Q3 2022) and the price of FSD each quarter (it started at $3,000 in Q4 2016 and peaked at $15,000 last August before Tesla cut the price by 20% to $12,000 now), one can estimate that Tesla likely made around $1.3 billion on FSD in 2022 and 2023. Given that FSD generates “software profit margins” of around 90%, FSD could’ve made up some 16% of Tesla’s 2023 non-GAAP net income.

Figure 7: Tesla’s FSD Revenues (including Enhanced Autopilot)

Source: TroyTeslike & Tesla through Q3 2022; My estimates of 6.5% take rate from Q4 2022 through Q4 2023 & Tesla’s published prices

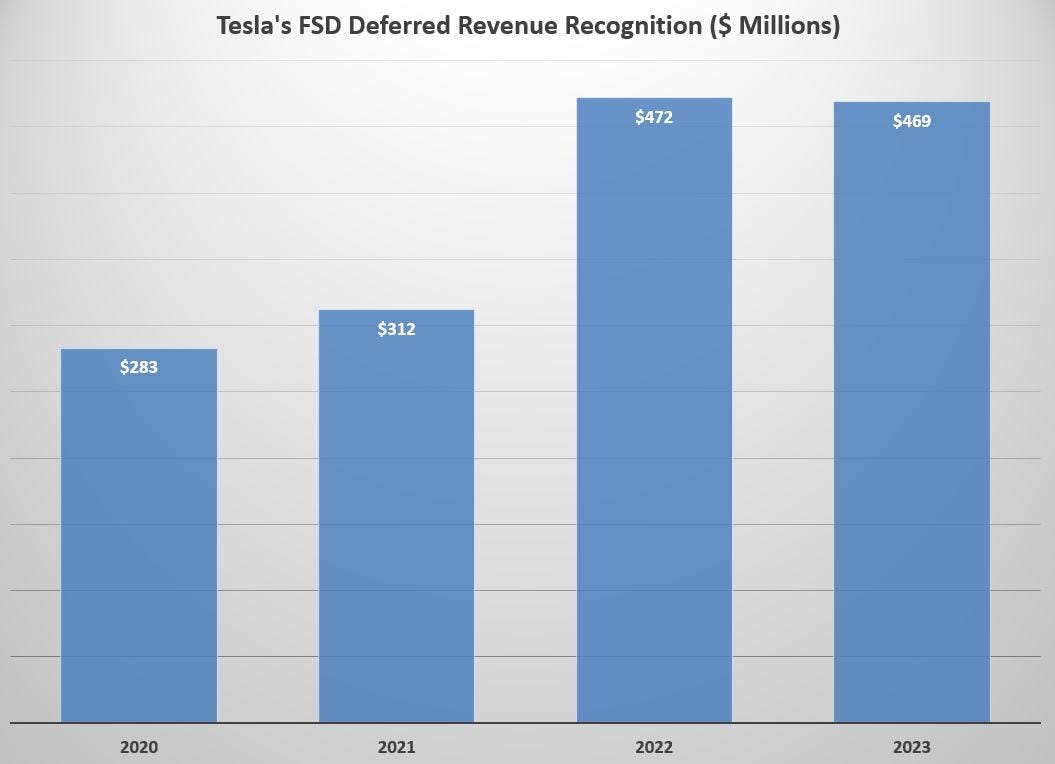

Mind the FSD Deferred Revenue Recognition in Tough Times

I expect Tesla to be aggressive in their booking of deferred FSD revenues this year, which could be as much as $926 million, based on how much they said they plan to recognize over the next 12 months in their 10-K (note that Tesla has only booked 50% of such plans since 2020, but last year actually booked 73% of what they stated in their 2022 10-K).

Tesla books deferred FSD revenues each quarter in its automotive segment and the bulk of it drops in the fourth quarter (not so in 2023 for some reason). Tesla has stated in past earnings calls (when Zach Kirkhorn was CFO) that they recognize deferred FSD revenues based on (a) technological milestones and (b) the span of release of FSD to its customer base. Despite a huge increase of both last year, it’s interesting that deferred FSD revenue recognition in 2023 was slightly down YoY (see Figure 8).

In their quarterly reports, Tesla discloses both how much deferred FSD revenues were recognized (FSD is clumped into automotive deferred revenues, which include Supercharging revenues, etc., but the bulk is FSD) and how much they plan to recognize over the next 12 months. Since 2020, Tesla has recognized on average 50% of what they stated they planned to the previous year but hit a record 73.4% of what they planned in 2022 during last fiscal year.

Tesla does not disclose deferred FSD revenues in their quarterly Shareholders Deck which comes out the day of quarterly earnings announcements, so both automotive revenues and average selling prices are unknown as of the earnings release. But they do give numbers in their 10-Q filings which come out roughly a week later. So, both real pricing and real profitability are unknown until the 10-Q comes out.

Figure 8: Tesla Can Juice Profits Via Deferred FSD Revenues

Source: Tesla

Even Hyping FSD Leaves Tesla Over 2x Nvidia’s Valuations

Even if FSD were to see its take rate in North America rise to 50% of deliveries, it would add an estimated $2.83 to 2024 EPS and $2.21 to 2025 EPS. On this basis, my non-GAAP EPS estimates for 2024 of $0.95 and -$0.77 for 2025 would lead Tesla to trade at a 2024 PER of 48x and a 2025 PER of 125x. Nvidia trades at a 2024 PER of 36x consensus estimates and a 2025 PER of 30x.

I see no reason for Tesla to trade at a premium to Nvidia, even if it is considered to be an “AI” stock due to FSD. Nvidia is massively more profitable than Tesla and it doesn’t have the burden of keeping a capital-intensive auto manufacturing business afloat.

Figure 9: Valuations & Returns Ranked by 2024 Pre-Tax Margins

Figure 10: The Magnificent 7 Valuations & Returns

Note: Nothing in the above report is investment advice.

It seems like they are in a catch 22 in that if they start to promote FSD too much including revenue recogntition, it would be admitting culpability in the lawsuits.

Is FSD still an additional 10k to the consumer to buy, on what is the same hardware? If so, then mandating salespeople show it off during test rides does seem, well, logical.