Diary of a Tesla Short Seller--34% Spike in 4 Days After a Bad Q1 Is a Gift for Shorts

Diary of a Tesla Short Seller--34% Spike in 4 Days After a Bad Q1 Is a Gift for Shorts

Tesla rose as much as 34% in 4 days after weak Q1 results in what was the most orchestrated stock pump since its IPO. It seems important for Tesla to stay above $140

Tesla’s North Scottsdale delivery lot is 110% full. H/T: @ValueExpected

An Epic 37% Pump in Four Days

It’s been years since I’ve seen Musk pump Tesla’s stock as hard as he did in the past 6 trading days. TSLA 0.00%↑ rose by as much as 37% in 4 days after Tesla’s earnings call on April 23rd. If you think this is just normal stuff, think about the amount of money that changed hands on Monday after Musk posted a selfie with him & Li Qiang: Tesla’s market cap rose by $97 billion, which is nearly twice the market cap of General Motors. In normal countries, there would at least be investigations into this.

And, let’s look at the main facts surrounding the well-orchestrated pumps on the Q1 earnings call, which led to this parabolic rise:

“Deliveries will grow year-over-year”: Musk said, “I think we’ll have higher sales this year than last year.” This is a brazen forecast that borders on subterfuge in light of April sales in China falling by 32% YoY, EU sales in March having plunged by 35% YoY and US revenues in Q1 having dropped by 13% YoY—more than any other major region.

New models in early 2025 (impossible): Musk said that Tesla would launch “new models” in “early 2025” which is impossible (new models require 4 years of development and Tesla has proven they need more than that) but the retail investors who have little knowledge of model cycles lapped it up.

Positive Free Cash Flow (FCF) from Q2 (No Way): The CFO said FCF would turn positive in Q2 after a negative $2.53 billion print in Q1 due to huge inventory. This also ticks the box among “reassurances needed to pump the stock” but is highly suspicious given that the CFO knows that Tesla faces Q2 restructuring charges (over $350 million according to Tesla’s 10-Q) and discounts are needed to clear record-high inventory, which, in turn, will lead to lower operating rates. Even if the -$2.7 billion drag from Q1 inventory build is removed from operating cash flow, FCF still would’ve barely broken even.

These three statements—all of which could be excused as “aspirational” if they don’t come true—were enough to send the stock up 16% over the next three days. Then came the clincher: Elon Musk’s April 29th surprise visit to Beijing, where his meeting with Premier Li Qiang paved the way for Tesla’s Full Self-Driving (FSD) driver-assist product to be sold in China.

Because Musk has been promoting FSD with all of his might and because it was thought that the CCP would never allow FSD to be sold in China (due to national security issues involving local data collection), the stock soared another 15% on Monday.

While the stock was up as much as 37% since reporting a horrible set of Q1 numbers, it has since given back 9% after Musk fired the entire Supercharger team of 500 on Monday and more high-profile executive departures ensued (e.g. Daniel Ho, head of new product development—an area of the utmost importance to Tesla right now).

Given how bad the Q1 results were, Tesla’s stock should be spiraling downwards, but this was a well-orchestrated pump either for an imminent equity raise or avoiding a margin call for Musk who may have pledged shares around $140 for loans. There is also the huge incentive for getting the share price higher ahead of the June 13th shareholder vote on whether Musk should get his $56 billion compensation package reinstated (a Delaware judge voided it due to having found “flaws” including Musk being friends with most of the Board members who approved it in 2018).

A Sober Look: Fundamentals Are Dire

It’s worth a reality check to see just how far out of whack Tesla’s stock price has been removed from the fundamentals. First, the Q1 results after the 10-Q was released just hours after the earnings call:

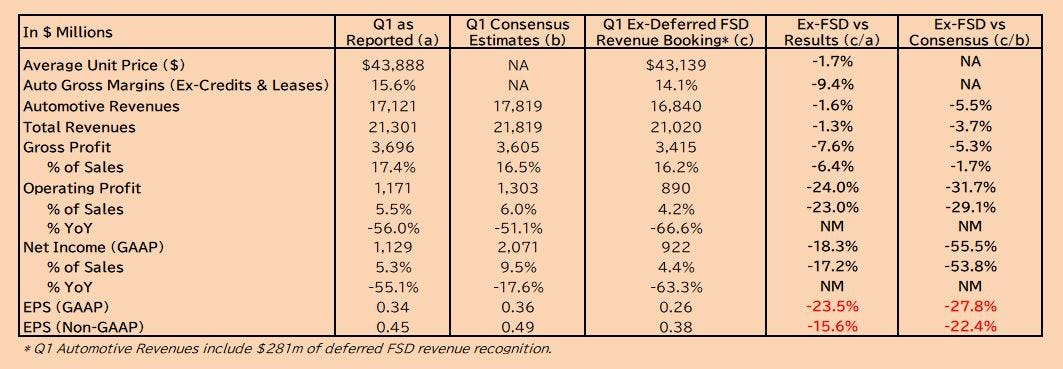

Figure 1 shows Tesla’s Q1 results after stripping out deferred FSD revenue recognition of $281 million. As can be seen, removing this abnormally large booking would’ve led to operating income missing consensus estimates by 32% and GAAP net income undershooting by 28%.

While I had thought that the booking must’ve been much higher due to ASPs not having fallen very much in Q1 (deferred FSD revenues are booked in Automotive Revenues and, even after stripping it out, average prices fell by a mere 0.3% QoQ despite hefty price cuts in the US and 3% cuts in China), $281 million is the second-largest amount of deferred FSD revenues booked by Tesla since Q4 2022’s $309 million.

The operating margin of 4.2% (excluding the deferred FSD revenues) is the lowest since Q3 2019’s 4.1% and less than half of GM’s 8.9% in Q1.

Finished Goods Inventory of $6.75 billion is a record high in absolute terms and is back to supply-chain disruption levels of 32% of revenues in 1H 2020. Finished Goods Inventory as a percentage of revenues saw a low of 5% in Q1 2022 when Tesla generated its record-high operating margin of 19.2%.

Unloading this inventory (see the cover picture above from Scottsdale, Arizona, and Figures 2 & 3 below from Brandenburg, Germany) will not be easy without deep discounts. Dividing Finished Goods Inventory of $6.75 billion by the average cost/unit of $36,261 in Q4 2023 (Q1 2024 COGS was distorted by a month’s shutdown of the German factory and Cybertruck start-up costs) gives you 182,083 units of vehicle inventory, or 39% of Tesla’s Q2 deliveries last year.

While the images of parking lots in Arizona and military airports in Germany filled with new Teslas may not be a big deal if this were the last month of the quarter, having this many cars sitting around at the start of the quarter is alarming. It points to further price cuts this quarter.

Figure 1: Tesla’s Q1 Results Ex-FSD Revenue Recognition

Figure 2: Inventory in Brandenburg

Figure 3: Aerial Shot of Brandenburg Inventory

The China FSD Pump—Big Fat Nothingburger

While this deal is still not finalized (there are many hurdles in terms of mapping, data storage, etc. which all are national security issues in China) it doesn’t sound like it will be profitable for Tesla for the following reasons:

Tesla will need to use Baidu for mapping and data storage, which inevitably eats into profits.

FSD monthly subscription rates will need to be competitive with local, more advanced ADAS products, so Tesla will likely only be able to charge $50/month versus $100/month in the US.

With a generous assumption of a 50% FSD take rate (305,000 vehicles based on 2023 deliveries in China), annual revenues would only be $180 million, part of which would go to paying Baidu for its services.

As noted in this Bloomberg article (here), in the fiercely competitive and tech-hungry Chinese car market, Tesla may ultimately have to give FSD away for free if competitors do so.

So, for a best-case scenario of $180 million of annual revenues ($0.04/share) from FSD sales in China, Tesla shares on Monday rose as much as $97.4 billion intraday. This brings back memories from the gamma-squeeze days of late 2019 and most of 2020, when Tesla faced high growth ahead.

Final Thoughts—The Walls Are Closing In

As mentioned in my report, Could Tesla Go Bankrupt? The Odds Are Rising (link here), old models like those in Tesla’s lineup become stale and stop selling without full makeovers, which every carmaker does on a regular basis (e.g. 12 generations of the Toyota Corolla and 7 generations of the BMW 3 Series).

Full model changes require billions in R&D and capex over at least a 4 to 5-year development cycle. Musk saying that Tesla will have “new models” by early 2025—and then refusing to give details when asked whether they would simply be “tweaked” versions of the Model 3 & Y—is highly deceptive. In fact, I’m hoping there aren’t any of the usual delays because I’m dying to see what these “new models” look like. Tesla’s refreshes of the Models S, X, and 3 have all been failures that led to lower sales.

The fact that it is so clear that the walls are closing in on Tesla due to its empty product pipeline makes one wonder how it can maintain a market cap of $574 billion. Figure 4 shows Tesla’s egregious valuations relative to its major competitors in the auto industry and Figure 5 shows how overvalued Tesla is as an “AI” stock if you believe it’s not a carmaker.

Figure 4: Valuation & Returns (Ranked by 2024 Pre-Tax Margin)

Figure 5: Tesla Vs Rivals in the “Magnificent 7” (Ranked by PEG Ratio)

Note: Nothing in this report is investment advice.

Musk is truly a grift genius. I do imagine him having a pump planner and essentially orchestrating his entire business strategy primarily around the pump schedule to keep everything spinning somehow.

AI/FSD - even if successful isn't worth that much

New models - rushed junk like the cubertruck or damp squib rehashes...can't keep sales up

Surely the walls are closing in...

So, allow me to propose an alternate interpretation on why Musk went to China.

The notion that Musk went to China to facilitate the roll-out of FSD in China is codswallop in my humble opinion. The China trip seemed hastily arranged with no prior announcement. To the best of my knowledge, we didn't know about this China visit until the plane was in the air.

Here is my theory. This trip was SEO (Search Engine Optimization). The NHTSA Office of Defects Investigation came out with a fairly devastating report on Autopilot/FSD on the Friday (?) immediately prior to the Musk China visit. The NHTSA report indicates that Tesla only reports something like 18% of crashes involving Autopilot/FSD. Musk wanted the news of this report off the front page. The following Monday all we hear about is the alleged roll-out of FSD in China. Anyone searching on Monday for information on "Tesla/Autopilot/FSD" will be greeting with nothing but news of the China trip. Mission Accomplished.

The Chinese played this game for their own reasons. They need foreign direct investment. They wish to show how accommodative they can be to business wishing to operate in China.

This was theatre, nothing more. But I think it was well played by him.

The agreement with Baidu for Tesla to utilize street mapping in China was inked in January 2024.

https://pandaily.com/tesla-is-testing-lane-level-navigation-in-china-collaborating-with-baidu-maps/

https://montanaskeptic.substack.com/p/the-nhtsa-has-finally-exposed-musks/comments

Of course, Musk could have gone to China looking for money...always a possibility.